All eyes are on Europe this summer. It’s one of the most visited regions, time and again, by tourists from all around the globe. The European Football Championship also kicked off last week in Germany, the Summer Olympics in Paris starts next month and, for those more politically minded, we just had the European elections and there are key national elections in France and the UK on the horizon (and, Europe aside, the all-important US election in November).

In our 2024 Investment Outlook, I talked about this being a year of two halves. Slowing growth and easing inflation in the first half, followed by mid-year rate cuts and a gradual recovery in the second half of the year. That’s just what happened in Europe, although growth didn’t slow to the recessionary levels we initially envisioned. I also spoke about an asynchronous interest rate-cutting cycle in the West, with the US Federal Reserve (Fed) leading the way as inflation was moderating more markedly in 2023. However, US growth has been surprisingly resilient (though beginning to slow more recently), causing inflation to be slightly stickier than expected. The asynchronous rate-cutting cycle has started, but it’s the European Central Bank (ECB) leading the way, with the Fed lagging and the Bank of England (BoE) somewhere in the middle.

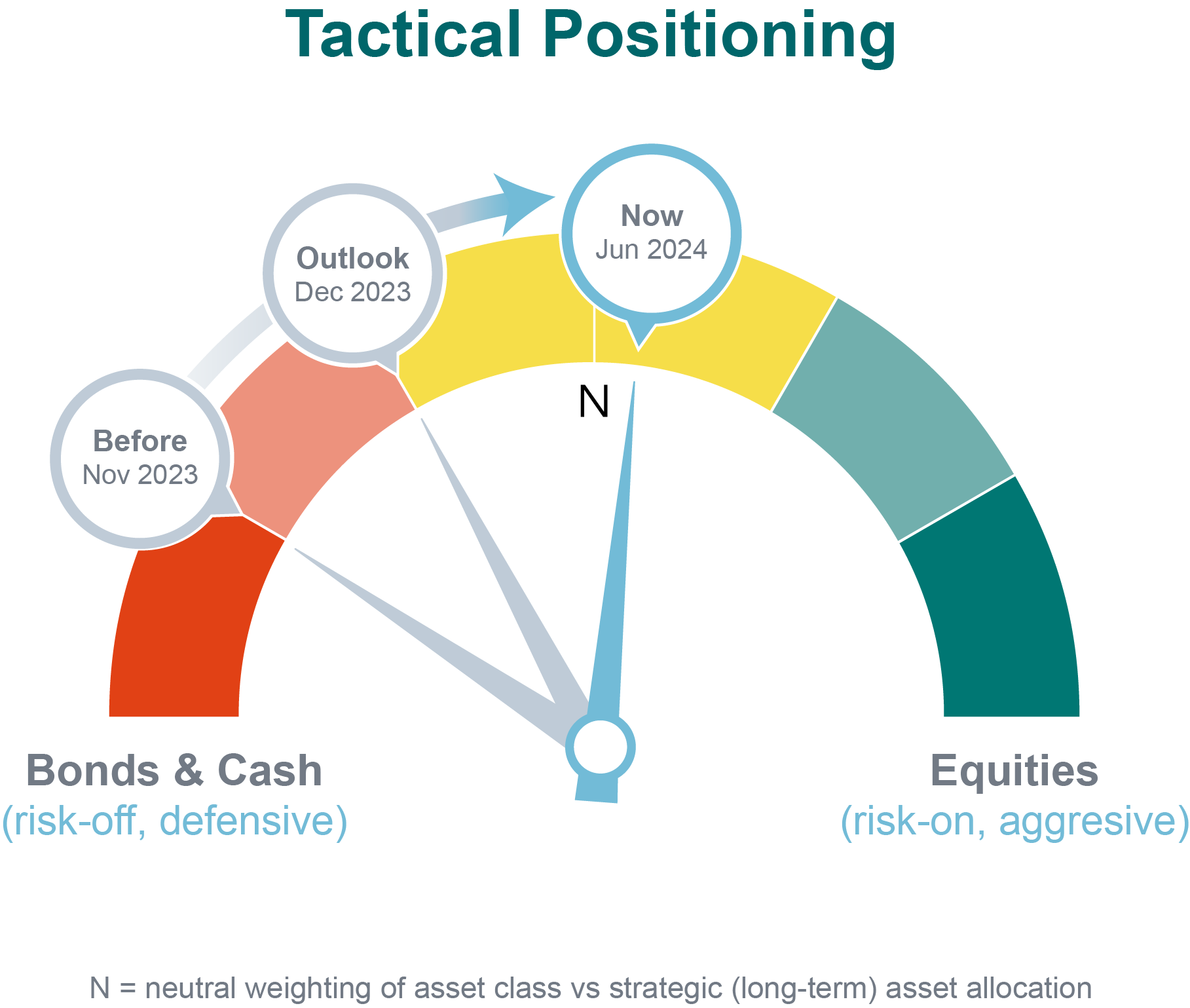

What did this all mean for portfolios? Active portfolio management is one of the core pillars of our investment philosophy. So, when the market environment changes, we adapt. We thought there was a high probability that Europe would go into recession but also that, as inflation slowed, interest rate cuts would remove a significant headwind to markets. This is why we moderated our defensive positioning in portfolios back in December 2023 and bought slightly more equities. Inflation did slow, but growth stayed resilient. So, we thought the outlook for equities was likely to improve. This led us to buy even more equities to a point where we now own slightly more compared to our long-term strategic allocation (we’re ‘overweight’ equities).

Daniele Antonucci

Co-Head of Investment & Chief Investment OfficerOur view for the next six months

This brings us to our Mid-Year Outlook. Just because we’ve reached the middle of the year, it’s no reason to rip everything up and start again with a new view. Instead, we simply adapt to today’s market environment, attempting to anticipate what may come next. We see a continuation of our 2024 Investment Outlook: interest rate cuts remove a headwind for growth, and the economic outlook improves.

We expect three key trends:

- A recession is unlikely over the next 6-12 months. More likely is a US ‘soft landing’ (slower but positive growth), a gentle acceleration in the Eurozone/UK, and some stabilisation in China.

- The Eurozone and the UK have room to grow better than the markets expect, and we’ve revised our forecasts to above consensus.

- The Fed should cut less and later than the ECB/BoE. We expect an asynchronous rate-cutting cycle: one or two Fed cuts at year-end vs two or three ECB/BoE cuts from mid-year.

Maintaining equity and fixed-income convictions

In our May Counterpoint, we said that we sold European bonds and bought European equities given the forthcoming economic improvement we saw and relatively attractive European equity valuations. This investment meant that we turned slightly ‘overweight’ equities (owning more compared to our long-term strategic asset allocation), though not yet for Europe, where we still remain somewhat underweight.

Fundamentally, the case for adding exposure to this region is growing, for quite a few reasons:

- Inflation in the Eurozone has been steadily decreasing since its peak in October 2022, at over 10%.

- Now, inflation is nearing the ECB’s 2% target and the central bank cut rates for the first time in five years.

- We believe interest rate cuts remove a major headwind for economic growth and equities. In the absence of a recession, history shows that interest rate cuts could boost equities.

- We expect one or two more rate cuts from the ECB this year, which could provide further support to the economy and markets.

So, given our view that there’s a higher probability of a recovery than a recession in Europe, adding to European equities would be a logical next step. Why not now, then? Because we think uncertainty prior to the French election is likely to increase. Therefore, even though the fundamental case for Europe looks more compelling to us than it was a few months ago, we maintain our somewhat reduced exposure at this stage. We will look for opportunities once the uncertainty clears and we get greater clarity on the European policy outlook.

Elsewhere in equities, back in February, we added a position in global small-cap equities as we believed equities had a more balanced risk-reward at the time, given the lower probability of recession in the US. Global small caps have performed well since then, and valuations remain attractive. At the same time, we’re looking at the timing of Fed rate cuts and the US economic outlook, which are important drivers for this asset class.

In fixed income, while valuations for European investment grade bonds have become somewhat more demanding, our exposure to this asset class remains higher vs our long-term allocation. This is because we like the yield these bonds offer. The ECB rate-cutting cycle in an improving economy could be supportive, too. Conversely, high-yield bonds are still pricing in a better economic backdrop than our base case, so we’re keeping a reduced exposure.

What to make of the European and French elections

We’re also maintaining the ‘insurance’ we purchased earlier this year in our flagship portfolios and those where client knowledge and experience, and regulations, permit. This is an instrument that, under certain conditions, appreciates in value if there is an equity drawdown relative the purchase level, partially offsetting any negative performance (the value of the instrument goes up as the value of our equity portfolio goes down). To be clear, we’re not expecting an equity drawdown. However, there are lingering risks to equity markets, including potential volatility associated with the US election in November and any bouts of unexpected geopolitical concerns. Think of this like any other insurance: you don’t think your house is going to fall down, but you buy insurance just in case as it’s inexpensive relative to the cost of rebuilding your house.

This strategy, along with our underweight on European equities, could also help if European political events were to cause significant market volatility. While the fundamental case for Europe is stronger, the increase in political uncertainty suggests that investors shouldn’t be complacent at this stage. The European and French elections, depending on their ramifications, could potentially have a near-term knock-on effect on investor sentiment and, perhaps more importantly, long-term effects that are relevant for markets. This could include a lesser commitment to certain environmental sustainability and European integration and fiscal themes such issuing again ‘Eurobonds’ backed by all countries, less fiscal prudence in some countries, or even a less coordinated response to geopolitical challenges.

Adaptation, not overhaul

Earlier in this piece, I spoke about active management being a key pillar in our investment philosophy. In fact, I’ve written a whole blog on the importance of this pillar, which you can read here. However, investing isn’t all about implementing tactical tweaks. The bulk of portfolio returns are generated by the so-called strategic asset allocation – the long-term anchor from which you make your tactical tweaks. This is the foundation of our globally-diversified, multi-asset portfolio, which holds the QMM Fund Range we co-created with BlackRock, a variety of other funds, our global direct equity and sovereign bond portfolios, commodities and cash.

The point I’m making here is that, while we believe our tactical tilts will benefit portfolio performance, they will likely be a smaller contributor to performance than our strategic asset allocation. To put this into perspective, since the start of the year, our strategic asset allocation has delivered almost all the positive performance in our flagship portfolios, which is often the case. The single greatest exposure in our strategic asset allocation is US equities, reflecting longer-term megatrends in areas such as artificial intelligence, and the overall quality and growth of that market.

Some of our tactical positions earlier this year have aimed to protect portfolios against the heightened volatility that might possibly come from geopolitical events and elections. Put very simplistically (and to squeeze in another football reference here), in 2024, think of the strategic asset allocation as your attacking players and the tactical tweaks as your goalkeeper and defenders. That’s not the case all the time. Sometimes your defenders will charge up the pitch and score goals themselves.

Regardless of the interaction of the different parts of our portfolios, we stay true to our aim of protecting and growing our clients’ wealth. While we now own slightly more equities than bonds relative to our long-term allocation, we retain a mix of positions that helps mitigate downside risks (should they materialise). Plus, we think our approach of global diversification, of ‘not putting all eggs in one basket’, reduces volatility and delivers more resilient outcomes by mitigating the impact of local events including geopolitics and elections, and spreading investments across multiple regions and asset classes driven by different risk and return factors.

If you want to discuss your portfolio positioning or learn more about the QMM Fund Range, your Client Advisor will be happy to help.

Always there for you wherever you are

At Quintet, we pride ourselves on being small enough to really get to know you, yet big enough to give you easy access to the best the world of finance has to offer. Whatever your needs, we will provide objective insights, advice, products and services tailored to your personal goals. And with offices in 30+ cities across Europe and the UK we are always there for you wherever you are. Why not come and talk with us today?

This document is designed as marketing material. This document has been composed by Quintet Private Bank (Europe) S.A., a public limited liability company (société anonyme) incorporated under the laws of the Grand Duchy of Luxembourg, registered with the Luxembourg trade and company register under number B 6.395 and having its registered office at 43, Boulevard Royal, L-2449 Luxembourg (“Quintet”). Quintet is supervised by the CSSF (Commission de Surveillance du Secteur Financier) and the ECB (European Central Bank).

This document is for information purposes only, does not constitute individual (investment) advice and investment decisions must not be based merely on this document.

Whenever this document mentions a product, service or advice, it should be considered only as an indication or summary and cannot be seen as complete or fully accurate. All (investment) decisions based on this information are at your own expense and at your own risk. It is up to you to (have) assess(ed) whether the product or service is suitable for your situation. Quintet and its employees cannot be held liable for any loss or damage arising out of the use of (any part of) this document. All copyrights and trademarks regarding this document are held by Quintet, unless expressly stated otherwise. You are not allowed to copy, duplicate in any form or redistribute or use in any way the contents of this document, completely or partially, without the prior explicit and written approval of Quintet. See the privacy notice on our website for how your personal data is used (https://www.quintet.com/en-gb/gdpr).

The contents of this document are based on publicly available information and/or sources which we deem trustworthy. Although reasonable care has been employed to publish data and information as truthfully and correctly as possible, we cannot accept any liability for the contents of this document.

Investing involves risks and the value of investments may go up or down. Past performance is no indication of future performance. Any projections and forecasts are based on a certain number of suppositions and assumptions concerning the current and future market conditions and there is no guarantee that the expected result will ultimately be achieved. Currency fluctuations may influence your returns.

The information included is subject to change and Quintet has no obligation after the date of publication of the text to update or inform the information accordingly.

Copyright © Quintet Private Bank (Europe) S.A. 2024. All rights reserved. Privacy Statement