Investing Through Structural Change: Opportunities at the Intersection of Growth and Sustainability

10 mins to read this article

The global economy is entering a new phase shaped by structural rather than cyclical forces, with the investment landscape becoming more fragmented, multi-polar and thematically driven. In this environment, long-term returns are likely to be generated less by broad market exposure and more by targeted positioning in transformative trends, many of which are closely linked to sustainability.

Four interconnected forces stand out: technological disruption, the energy transition, geopolitical realignment, and demographic change. Together they are reshaping supply chains, capital flows and corporate profitability, and creating new investment opportunities across regions and asset classes.

Artificial Intelligence: A Productivity Revolution with an Energy Constraint

Artificial intelligence (AI) is emerging as a general-purpose technology comparable to electrification or the internet, capable of reshaping entire economies over decades. The scale of capital expenditure on data centres, semiconductors and cloud infrastructure suggests that this is not a short-term hype cycle, but a structural shift supported by strong corporate earnings and cash flows.

However, AI’s growth is inseparable from energy availability. Training and operating advanced models require enormous computing power and electricity, making reliable and low-carbon energy infrastructure a critical bottleneck. The outlook highlights that AI adoption must advance alongside the energy transition, including renewables, nuclear power, grid modernisation and storage solutions.

This creates a powerful investment nexus:

- Technology leaders enabling AI deployment

- Utilities and grid operators expanding capacity

- Renewable developers and nuclear providers

- Energy storage and transmission infrastructure

- Semiconductor supply chains

Importantly, the benefits of AI are not confined to technology companies. Productivity gains are expected across sectors including healthcare, manufacturing, logistics and finance, creating broad-based opportunities for companies able to deploy AI effectively.

The Energy Transition: Infrastructure, Electrification and Capital Intensity

The transition toward low-emission energy systems is one of the largest investment programmes in modern history. Estimates suggest trillions of dollars annually will be required to build renewable generation, grids, batteries and energy-efficient infrastructure1.

Electrification is the common thread linking multiple sectors, such as transportation (electric vehicles), industry (electrified processes), buildings (heat pumps and efficiency upgrades), digital infrastructure (data centres).

For investors, this transition favours companies involved in the following: Renewable energy production, grid expansion and smart networks, energy storage technologies, electrification equipment and materials, energy efficiency solutions.

It also reinforces the importance of infrastructure investing, both public and private, as governments alone are unlikely to finance the required scale of development.

Commodities and Critical Materials: The Foundations of Decarbonisation

A frequently overlooked implication of the energy transition is the surge in demand for raw materials. Renewable technologies, batteries and electrification rely heavily on metals such as copper, lithium, nickel and rare earth elements.

At the same time, geopolitical fragmentation is increasing the strategic importance of secure supply chains. Countries and regions are prioritising resource independence, recycling and domestic production to reduce reliance on external suppliers.

This dynamic supports several investment areas:

- Mining companies focused on transition metals

- Recycling and circular-economy businesses

- Processing and refining capacity

- Resource-efficient manufacturing technologies

Sustainability considerations are critical here: investors are increasingly differentiating between producers based on environmental practices, labour standards and governance.

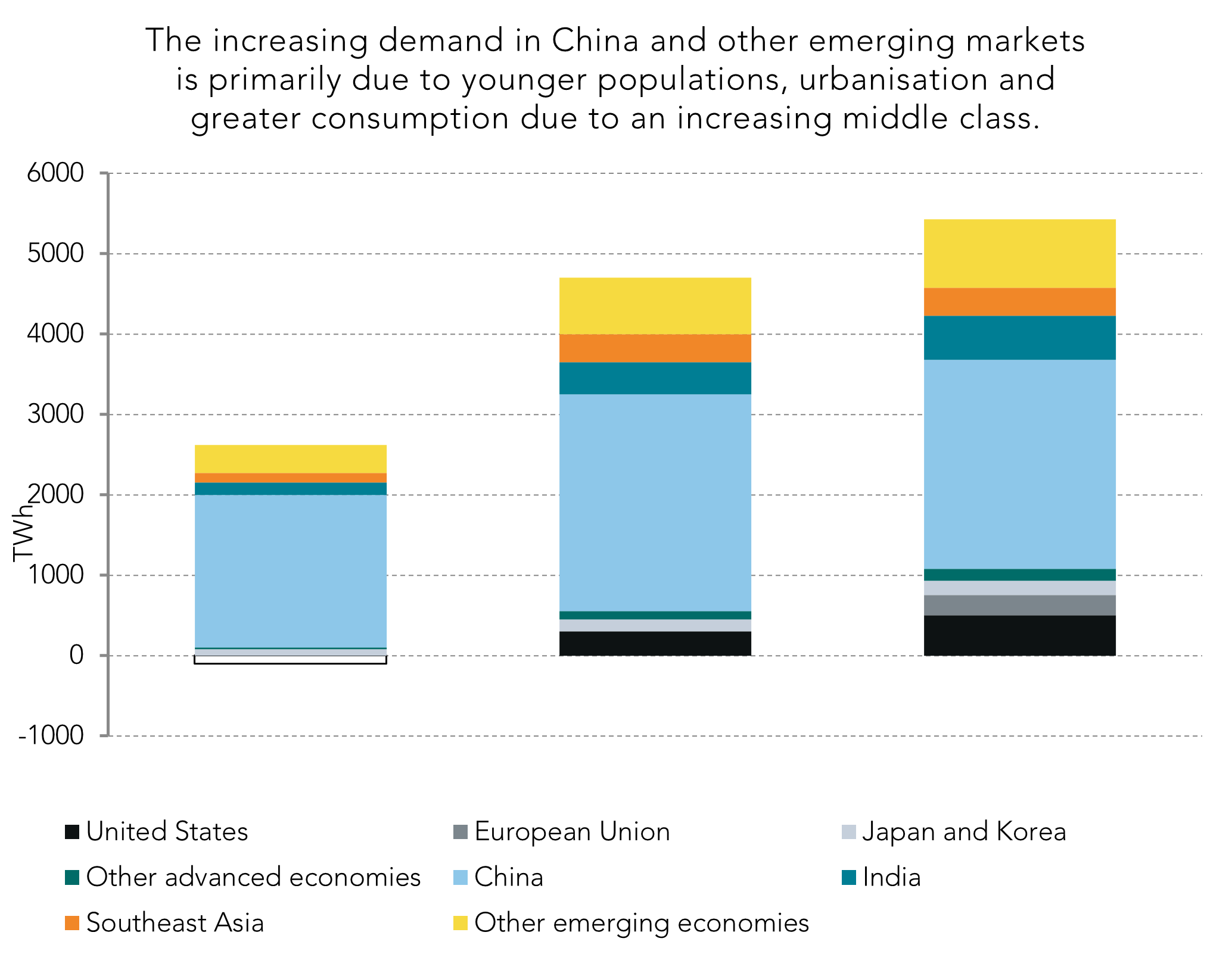

Emerging Markets: Growth, Demographics and Consumption

From a long-term perspective, emerging markets (EM) stands to benefit from structural shifts in both global growth and sustainability. Younger populations, urbanisation and rising middle classes support long-term consumption trends, while infrastructure development drives demand for energy, transportation and digital connectivity.

Source: IEA

A weaker US dollar, not now given elevated geopolitical uncertainty but over longer horizons as EM central banks and investors refocus their currency exposure away from the dollar, and supportive domestic policies can also improve capital flows and economic conditions in EM economies.

From a sustainability perspective, EM plays a dual role:

- Demand centre — growing energy needs from electrification of industries and consumption from an increasing middle class are increasing electricity demand.

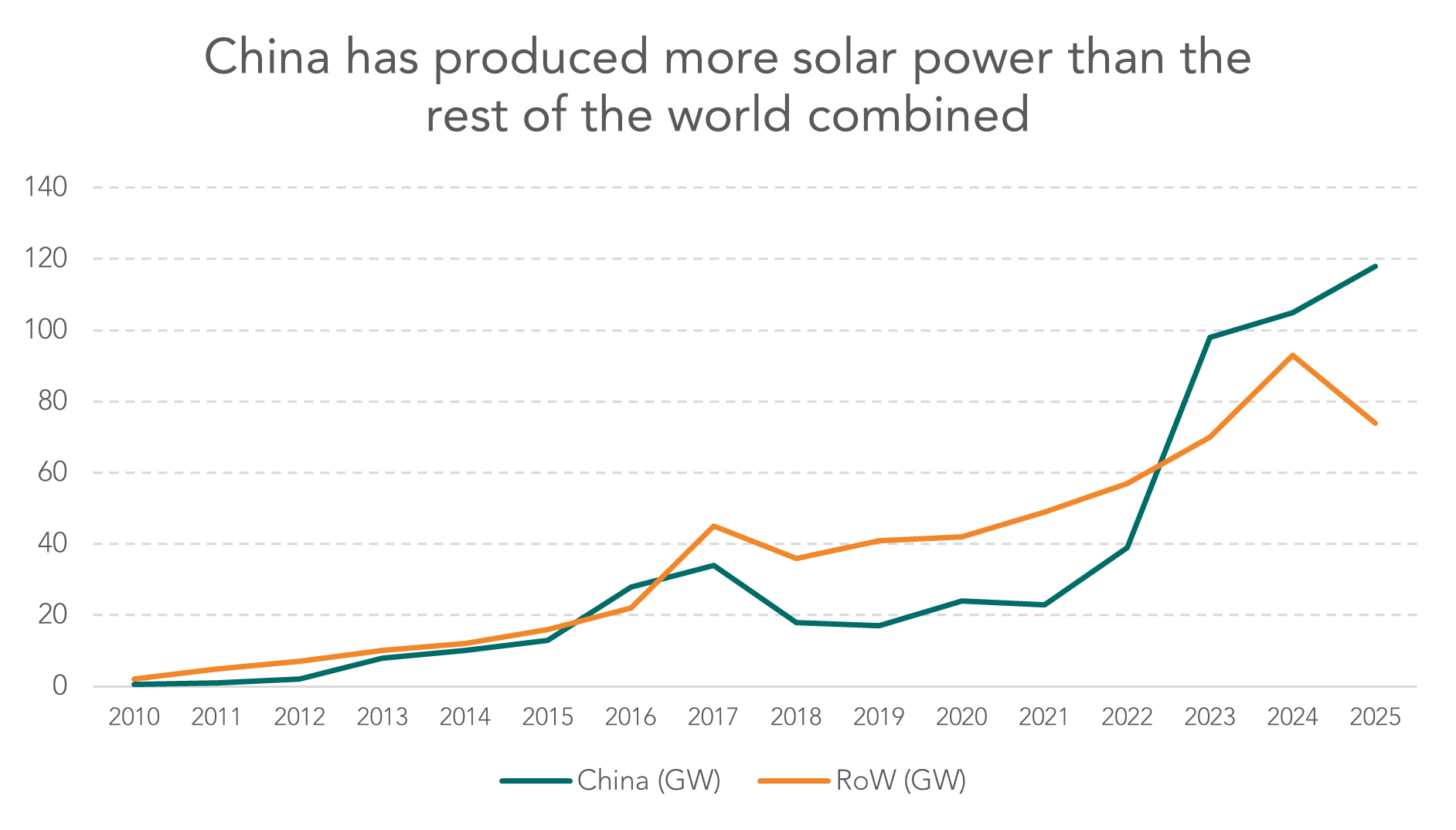

- Solution provider —EM plays a key role in the development of renewable deployment, resource supply and manufacturing. For example, China alone has added more solar capacity for generating solar than the rest of the world combined (with panels designed and manufactured in China).

Source: Global energy monitor

Opportunities include:

- Renewable expansion in fast-growing economies

- Sustainable infrastructure development

- Financial inclusion and digitalisation

- Consumer sectors benefiting from income growth

Europe’s Strategic Reorientation: Self-Sufficiency and Resilience

Europe is repositioning itself for a more fragmented world by investing in energy independence, infrastructure, defence and technological capability. This reflects a broader shift from efficiency-driven globalisation toward resilience and strategic autonomy.

Key investment areas include:

- Clean energy and grid modernisation

- Defence and cybersecurity

- Industrial innovation

- Healthcare and life sciences

- Circular-economy initiatives

Europe’s emphasis on sustainability regulation and resource efficiency may also support companies positioned to benefit from stricter environmental standards and repair-oriented product design.

Private Markets: Financing the Real Economy

Private markets continue to expand, offering a growing range of investment opportunities. As highlighted in our outlook many of the most capital-intensive sustainability projects - infrastructure, energy systems, logistics networks - are being developed outside public markets. Private equity, private debt and infrastructure funds provide access to these long-duration assets.

The outlook emphasises that structural forces such as decarbonisation, digitisation, demographics and deglobalisation are particularly visible in private markets.

Conclusion: Sustainability as a Driver of Returns, not a Constraint

Sustainability is no longer a niche consideration but a central organising principle of the global economy. The transition to cleaner energy, digital infrastructure, resilient supply chains and ageing societies requires unprecedented capital investment, creating long-term opportunities across public and private markets.

Successful investing in this environment means identifying where structural growth, policy support and sustainability objectives intersect. Rather than treating ESG factors as exclusions, investors can view them as signals of where future demand, regulation and innovation are likely to concentrate.

In a world of clearer skies but persistent uncertainty, portfolios anchored in these enduring themes may be best positioned to deliver both financial returns and long-term resilience.

This document is designed as marketing material. This document has been composed by Quintet Private Bank (Europe) S.A., a public limited liability company (société anonyme) incorporated under the laws of the Grand Duchy of Luxembourg, registered with the Luxembourg trade and company register under number B 6.395 and having its registered office at 43, Boulevard Royal, L-2449 Luxembourg (“Quintet”). Quintet is supervised by the CSSF (Commission de Surveillance du Secteur Financier) and the ECB (European Central Bank).

This document is for information purposes only, does not constitute individual (investment) advice and investment decisions must not be based merely on this document.

Whenever this document mentions a product, service or advice, it should be considered only as an indication or summary and cannot be seen as complete or fully accurate. All (investment) decisions based on this information are at your own expense and at your own risk. It is up to you to (have) assess(ed) whether the product or service is suitable for your situation. Quintet and its employees cannot be held liable for any loss or damage arising out of the use of (any part of) this document. All copyrights and trademarks regarding this document are held by Quintet, unless expressly stated otherwise. You are not allowed to copy, duplicate in any form or redistribute or use in any way the contents of this document, completely or partially, without the prior explicit and written approval of Quintet. See the privacy notice on our website for how your personal data is used (https://www.quintet.com/en-gb/gdpr).

The contents of this document are based on publicly available information and/or sources which we deem trustworthy. Although reasonable care has been employed to publish data and information as truthfully and correctly as possible, we cannot accept any liability for the contents of this document.

Investing involves risks and the value of investments may go up or down. Past performance is no indication of future performance. Any projections and forecasts are based on a certain number of suppositions and assumptions concerning the current and future market conditions and there is no guarantee that the expected result will ultimately be achieved. Currency fluctuations may influence your returns.

The information included is subject to change and Quintet has no obligation after the date of publication of the text to update or inform the information accordingly.

Copyright © Quintet Private Bank (Europe) S.A. 2026. All rights reserved. Privacy Statement