There are potentially attractive yields on offer for fixed income investors in selected parts of the European financial bond market.

Interest rates in the eurozone have been falling gradually since the 2008 financial crisis and are now at record lows. As a result, investors are looking for opportunities to earn higher returns in the fixed income markets. While the post-pandemic recovery makes it challenging, the banking sector still has something to offer, especially in the lower tier segment.

Valuation attractiveness of subordinated and AT1

If the economic environment improves in 2021, cyclical sectors like financials should benefit from the rebound in activity when vaccines allow lockdown measures to ease and life begins to return to the way it was before the pandemic.

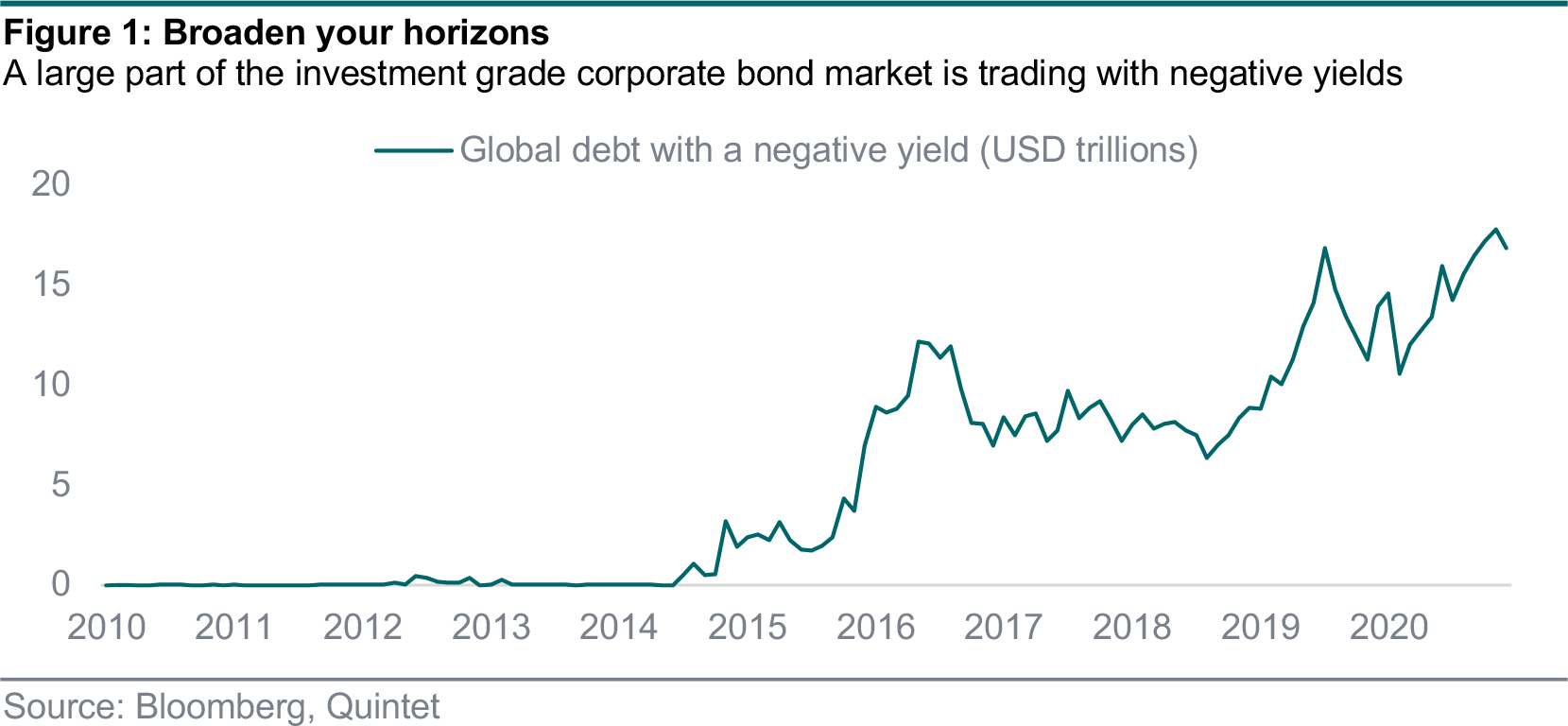

As well as an improving economic backdrop, the financials sector should also benefit as investors search for higher yields. The mood in investment grade corporate bond markets is likely to be optimistic in 2021, helped by the European Central Bank’s (ECB) asset-purchase programme. However, we believe investors need to broaden their horizons because a huge part of the credit market is trading with a negative yield (figure 1).

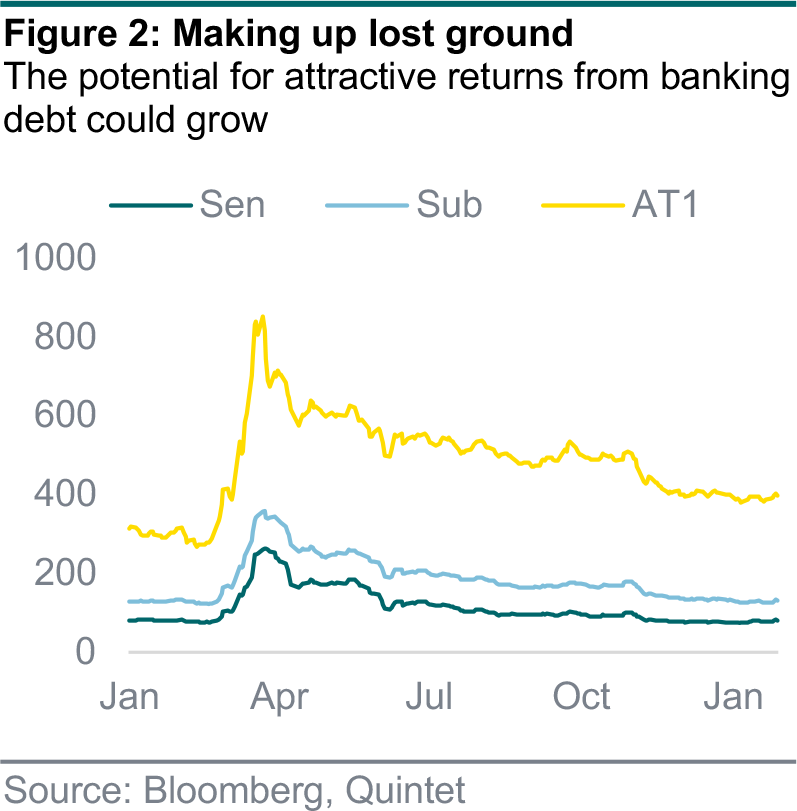

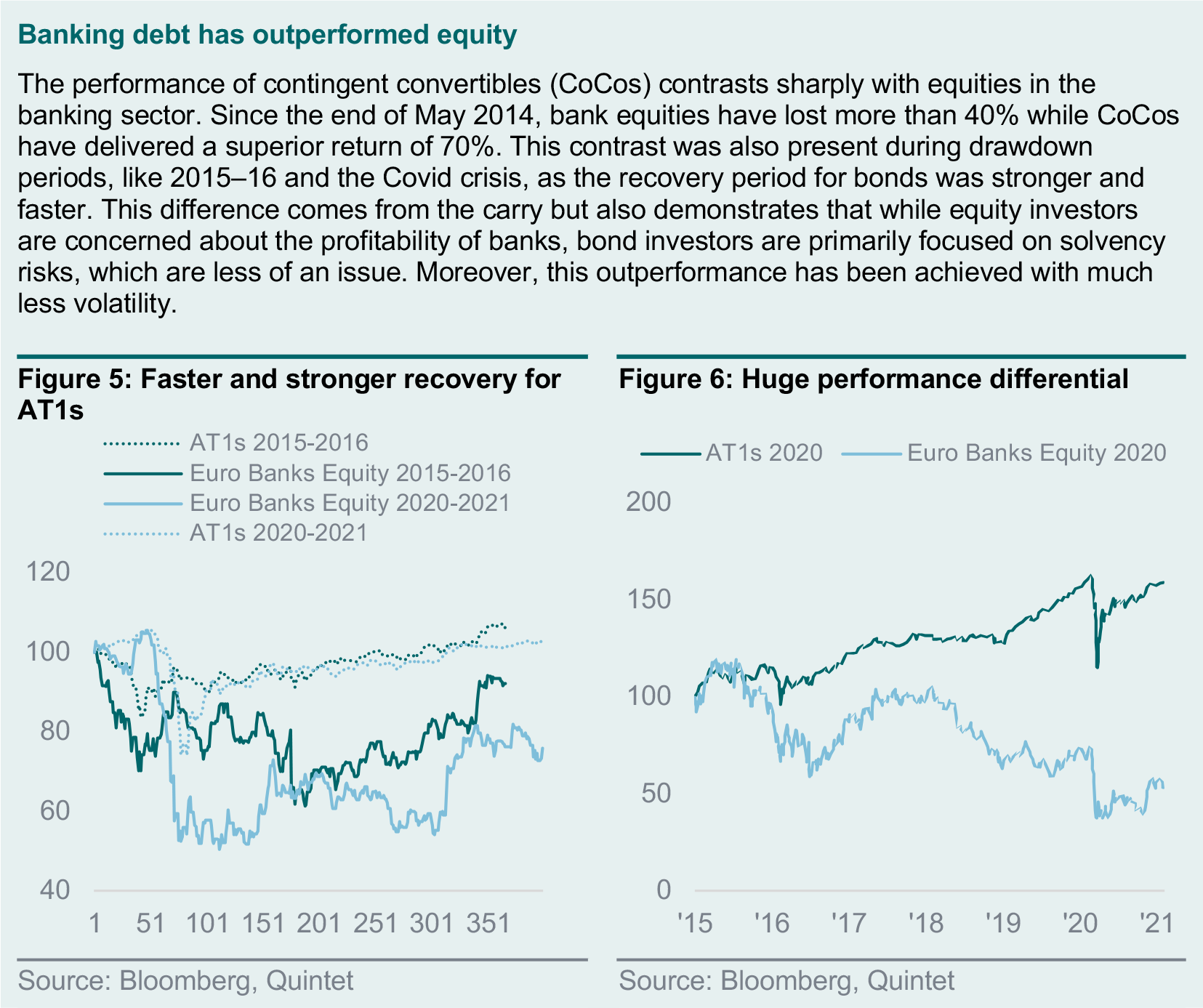

European senior bank debt spreads are already back to their early 2020 levels, and similar to non-financial corporate bonds. However, there is room for additional spread tightening for subordinated bank debt and additional tier 1 contingent convertibles (AT1s) as they make up lost ground (figure 2). AT1s and subordinated bonds have recovered 77% and 93% respectively compared to pre-crisis tightening. Even if the potential for subordinated debt compared to AT1 is more limited, we still consider it an opportunity as carry is also supportive.

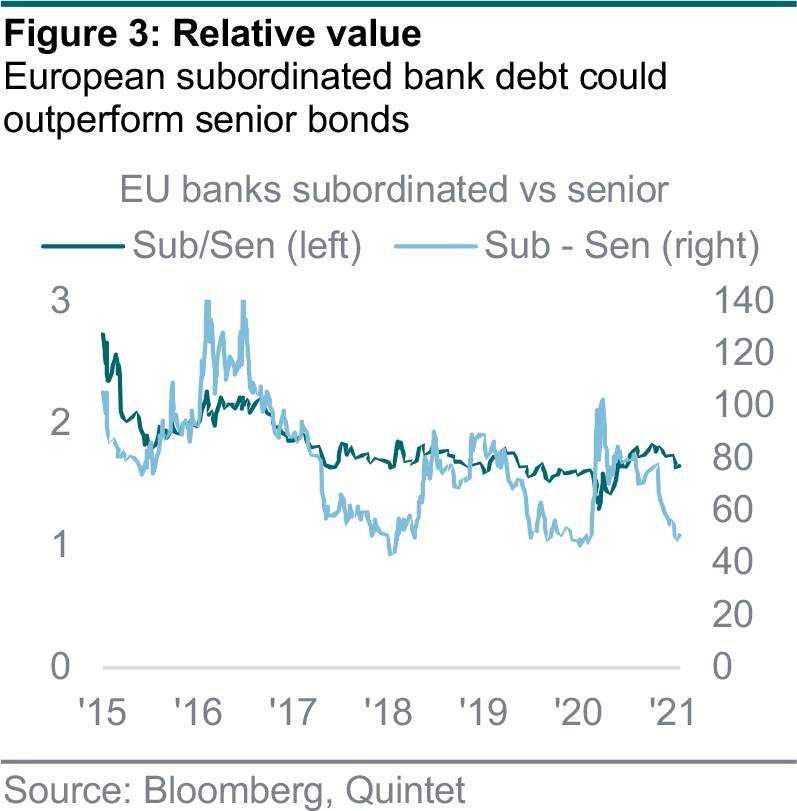

The valuation of subordinated debt and AT1s compared with senior debt reinforces this view (figure 3). The subordinated/senior debt ratio highlights room for subordinated bonds to outperform.

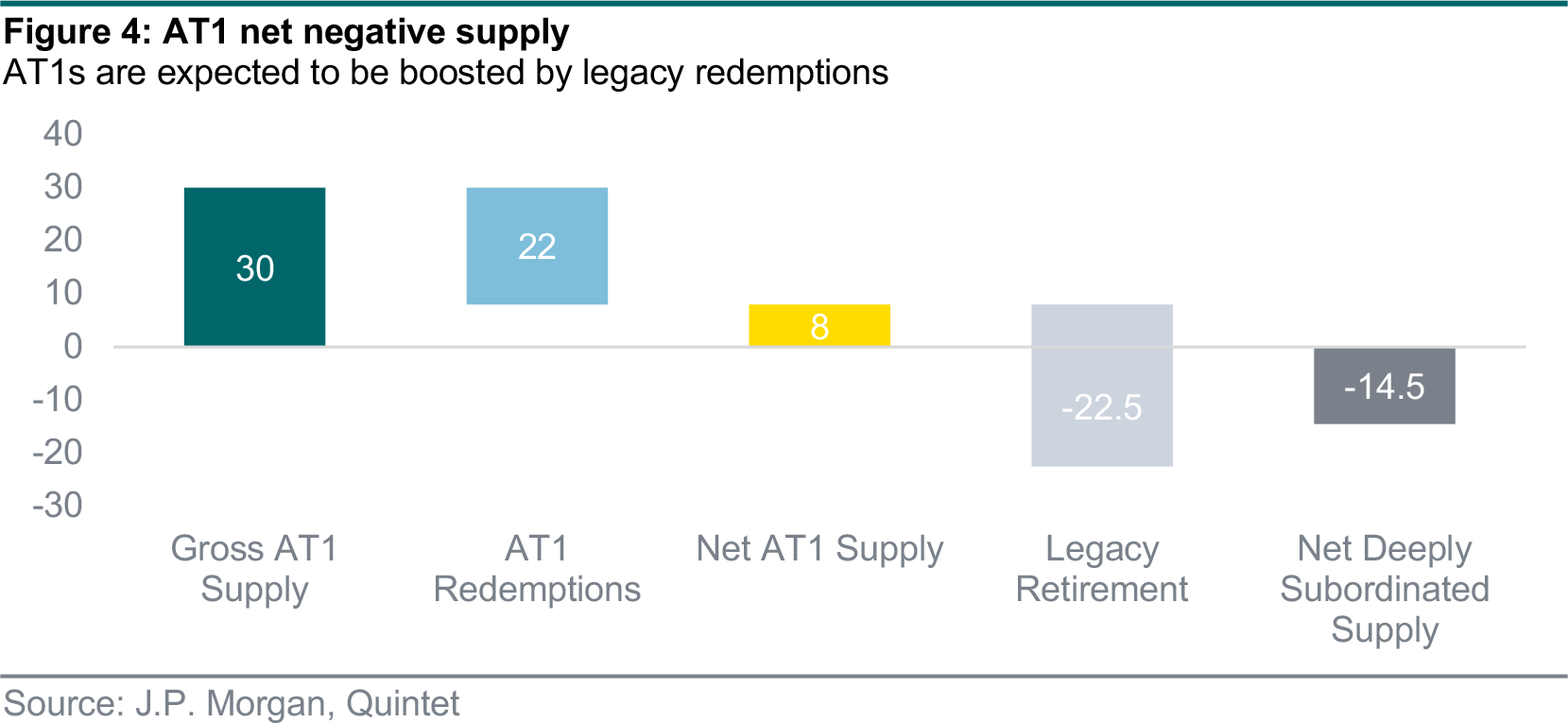

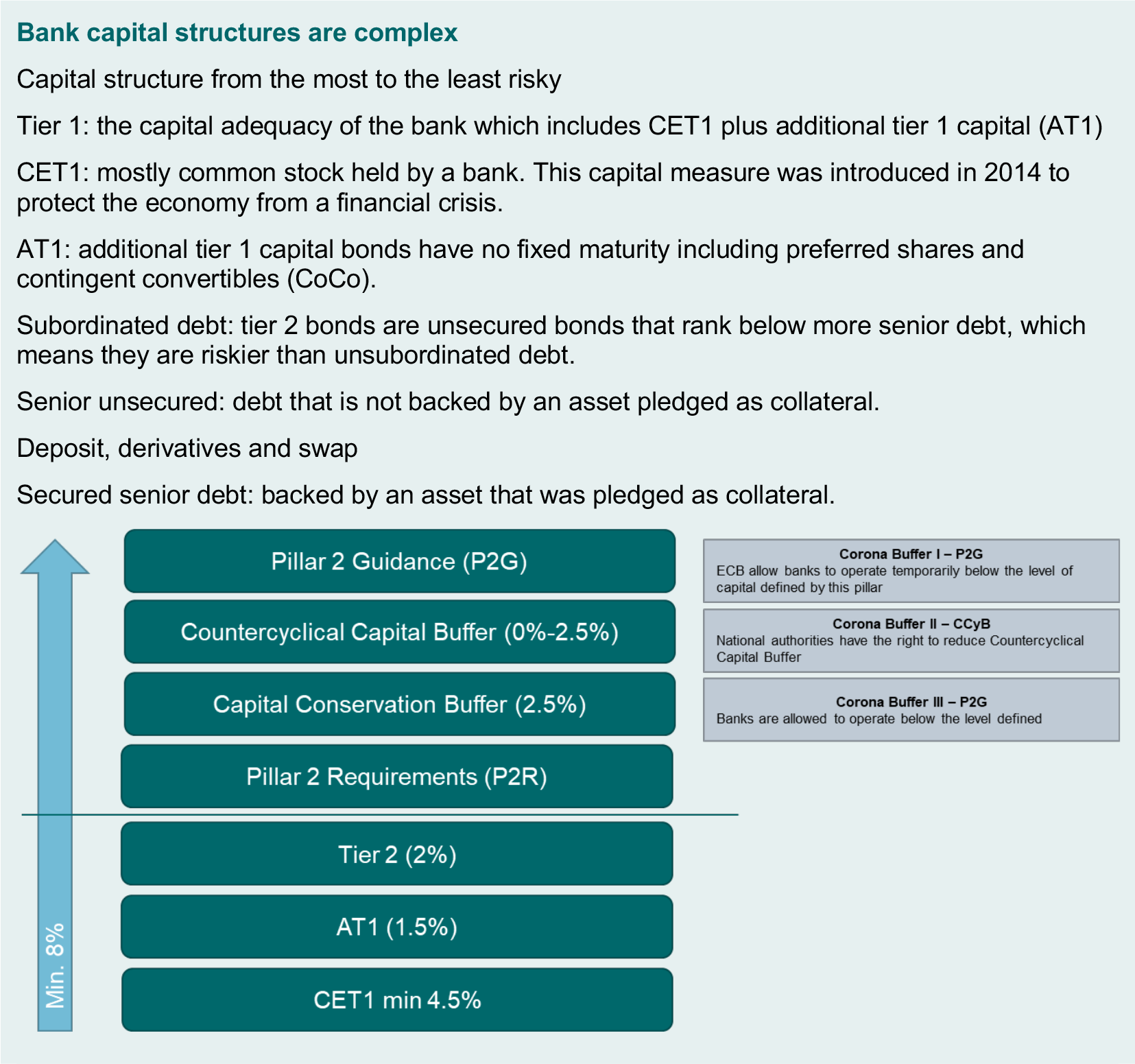

AT1 is a specific asset class that raises many questions for investors. They are subordinated bonds with a higher priority on the capital structure than equity but lower than other creditors. Early in the crisis, concerns about the potential conversion and the probability of non-call risks have been addressed to reassure the market. Indeed, as we enter the last year of the transitional arrangements for legacy capital instruments (generated during Basel II), AT1 should be supported by this technical factor as investors have to redeploy redemption proceeds.

Consequently, European banks’ subordinated bonds and AT1s represent an attractive risk/return opportunity supported by the expensiveness of the broad corporate market and their specific valuation attractiveness on a relative basis. Besides, this valuation aspect is corroborated by healthy banking fundamentals.

European banks are in good shape

When looking at the very poor performance of shares in the European financials sector in 2020, we could have a global negative perception of European banks and their capacity to rebound from the crisis. However, from a bondholder perspective, they are in good shape to manage the consequences of the crisis thanks to their long-term thinking.

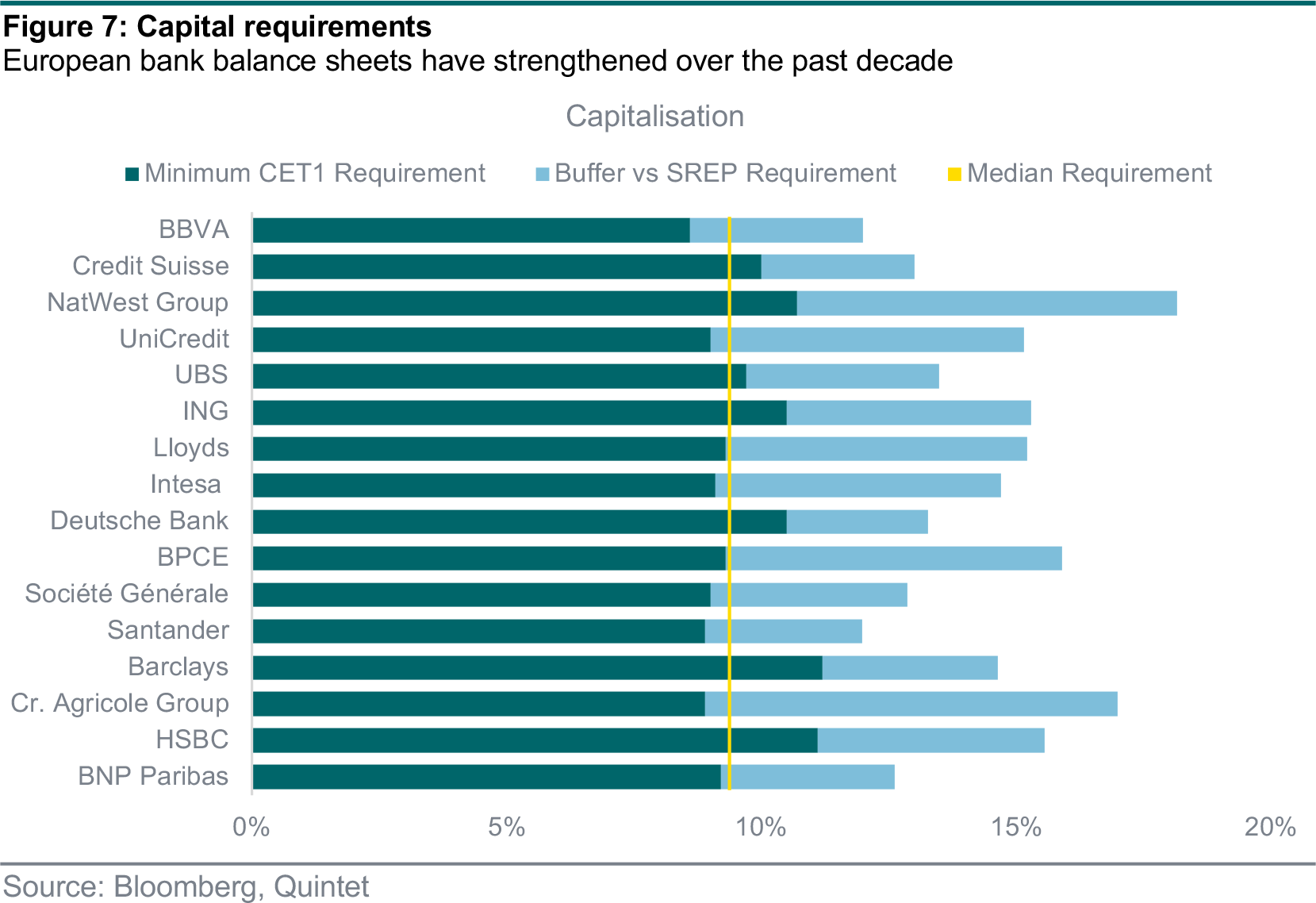

Since 2008, the regulatory requirements imposed by authorities have strengthened the balance sheet of European banks. The efforts of the banking system and the reforms translated concretely into better liquidity positioning and stronger capital profiles (large CET1 buffers) (figure 7).

The weak spot is on the profitability side, where low rates have been putting pressure on interest margins for a long time. However, banks continue to tackle the issue by activating the levers at their disposal – strict cost management and restructuring measures – when deemed appropriate. This approach has already led to many M&A deals – especially in Southern Europe, such as Intesa/Ubi Banca and CaixaBank/Bankia) – and to a higher concentration of participants in the sector.

At this stage, most deals are domestic owing to cross-border hurdles and substantial economies of scale. The timing for M&A is particularly good as the poor equity performance of targeted companies in 2020 enables the recognition of badwill for the buyer (as equity value is lower than accounting net asset value).

The evolution of non-performing loans (NPLs) is another indicator closely followed by the market. The expectations cloud the outlook for banks slightly, as their level will undoubtedly increase with the progressive withdrawal of government support and the consequences of the crisis in the real economy (such as unemployment and loan impairments). However, while reversing from a recent favourable trend, we do not expect NPLs to run out of control, especially as banks have already front-loaded provisions for loan losses in 2020. Moreover, the European Commission has specified its strategy to support the risk associated with the four following objectives:

This example is one aspect of the way the regulation broadly supports banks and limits the risks associated with the crisis. Indeed, European banks can count not only on their strong fundamentals, but also on the unfailing support of European institutions.

The support of banks by European institutions does not materialise directly in the low rates environment that drag the profitability, nor in the pandemic emergency purchase programme

(PEPP) from which banks are excluded. However, the ECB does not forget banks as they play a key role in the funding of the real economy. The European institutions confirmed their support, which will remain beneficial in the future.

In order to manage the consequences of the Covid crisis, European banks have benefited from the easing of regulatory constraints from March 2020. This includes capital buffer and leverage rule releases but also IFRS 9/Basel III transitory measures. For example, banks could operate below their Pillar 2 Guidance (P2G) and Liquidity Coverage Ratio (LCR) in order to lend to companies and households, and support the economy. These easing measures have reduced the pressure on financial institutions, even if most of them have kept strong buffers.

Furthermore, the Governing Council of the ECB shows its support by very attractive financing access. Initiated directly after the crisis, this support was reaffirmed on December 2020 when the ECB:

Another important element is on the capital distribution side. After a period of temporary suspension of all cash dividends and share buybacks from March 2020, the ECB put in place a dividend and share buyback policy in December 2020 to limit distributions until September 2021. The possible distribution was limited at a maximum amount defined as follows: “the ECB expects dividends and share buybacks to remain below 15% of the cumulated profit for 2019–20 and not higher than 20 basis points of the Common Equity Tier 1 (CET1) ratio, whichever is lower” (ECB press release, 15 December 2020). This measure – unfavourable to shareholders – is clearly supportive for bond holders, as it will contribute to keep buffers at healthy levels.

All these measures enable the reinforcement of European banks to address issues raised by the crisis. In the short to the medium term, it is supportive and should continue to be. In this context, the underlying risks associated with subordinated bonds and AT1s are limited, while we believe valuations represent an attractive investment opportunity.

A late surge in issuance meant 2020 was another record year for green bonds, with USD 269.5 billion issued. Since 2015, financial issuers such as banks and insurance companies have been a steady source of growth for the green bond market. They now represent the third largest issuer group with around 20% of the annual total.

Typically, banks tap the green bond market as a funding source for loans linked to energy projects (such as commercial renewable energy) or commercial and residential real estate (such as energy efficiency improvements and green buildings), while other categories such as transport and the circular economy make up a smaller share of the proceeds.

BNP Paribas has been a regular issuer of green bonds since 2016, and most recently came to market with a EUR 750 million green bond in October 2020. The bank provides a good example of the typical profile of a financial green bond: renewable energy makes up 67% of the underlying assets, with green buildings representing 25%, and 8% being allocated to clean transport and water management.

Last year also saw the first ever green contingent convertible (CoCo) bond by a financial institution, a EUR 1 billion benchmark issue by BBVA. The bond was met with significant investor interest given the higher coupon (6%) available. In a market where the average coupon is only around 1% due to the preponderance of high-quality issuers, other banks look likely to follow – now that BBVA has tested the water – and tap into the growing demand for high-yield green debt.

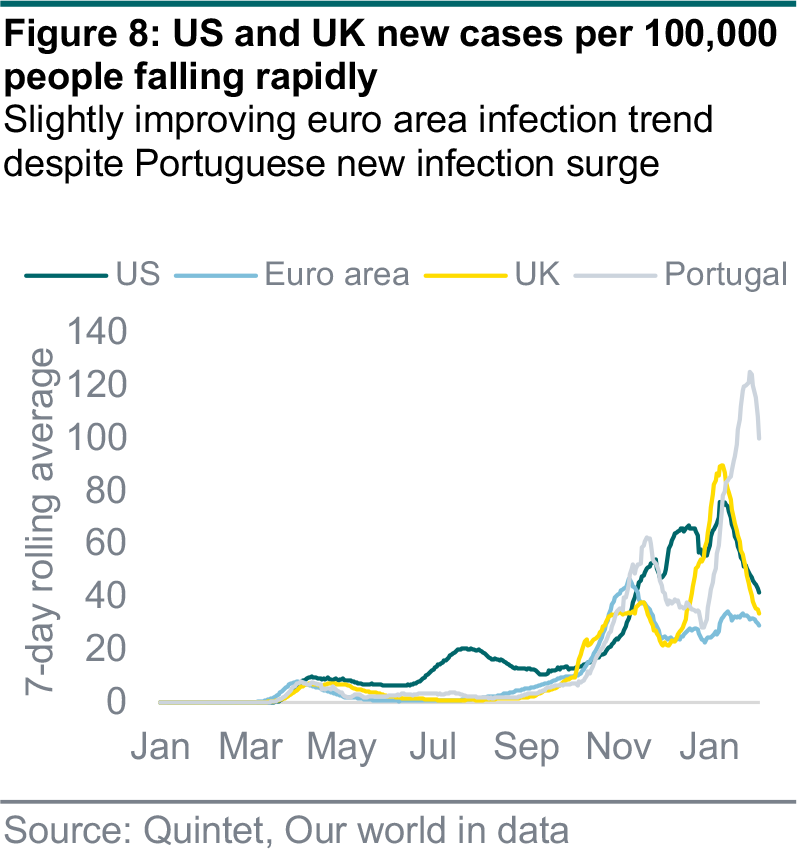

The number of globally confirmed cases of Covid-19 continues to rise and now stands at around 105 million. The rate of infection is falling sharply in the US and UK, but not in the euro area – where the level, however, has been lower for some time and below last year’s peak (figure 8). The situation is improving in Germany and Italy. Yet France is struggling to control the pandemic and the rate of new infections has risen sharply in Portugal.

In the US, new infections are falling after peaking at the start of the year. With less than 40 new infections per 100,000 inhabitants, the rate is similar to the one across euro area. The rate is slightly higher in the UK but is falling rapidly and it looks like both the US and the UK will soon be at lower levels than the euro area.

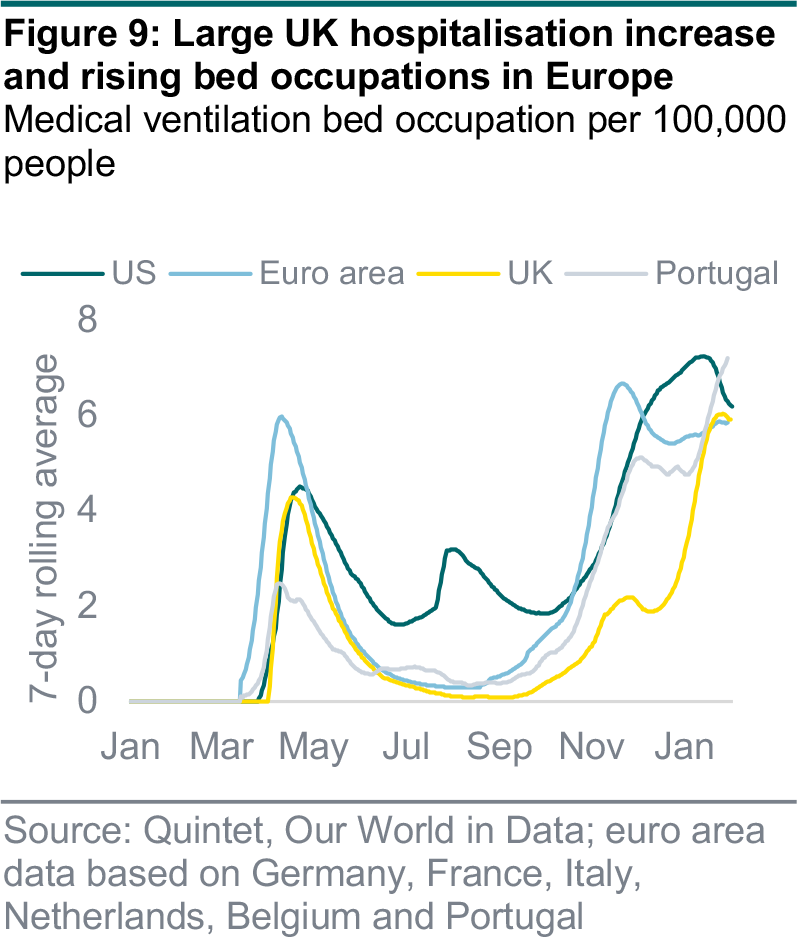

These developments are not yet reflected in subsequent intensive care unit (ICU) occupancy. The figures are already softening in the US and slightly rising again in the euro area after a drop at the end of last year, with the latest turn driven by individual countries, such as Portugal. In the UK, ICU occupancy is rising quite quickly (figure 9). This sharp increase can be attributed to the high number of infections in recent weeks, as hospitalisations have a time-lag effect.

Infections in Portugal increased so drastically that at times there was a state of emergency in ICUs. This development was reflected in stricter lockdown measures, which are still in place in most of Europe as well. Restrictions have also been tightened in the US, which include making masks compulsory on public transport.

The global median age of people who are hospitalised is 63 years, which is more than 30 years above the median of the world population and almost 20 years above the European median. This implies that a large proportion of people with severe Covid-19 disease can be classified as elderly. In addition, according to the Centers for Disease Control and Prevention, the mortality risk for someone aged 85 or older is 630 times higher than that of a young adult. Based on this data, most governments have opted for a similar vaccination strategy, in which older people and healthcare workers are at the front of the queue.

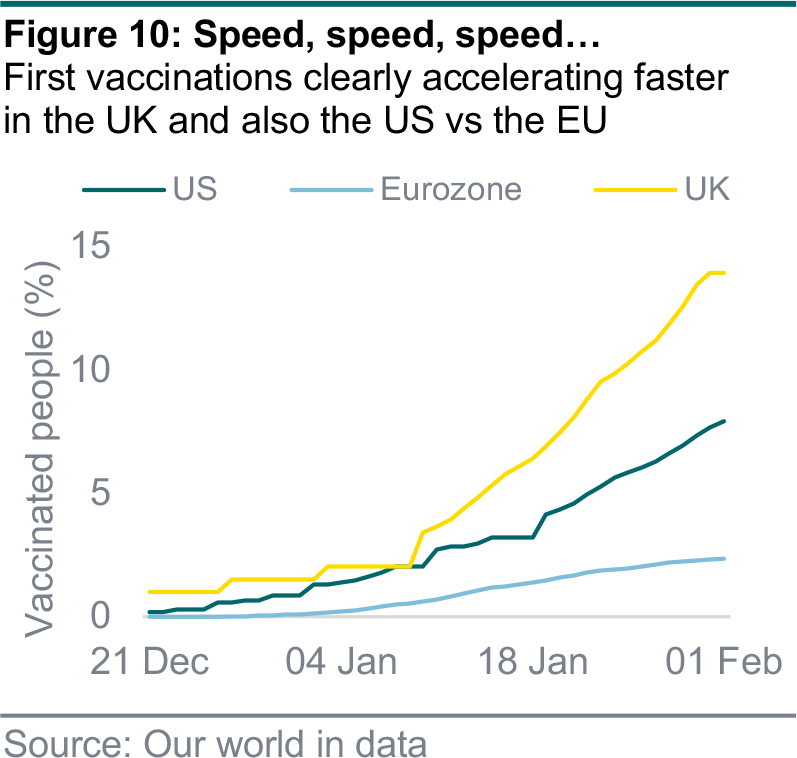

In both the euro area and the UK, as well as in the US, where President Biden is intensifying the vaccination campaign, inoculations started at the end of December. However, the numbers vary substantially between regions (figure 10). More than 10 million people in the UK have already received their first dose of the Covid-19 vaccine, and the programme is also being rolled out widely in the US. In contrast, Europe is suffering with substantial problems, including inadequate supplies after a longer approval process and ordering delays.

The UK has now vaccinated about 18% of its population with at least one shot compared with 4 times less in the euro area (in percentage terms). Owing to the more infectious mutation from the UK and another one in South Africa, the pressure to vaccinate quickly and efficiently has increased once again. The US has been vaccinating more than a million people a day and more than 8% of its population have received their first dose. The Biden administration plans to accelerate the programme, which will be supported by funds from the upcoming billion-dollar fiscal stimulus package currently being negotiated in Congress. This rapid process should continue to limit new infections during 2021.

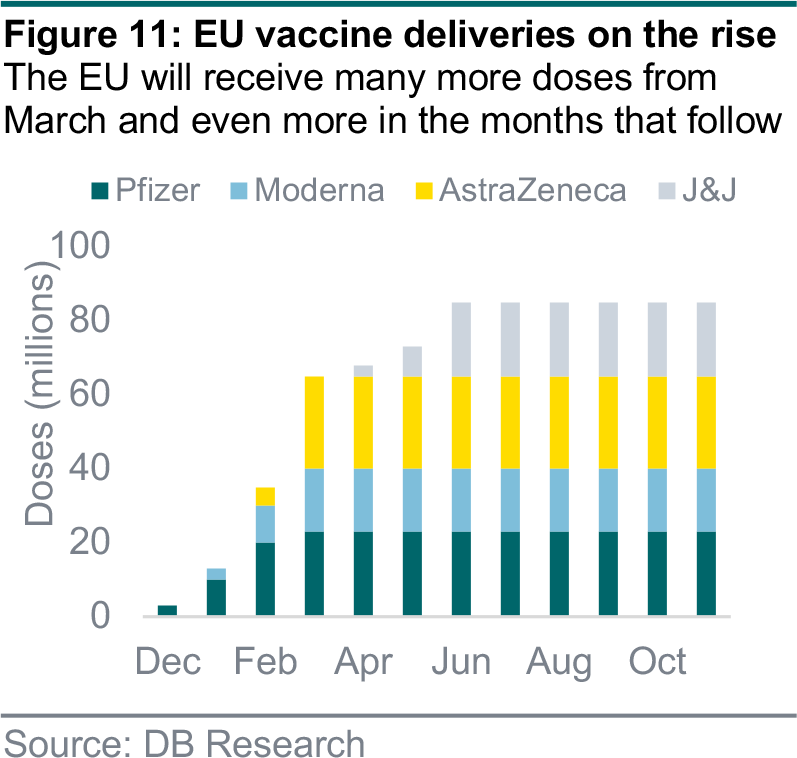

Continental Europe’s bumpy start to the vaccination process leaves it far behind other developed regions. The region has managed to secure additional supplies and the programme should pick up speed as new vaccines are approved and production facilities are expanded. However, it looks like the UK and US will be able to start reopening their economies much earlier. Figure 11 highlights one bright spot for the EU: its contracts with manufacturers of vaccines include sharply rising delivery volumes for the upcoming months.

AstraZeneca will start delivering its vaccine to the euro area in February, initially in small quantities but they should increase. In addition, Pfizer/BioNTech and Moderna are supplying vaccines at an accelerating pace, and from April Johnson & Johnson will also deliver its vaccine. Several additional vaccines could receive approval in the spring, including from CureVac, which has partnered with Bayer and AstraZeneca, which raises hopes for faster vaccinations.

The risk of further mutations that are more resistant to current vaccines is an ongoing risk. Yet studies continue to suggest they offer a high level of protection. A combination of vaccination programmes and higher temperatures in the spring should allow the economy to begin reopening, paving the way for early-cycle recovery.

Lionel Balle Head of Fund Management & Fixed Income

Amélie D’Agostini Fund Manager

Yann Kahe Fund Manager

Daniele Antonucci Chief Economist & Macro Strategist

Bill Street Group Chief Investment Officer

This document has been prepared by Quintet Private Bank (Europe) S.A. The statements and views expressed in this document – based upon information from sources believed to be reliable – are those of Quintet Private Bank (Europe) S.A. as of 8 February 2021, and are subject to change. This document is of a general nature and does not constitute legal, accounting, tax or investment advice. All investors should keep in mind that past performance is no indication of future performance, and that the value of investments may go up or down. Changes in exchange rates may also cause the value of underlying investments to go up or down.

Copyright © Quintet Private Bank (Europe) S.A. 2021. All rights reserved.