WHAT YOU NEED TO KNOW

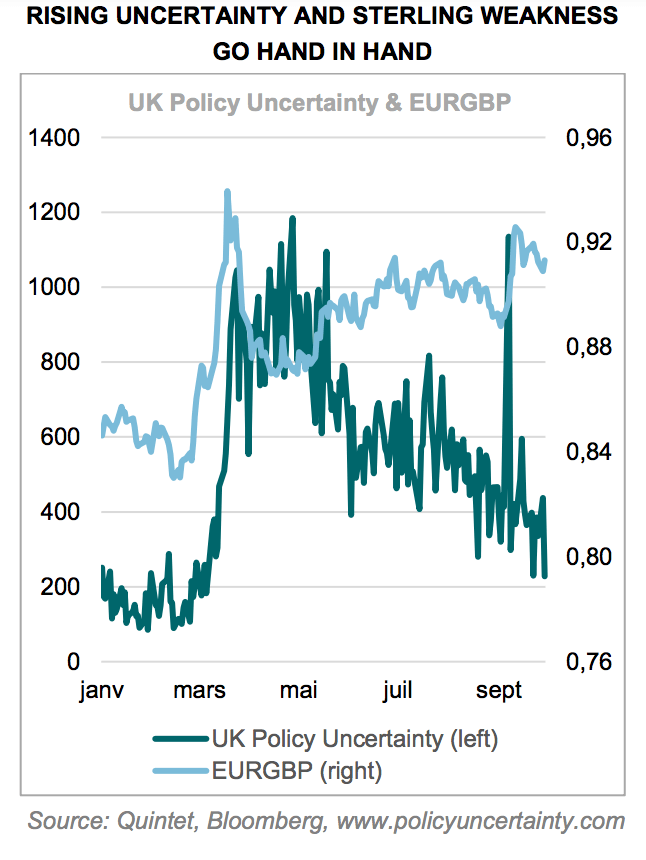

HOW WE THINK ABOUT POLITICAL RISK

Political risk tends to have a particularly pronounced effect on markets when it’s about a single, cathartic moment that tightens financial conditions, triggers a credit crunch and, therefore, risks putting the economy in recession. Examples include the Greek referendum on cash for austerity years ago, as well as votes that formally or informally were about euro membership: the French elections of Macron versus Le Pen and the Italian elections when anti-euro parties featured prominently.

Brexit is different. It’s a process, not a single event – a series of potentially small negatives that, if summed up over a long timeframe, may perhaps turn into a bigger negative for the UK economy relative to a no-Brexit counterfactual. But, taken individually, the impact isn’t going to be that much. And these effects are based on no-policy-change assumptions (other than Brexit).

So, looking beyond a likely adjustment period, a negative impact is not necessarily a given. Although some near-term disruptions on export/import and currency flows is likely while uncertainty rises, over the longer term we’d expect the trade relationship between the UK and both the EU and the rest of the world to evolve. The structure of the domestic economy should adapt too, which includes London as a financial centre, with no competitor at the moment on the same scale within Europe’s time zone. So the overall impact over many years remains very much an open question.

LEAVING THE EU AMID COVID-19 AND POLICY STIMULUS

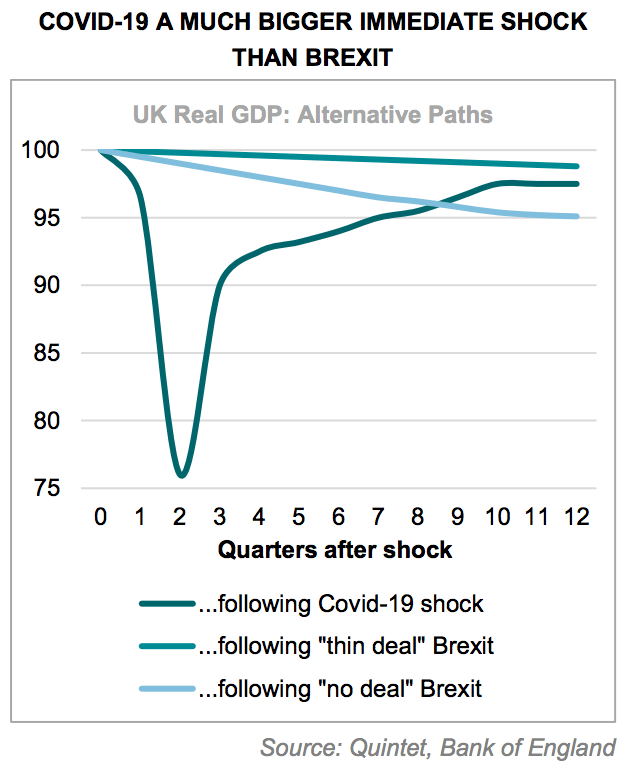

Brexit is taking place in the context of two very important developments. First, the massive shock to the real economy and financial markets caused by Covid-19. Second, the most comprehensive monetary and fiscal stimulus measures ever. Market participants sometimes see the virus outbreak and the UK exit from the EU as two mutually reinforcing shocks. We offer a counterpoint and argue that if there’s a good time for Brexit to happen, it’s now when both the government and central bank are stimulating the economy significantly.

Covid-19 has severely disrupted the real economy and, especially in the early part of this year, financial markets. While it’s difficult to separate one from the other, we think that the impact of the virus outbreak over the next few quarters – along with the measures to contain it – is likely to be much bigger than any effect Brexit may have, deal or no deal. If the lockdown following Covid-19 made a 20% hole in GDP in just a month, Brexit could perhaps cut one percentage point in a year. Relative to 2020, it’s going to be very hard for the UK not to rebound strongly in 2021.

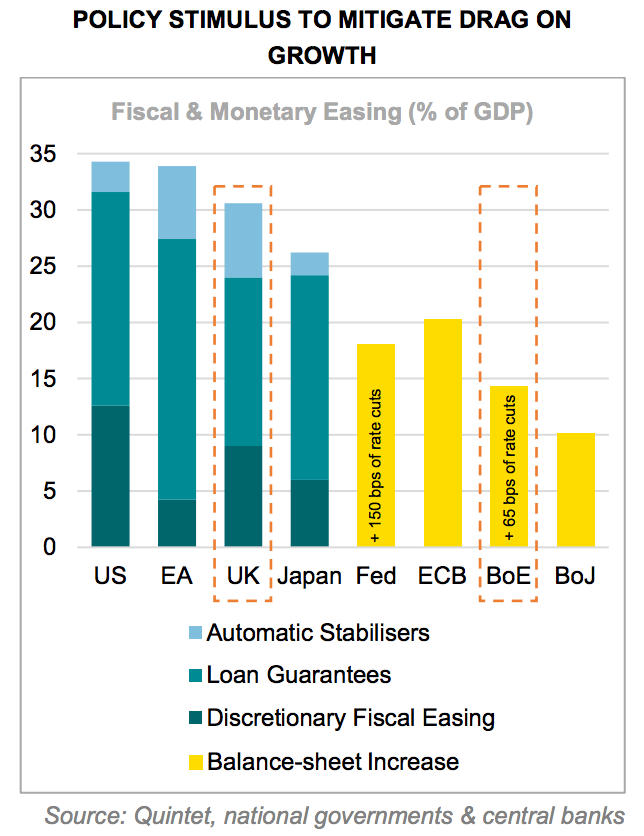

Large policy impulses – both directly and through currency depreciation – are likely to mitigate any short-term impact to a significant extent. Adding up discretionary fiscal easing, automatic stabilisers and loan guarantees, we estimate that the UK has deployed resources exceeding 30% of GDP. In addition, the Bank of England has eased financial conditions significantly by expanding its balance sheet via asset purchases and cutting interest rates. With the central bank keeping funding costs at rock bottom, we’d expect the government to borrow and spend as warranted.

WHAT TO EXPECT? SKINNY DEAL VS NO DEAL

The Brexit process has been dragging on for over four years. It’s hard to imagine that markets are so complacent to be surprised if negotiations don’t deliver a full deal. More likely, they expect a ‘skinny’ deal with minimal details or an inconclusive no-deal outcome to work out in more detail over time. This means that a confidence shock isn’t that likely anymore, with market pricing already reflecting – at least in part – the risks associated with these scenarios.

There have been some relatively encouraging signs that negotiations are progressing. Our expectation is that an agreement, perhaps at the very last moment, is slightly more likely than not. But we wouldn’t be surprised if such complex negotiations fail to deliver, or perhaps fail to do so over the pre-agreed timeframe. While assigning hard probabilities would be a fool’s errand, slightly more than even could be interpreted as 55% or so – though not too literally. Consider these two scenarios:

FX AND DOMESTIC EQUITIES KEY SWING MARKETS

The risk premium on UK investments should rise in a no-deal outcome. With rates already very low, we think that currency depreciation is one of the main drivers for financial conditions to ease further. Sterling would look vulnerable especially if markets were to assign a higher probability to a rather disorderly Brexit, perhaps going to parity versus the euro. A deal, however ‘skinny’, is unlikely be a big currency mover.

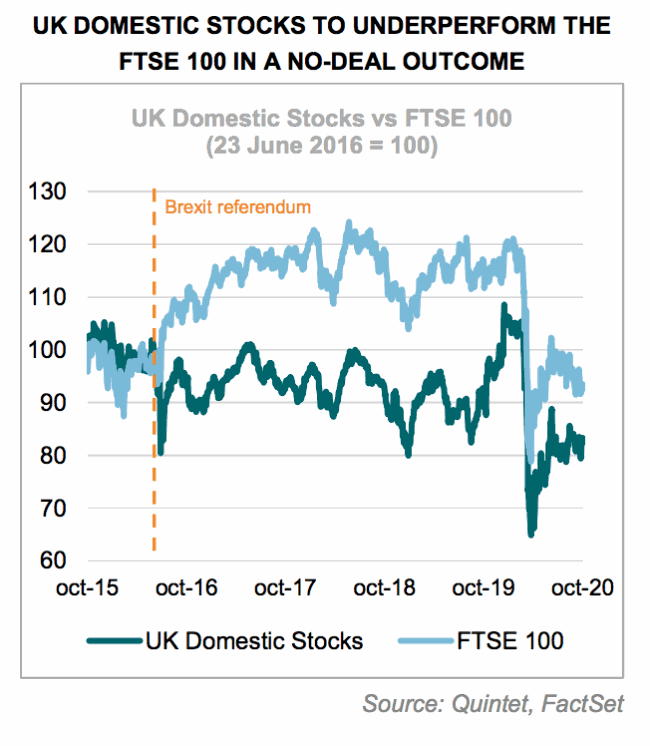

UK domestic stocks would be particularly exposed to a no-deal outcome as they’re sensitive to any negative implications for growth from uncertainty. Large UK companies tend to be among the most global corporates. FTSE 100 index constituents generate just about a quarter of their total revenues from the UK. In the wake of further sterling weakness, we would expect the FTSE 100 to perform better than the more domestic FTSE 250 – as it did in the immediate aftermath of the Brexit referendum. UK domestic stocks – those with a high proportion of UK domestic sales – are likely to lag to an even greater extent and for a longer period of time, again repeating what happened after the Brexit referendum in 2016.

To be clear, the differences between a deal and a no-deal outcome aren’t as big as they were immediately after the UK decided to leave the EU in 2016 and just before the original Brexit deadline of March 29, 2019. That’s partly because leaving the EU’s single market and customs union makes this Brexit a relatively ‘hard’ one. But it’s also because the Withdrawal Agreement has established the terms of the break-up; both the UK and the EU have made some progress in granting financial services equivalence; and the UK has already replicated parts of the trade deals it had with non-EU countries via the EU. After all, what’s often missed is that there are many types of no deals. What’s not priced in financial markets is if the UK and the EU go through a particularly tough break-up.

COVID-19 WATCH

Globally confirmed cases of Covid-19 have now increased to almost 35 million, up from nearly 33 million seven days previously.

With the virus outbreak spreading again in Europe and not yet under control in the US, we expect the pace of economic improvement to slow – both in absolute terms and relative to expectations. Our narrative has been one of an incomplete recovery from the onset. It’s one thing to recover strongly from an economy that a full lockdown has closed completely. Another is to continue to grow at that pace for an extended period of time once activity resumes after reopening.

However, what’s new here is that the latest measures to contain the spread of Covid-19 are slowing economic activity. For example, real-time data on restaurant bookings show a loss of momentum in Germany and the UK, and that the US hasn’t really gained much momentum in this particular area of spending to begin with. A cross-check of this information with other high-frequency and timely indicators confirms that some services are on a path of deceleration – which we think will prove temporary – while manufacturing remains relatively solid.

The good news is that so far the deceleration seems relatively mild, perhaps reflecting differences in the demographic composition of the second wave, which is now mostly impacting the more resilient, younger groups. Conversely, more vulnerable segments of the populations appear to have been affected to a lesser degree this time around. Our expectation is that Q4 should show positive economic growth, but not as strongly as our predicted rebound in Q3.

We believe that activity looks set to hit a speedbump in Q4 this year, as containment measures to mitigate the spread of Covid-19 constrain services activity, and rising uncertainty – partly political in nature – impacts sentiment and expenditure. However, we still expect overall economic growth to reach escape velocity over a multi-quarter, cyclical horizon. This means that, progressively, it will likely become less reliant on public-sector support and more self-sustained, with consumer spending and corporate investment playing a bigger role.

Daniele Antonucci - Chief Economist & Macro Strategist

Bill Street - Group Chief Investment Officer

This document has been prepared by Quintet Private Bank (Europe) S.A. The statements and views expressed in this document – based upon information from sources believed to be reliable – are those of Quintet Private Bank (Europe) S.A. as of October 5, 2020, and are subject to change. This document is of a general nature and does not constitute legal, accounting, tax or investment advice. This document does not provide any individual investment advice and an investment decision must not be based merely on the information and data contained in the document. All investors should keep in mind that past performance is no indication of future performance, and that the value of investments may go up or down. Changes in exchange rates may also cause the value of underlying investments to go up or down. Copyright © Quintet Private Bank (Europe) S.A. 2020. All rights reserved.