There are potentially attractive yields on offer for fixed income investors in selected parts of the European financial bond market.

The US continues to outperform Europe for a variety of reasons, including its technology giants, which have been the standout winners amid the pandemic. Within Europe, the UK is a drag.

There has been muted market reaction to strong beats in the US – especially in tech and financials – but more positive rewards for beats in Europe. Companies not as upbeat as they were in Q3 2020 with forward guidance.

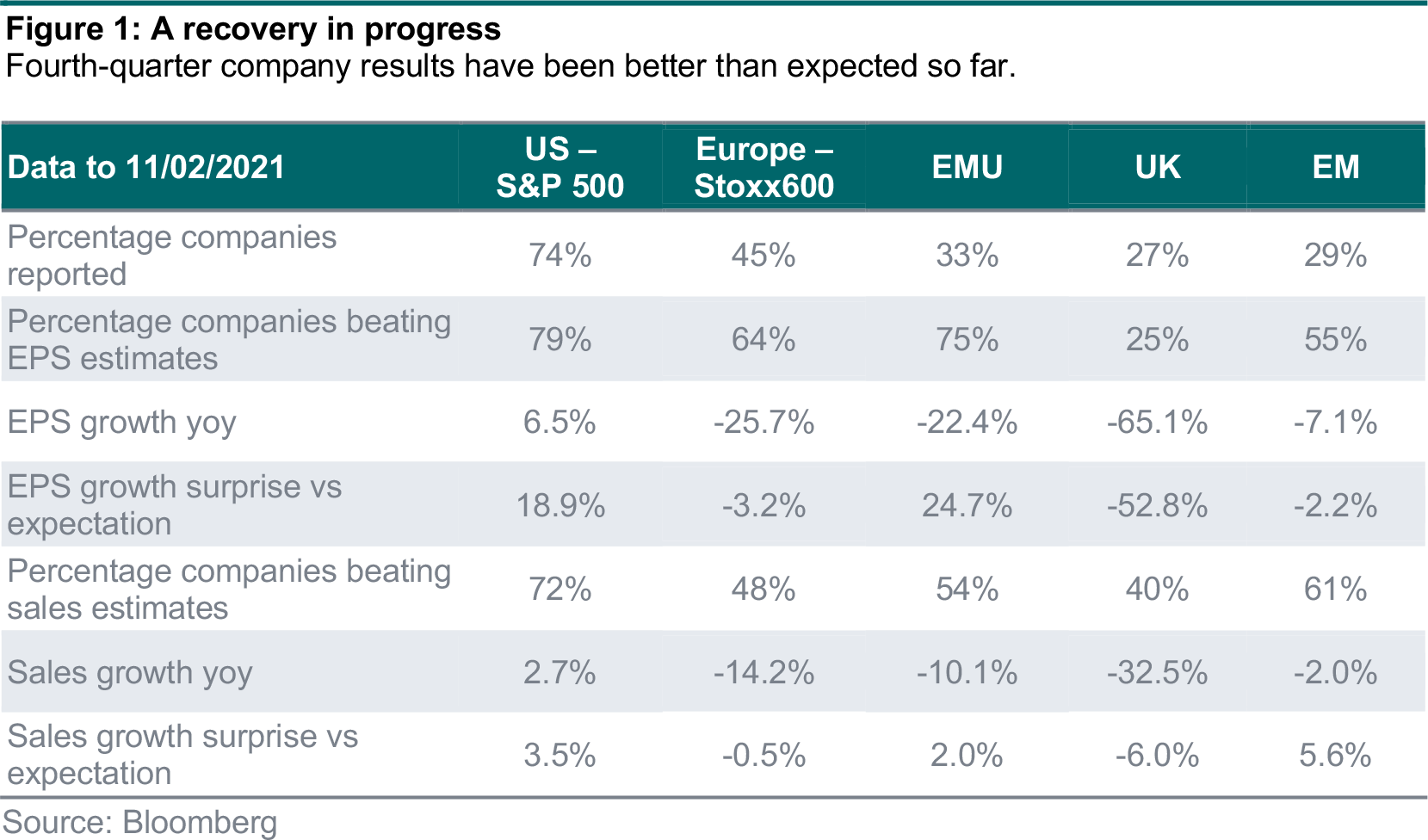

With 74% of companies in the US and 45% in Europe having announced results (as of 11 February), the fourth-quarter (Q4) reporting season is not over yet but some clear trends are emerging (figure 1). We note that both in the UK and emerging markets (EMs), only a small percentage of companies have reported (below 30% so far). Although we look at the short-term figures, one should remain focused as always on medium- to longer-term trends rather than on assessing companies and sectors based on single quarters.

Overall, the Q4 earnings season is showing that despite ongoing lockdowns, the world and companies are not suffering to the same extent as they were at the start of 2020. This is in part because companies and consumers where possible have learnt to adapt to the pandemic. However, we continue to see a dichotomy in operating performance between the sectors most impacted by the pandemic (such as physical retail and energy) and those that have benefited from it (online businesses) in terms of year-over-year growth rates.

For instance, earnings growth is showing signs of turning positive on a year-over-year basis in the US, up 6.5% from Q4 2019 levels, while still 25% below Q4 2019 levels in Europe. Sales are also up 2.5% on last year’s levels in the US, but 14% lower in Europe.

Companies are in general surprising positively versus expectations, with earnings growth in aggregate around 19% better than analysts expected in the US, but 3% below expectations in Europe. Within Europe there is a clear differential in performance between companies listed in the eurozone, which have surprised positively (20% aggregate growth surprise, just like in the US), while UK companies have so far reported disappointing results.

We note a difference between Europe and the US in that almost 80% of companies have beaten estimates in the US versus only 64% in Europe. However, 64% is a record high in Europe; in addition, if one strips out the UK, the eurozone has seen 75% of companies beating expectations, which is a record high versus an average of around 55% since 2009.

Outside the US and Europe, we are now reporting on EMs, where only 30% of the companies have announced results, with 55% of firms beating earnings expectations. With a sector composition in between Europe and the US in terms of balance between tech/internet and ‘physical’ sectors, earnings growth in EMs unsurprisingly stands in between at -7%, with sales growth at -2%.

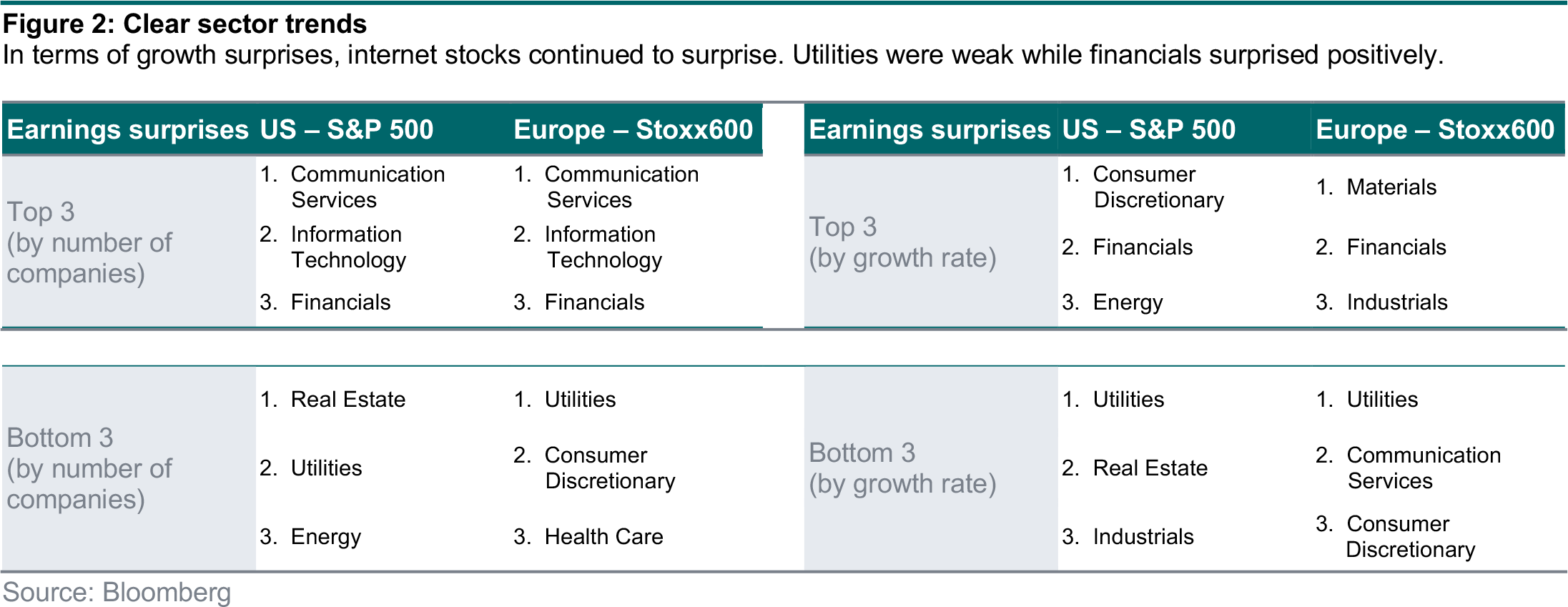

Beats in the US were once again substantial in the tech and internet-related segments (figure 2), with index heavyweights reporting stellar profits, including Amazon ($14.09 vs $7.20), Microsoft ($2.03 reported EPS vs $1.64 expected), Alphabet ($22.3 vs $15.8) and Facebook ($3.88 vs

$1.25). These contributed markedly to the positive growth improvement compared to Q4 2019.

A boost to profits was also received from financials, particularly banks, both in the US and in Europe. It is worth noting that financials beating expectations did not create much enthusiasm from investors as the sector continued to underperform.

In the eurozone, we also observe a pickup in the performance from cyclicals in materials (Arcelor, Norsk Hydro and Boliden) and across the whole industrials complex.

The market performance differential between winners and losers from the pandemic so far has come through with a wide gap in operational performance (figure 3). It is interesting to observe in the short term that strong beats have not been rewarded by better share price performance in the US, while they have in Europe. It is worth noting that the headline earnings from a sector are sometimes dominated by extreme results from a small number of companies within them. We explore these below by focusing on a few industries.

Materials: Notable strong performance in the US from the likes of Freeport-McMoRan (miner) and Nucor (steel), and in Europe from the likes of Boliden (miner) and Linde (gas).

Industrials: European figures have been driven higher by very strong earnings and sales growth from shipping company AP Moller-Maersk. US figures have been mostly dragged down by the substantial falls in profits and sales from Boeing, General Electric and Raytheon Technologies.

Utilities: Not many companies in Europe have reported and negative results are so far being impacted by Scatec (renewable energy).

Energy: In the US, Exxon, Chevron and Phillips66 have seen profits collapse amid the Covid-19 demand falls. In Europe, the likes of Total, Shell and BP have had similar fortunes.

Structurally, we maintain our positive structural view on sectors exposed to innovation, such as technology and healthcare. Both sectors have reported solid results and we believe they remain well-placed to continue to benefit from their respective structural growth drivers. However, we remain cautious and selective within sectors such as energy and financials, where the long-term outlook remains challenging.

Cyclically, our equity tilts remain mostly regional (overweight EMs and US), with our early-cycle recovery macro view also expressed via an overweight to UK smaller companies.

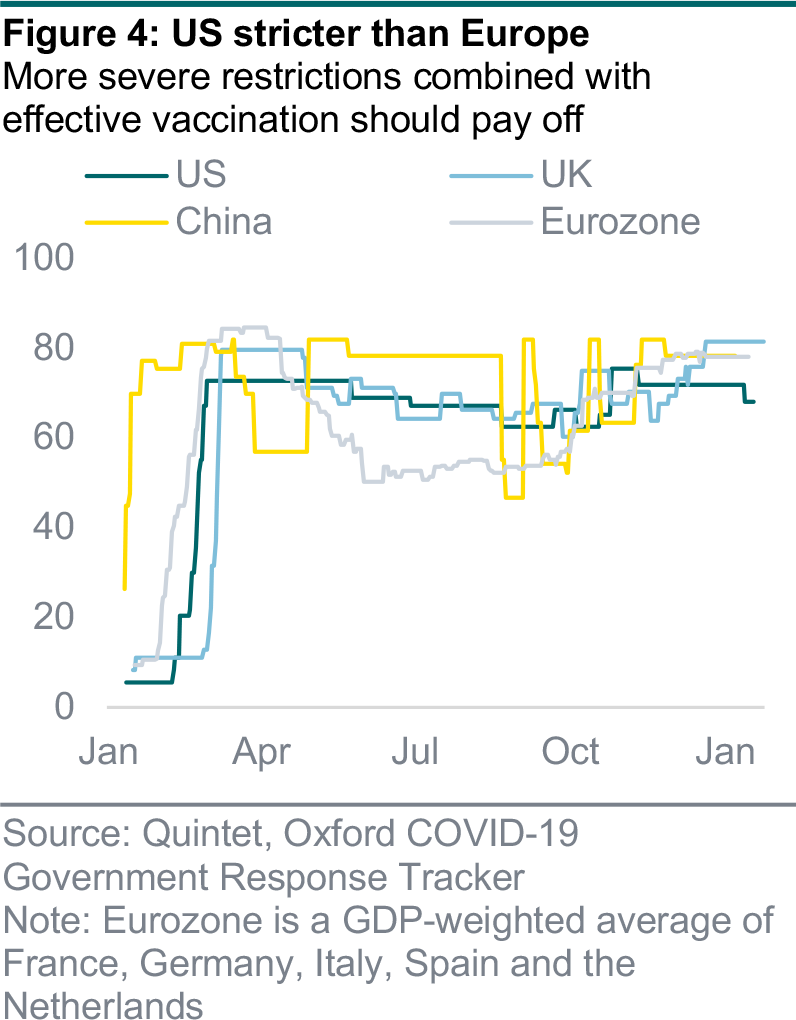

The total global number of confirmed Covid-19 cases around the world has risen to around 108 million. Yet the rate is slowing, with week-on-week infection numbers falling by about a quarter in the US and UK and by a fifth in Europe. The situation in Germany is improving and France’s third lockdown appears to be working. Although Italy’s infection rates remain mostly unchanged, tighter restrictions in Spain and Portugal also appear to be having a positive impact.

Fewer infected patients are receiving intensive medical care, which is easing pressure on hospitals in the UK, US and Germany – while those in Portugal and Spain remain most strained. One of the preconditions for governments to loosen lockdowns is a reduction in intensive care bed occupation, which leaves spare capacity for patients in need of medical ventilation.

Vaccination programmes are another key factor, and the US and the UK are progressing much faster than the EU. The US has increased daily inoculations to almost 2 million and already around 13% of Americans have received their first shot. A fifth of the UK’s population has been vaccinated, compared with just 4% in the EU. In the US and UK, around one third of their populations may already be immune to Covid-19 because they’ve been vaccinated or already been infected, which would mean they are halfway to achieving herd immunity.

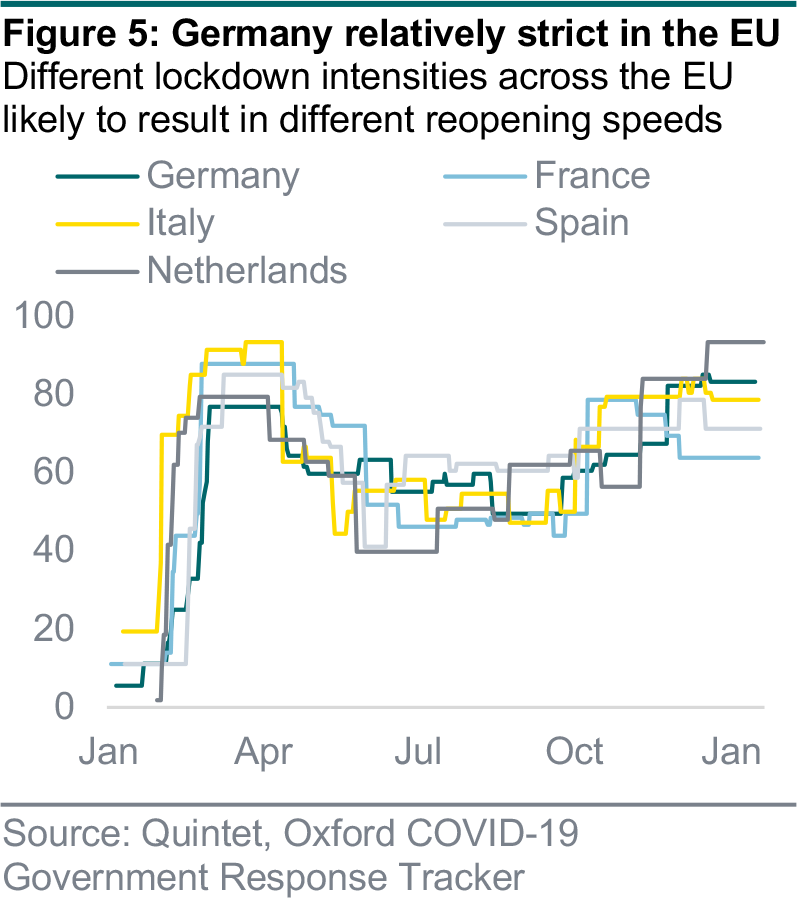

However, lockdowns are continuing to depress economic activity. Indices measuring the stringency of restrictions, including closing schools and workplaces and travel bans, show they are a major burden for Europe and a bit less so in the US. Within the EU, lockdown measures in the Netherlands are the most stringent among the major countries, ahead of Germany and Italy. Germany decided to prolong its lockdown by keeping shops and restaurants closed until 7 March in order to slow the spread of more infectious virus mutations and avoid a third lockdown.

These positive infection and vaccination trends suggest governments will be able to begin relaxing restrictions in the spring. As the vaccination programmes gather momentum, we expect consumer and services sectors to rebound, which will lead the cyclical recovery in the US and UK first, followed by the EU.

Cyrique Bourbon Senior Asset Allocation Strategist

Daniele Antonucci Chief Economist & Macro Strategist

Bill Street Group Chief Investment Officer

This document has been prepared by Quintet Private Bank (Europe) S.A. The statements and views expressed in this document – based upon information from sources believed to be reliable – are those of Quintet Private Bank (Europe) S.A. as of 15 February 2021, and are subject to change. This document is of a general nature and does not constitute legal, accounting, tax or investment advice. All investors should keep in mind that past performance is no indication of future performance, and that the value of investments may go up or down. Changes in exchange rates may also cause the value of underlying investments to go up or down.

Copyright © Quintet Private Bank (Europe) S.A. 2021. All rights reserved.