Our scorecards for emerging markets highlight where fundamentals are resilient and where they’re not. These measures are especially important if bond yields overshoot their forecasts

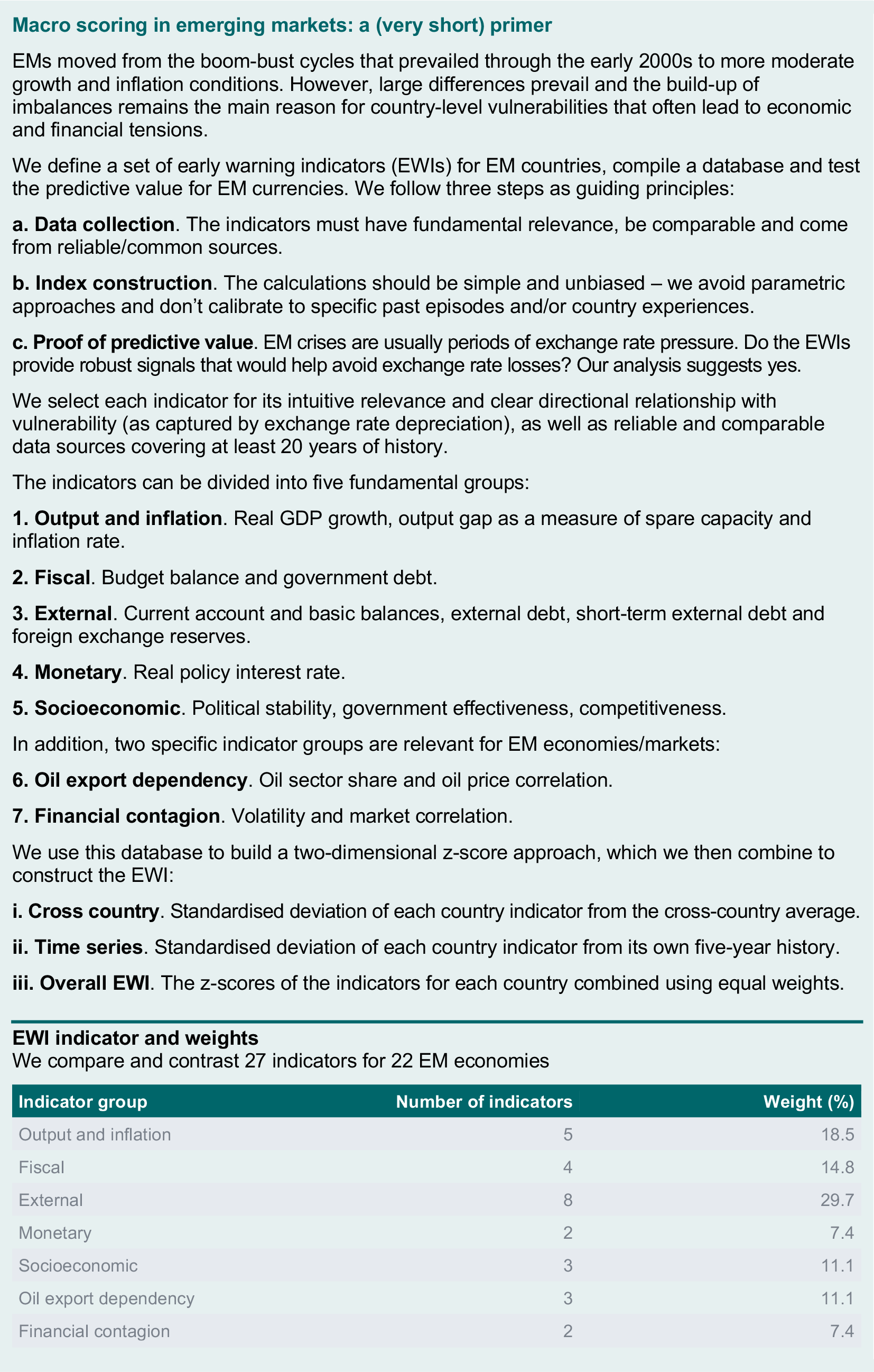

- We compile a large macro-financial dataset on emerging markets: 22 economies and 27 indicators describing different key aspects covering at least 20 years of history.

- We use this information to build a scoring model that compares and contrasts different macroeconomic factors and other dimensions, combining them in a single Early WarningIndicator (EWI): a ranking of emerging markets based on relative strengths and weaknesses.

- Currently, the EWI suggests that the Asian economies we track, including China, South Korea, Taiwan, Malaysia and Thailand, have the strongest fundamentals, together with Poland and the Czech Republic.

- Several (but not all) Latin American economies, including Brazil, Argentina and Colombia, along with Turkey, Romania, Russia and South Africa, appear more vulnerable, showing a range of structural and financial imbalances.

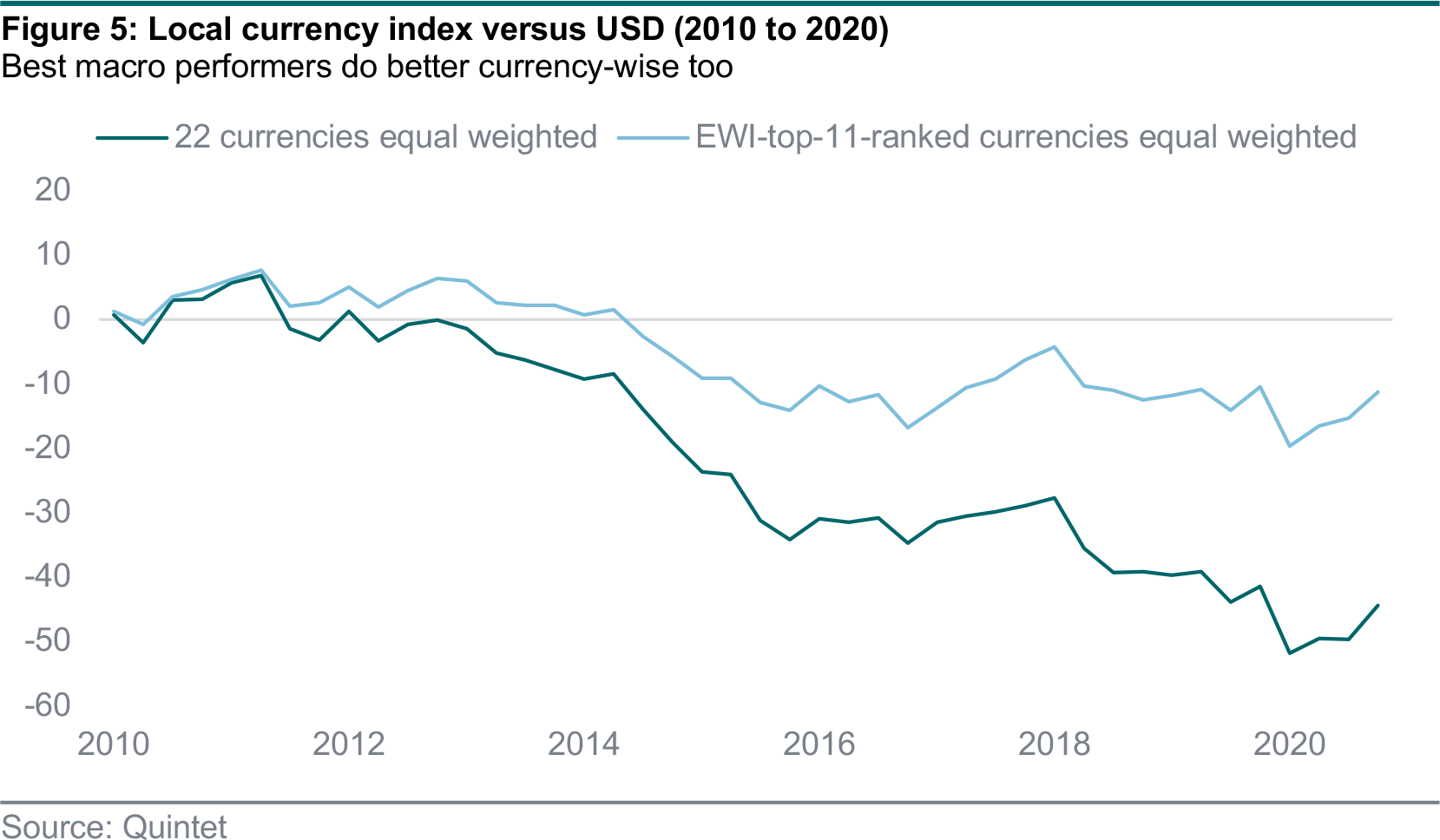

- We show that our EWI captures financial stress, as proxied by currency depreciation. Our simulation shows that a portfolio of currencies scoring highly in the macro and financial ranking would outperform one made of those scoring poorly.

- We believe that the rise in US yields is happening because of an improving global outlook of stronger growth and temporarily higher inflation. As such, we think it’s a positive for markets, especially as we don’t expect central banks to hike rates for now.

- Although a pickup in world trade is an offset mainly for Asia, and rising commodity prices help more generally, a potential yield spike is a risk for some emerging markets.

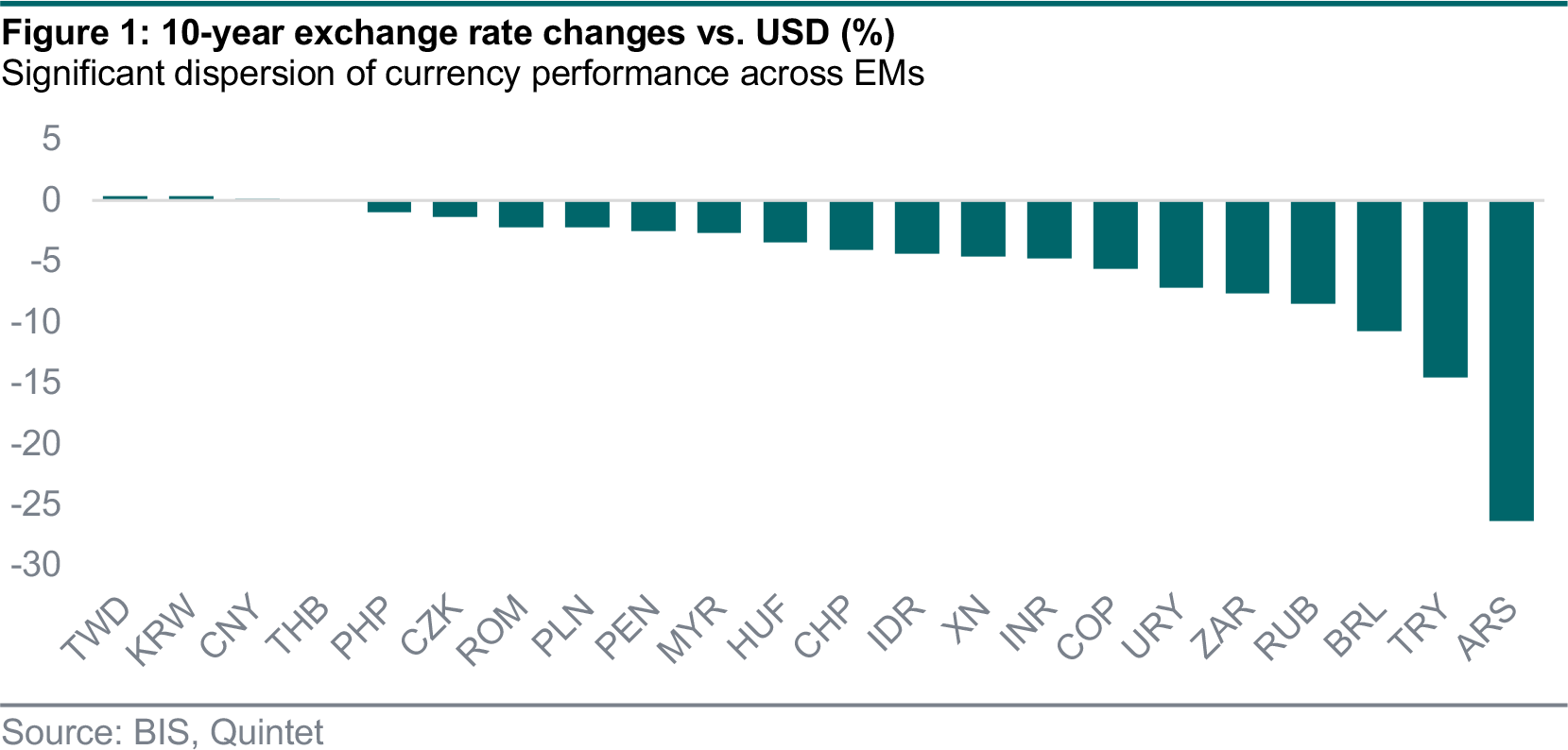

Investors tend to assign more or less importance to different parts of the emerging market (EM) narrative. After all, their fundamentals, as reflected in relative currency performance, appear heterogeneous. Some emphasise the economic cycle (the ‘growth’ story), others imbalances such as high debt levels or structural themes ranging from reform and competitiveness to political stability (or lack thereof). We can do better by combining all these dimensions in a single scorecard ranking the EMs we track across many metrics and overall.

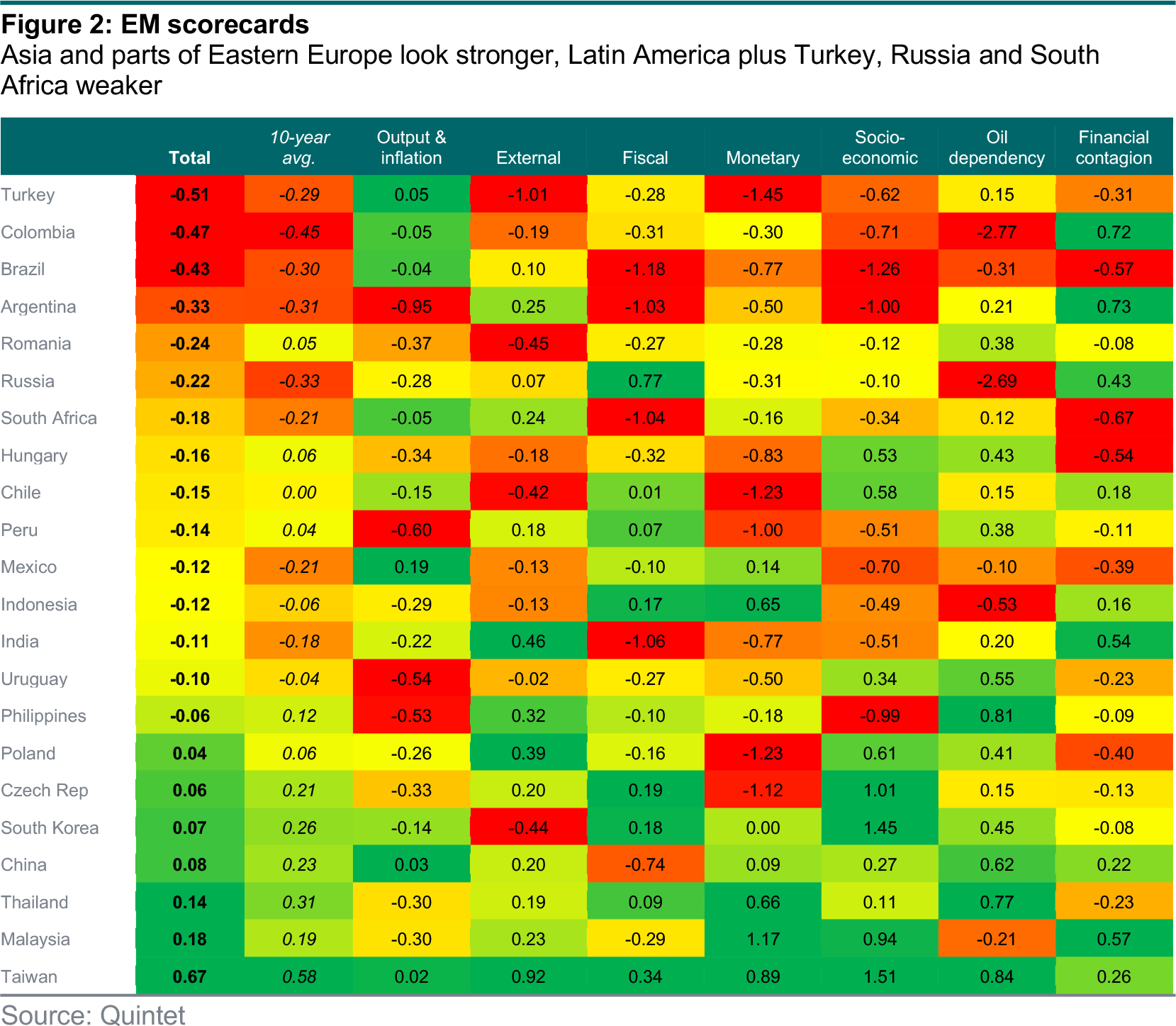

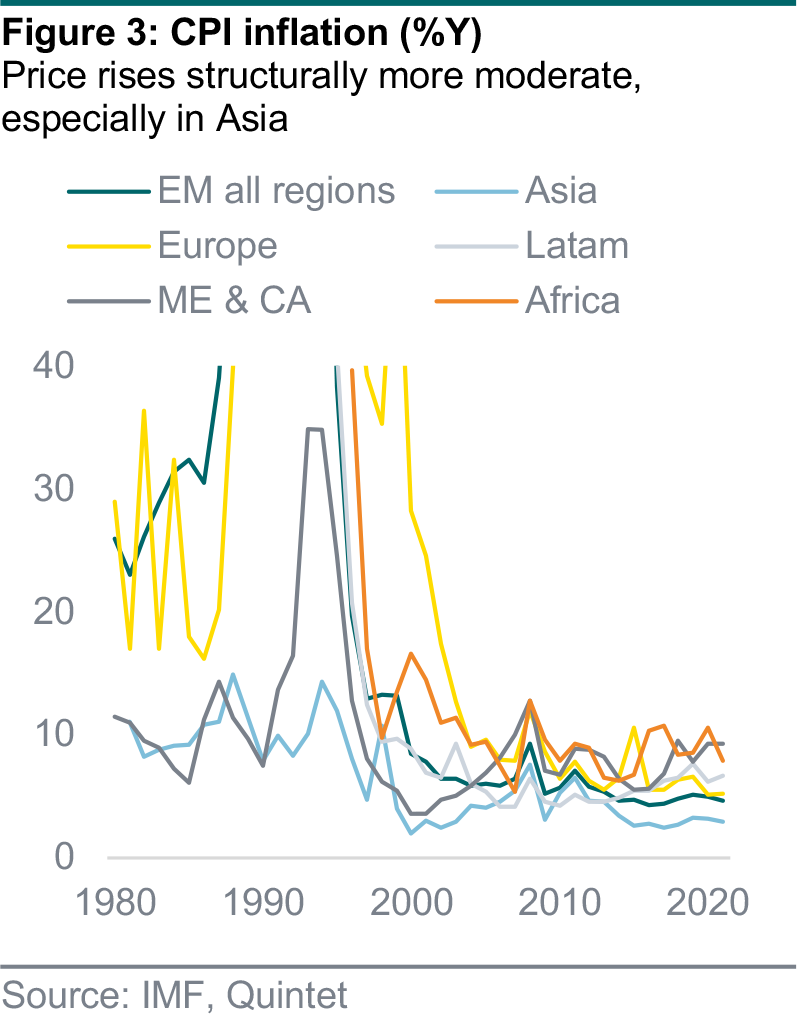

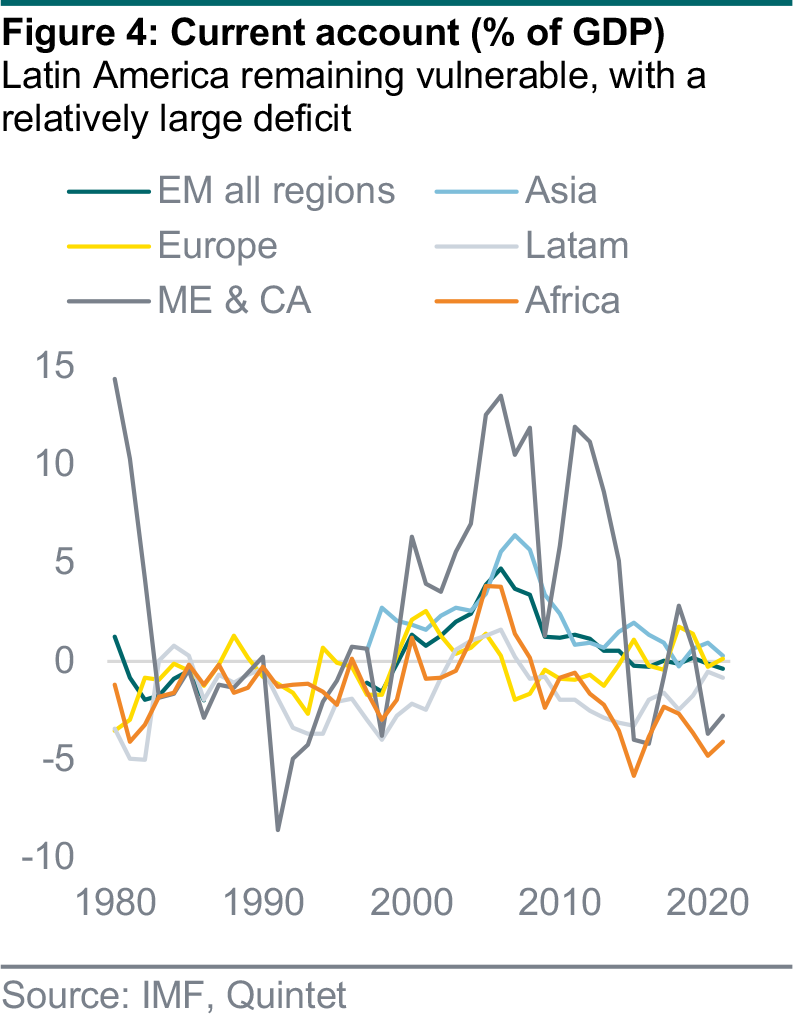

Aggregating the individual country scores gives us the following ranking: the most vulnerable EMs, among those we track, are typically Latin America plus Turkey, Romania, Russia and South Africa. This is mainly because of weak scores across a range of dimensions apart from output growth and inflation – especially on socioeconomic indicators but also more generally, with significant imbalances and fragilities.

In particular, the latest trends show that:

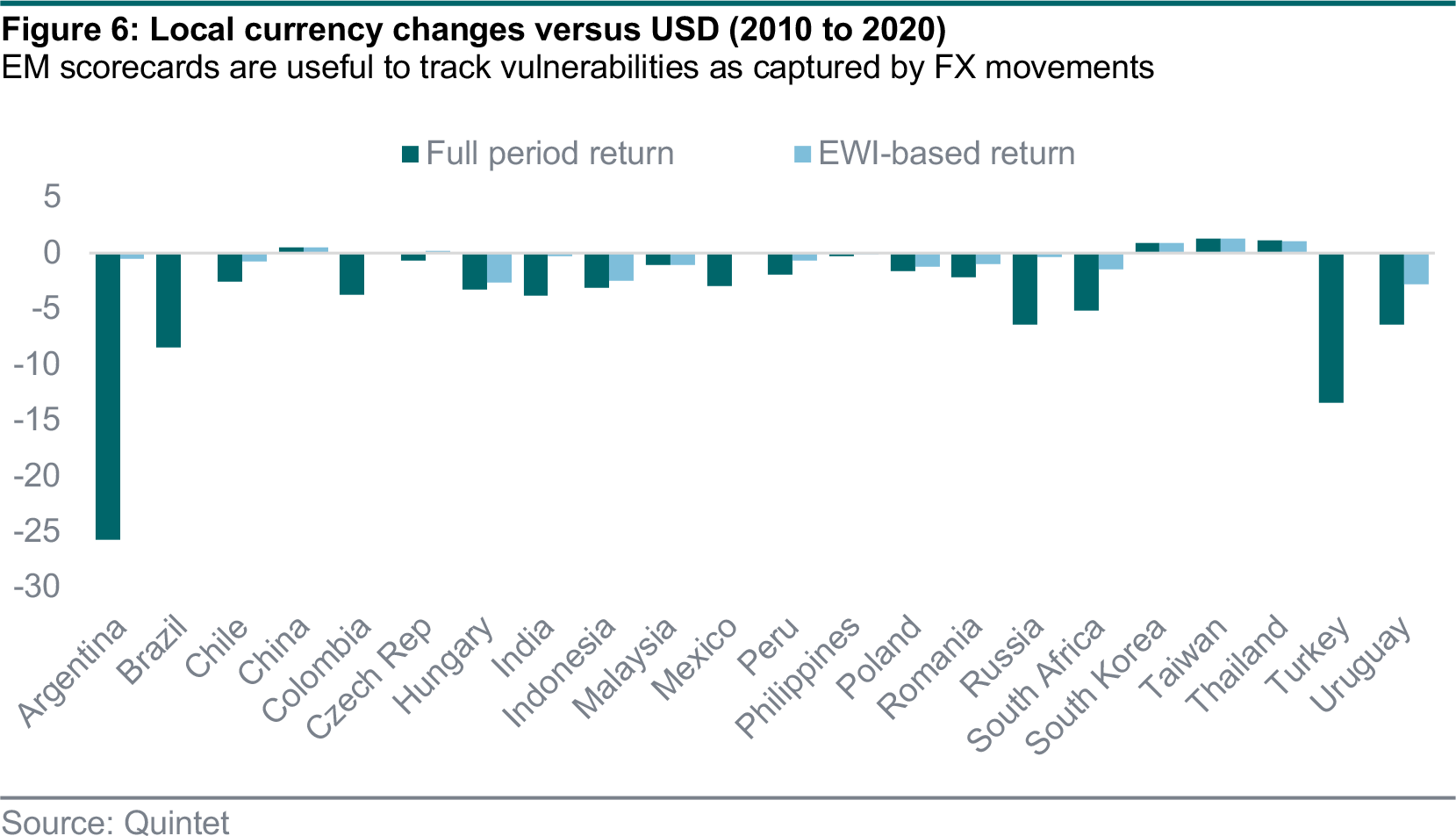

- Turkey is still the most vulnerable of the 22 countries. The Turkish Lira has done well since various changes at the helms of the central bank and the ministry of finance last November, but this isn’t yet captured by our indicator. The economy has bounced back from Covid-19, especially compared to other EM economies, but inflation is still high, current account and fiscal deficits are large and short-term external debt is high too. Against that background, real interest rates are low. Whether Turkey is really on the path of improvement isn’t clear yet.

- Argentina and Brazil remain challenged macro-wise. External balances and debt have improved, but their fiscal positions are among the weakest. Socioeconomic factors are also comparatively poor. In the case of Argentina, inflation is an additional problem. In both countries, monetary policy may be too loose. Brazil also has a high financial contagion risk.

- Colombia and Russia are primarily vulnerable because of their high dependency on oil exports. Stripping out oil would put them both more in the middle of the ranking. Arguably, rising commodity prices are helpful right now, but high dependency on just one or few commodities, over the cycle, is a vulnerability. For Colombia, the other drawback is the socioeconomic factors (political stability, government effectiveness and competitiveness).

- South Africa is also in the camp of persistently vulnerable countries, mostly due to its weak fiscal position and high financial contagion risk.

- Romania has slipped the most relative to its long-term position, mostly due to weak current account and fiscal balances.

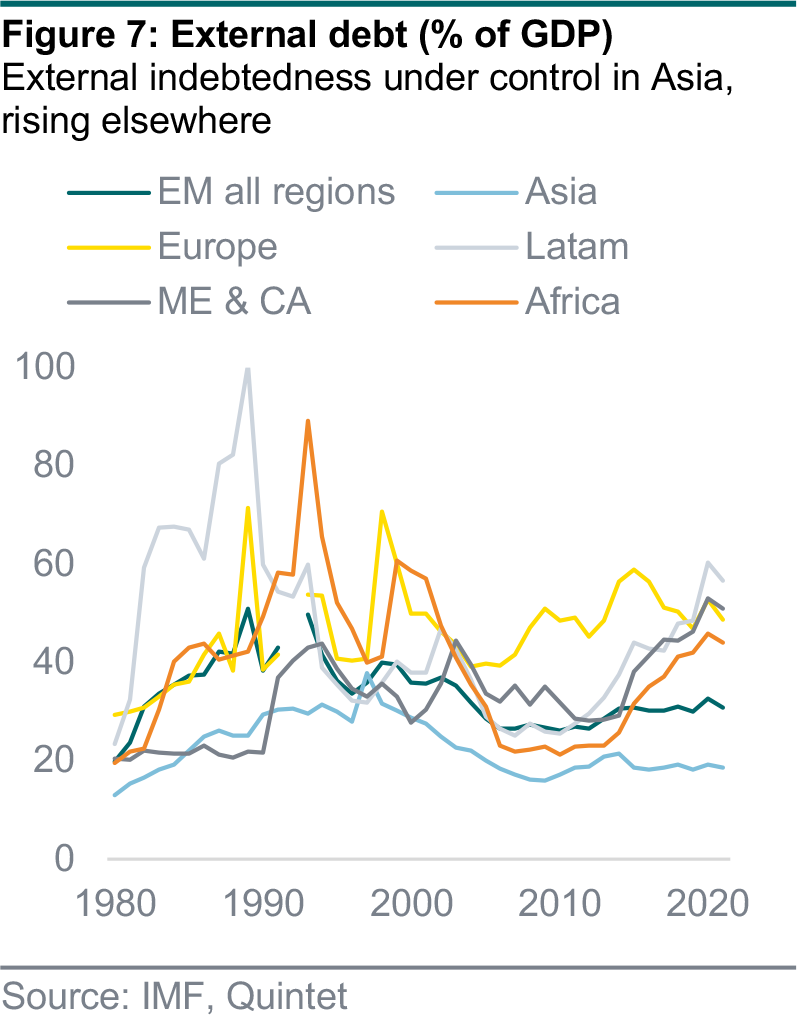

- All eight Asian economies we track are in the less vulnerable half of the ranking. Taiwan, Malaysia, Thailand, China and South Korea rank as least vulnerable. All five have no inflation and current account problems, and their monetary policy isn’t too loose. In addition, all score high in the socioeconomic category (though for different reasons).

We test the predictive value of the EWIs on FX with a portfolio simulation:

- Each quarter, dating back over the last 10 years, we divide the 22 countries in two groups: the 11 most vulnerable and the 11 least vulnerable countries:

- The indicators used for each country are based on the data known at the time of calculation (typically one to two quarters backdated); however, some ex-post revision bias can’t be excluded.

- We construct a portfolio of the 11 least vulnerable currencies using equal weights and rebalance the FX portfolio every quarter.

- Calculation of quarterly FX returns are based on pure spot (no carry), as we want to capture financial stress via currency changes.

- We compare the resulting return series of the rolling top 11 currencies with the returns of an equal-weighted portfolio of all 22 currencies with quarterly rebalancing.

The results show that the most vulnerable countries have also experienced the largest FX losses over the past 10 years. A portfolio that avoids the 11 most vulnerable currencies based on our EWI every quarter produces substantially lower FX declines than a portfolio of all 22 currencies.

In this, admittedly illustrative, simulation, the EWI top 11 portfolio stood clear of the largest losers – Argentina, Turkey and Brazil, followed by Russia, Uruguay and South Africa, and was consistently long top performers such as China, South Korea, Taiwan and Thailand.

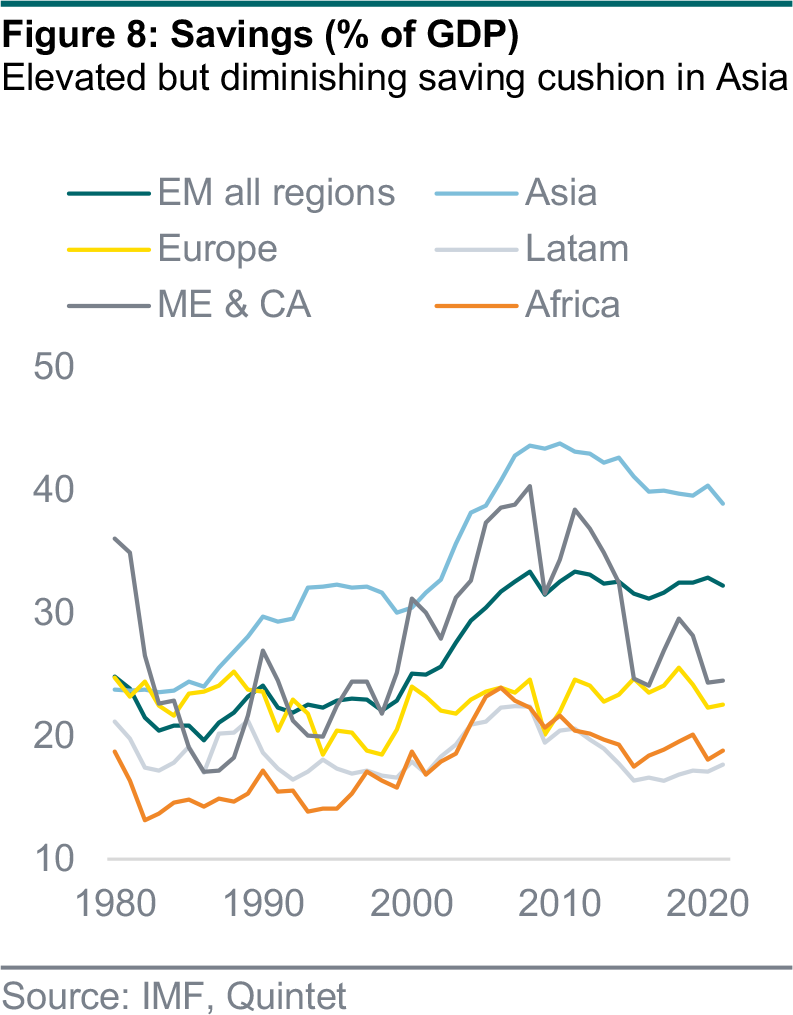

We’re often asked whether pressure on EMs is likely to increase if bond yields continue to rise. It’s normal for rates to rise as the economy does better. The problem is when higher rates tighten financial conditions for EMs with weak fundamentals, in some cases impacting markets at large. At this juncture, while rising yields make the macro case for the EM complex more nuanced, strengthening global growth and world trade (along with rising commodity prices for some EMs) do offset some of the risks, especially for the Asian countries embedded in global supply chains – also given low external debt and large economy-wide savings.

It would be one thing if our global macro forecast did envisage a major overshoot in yields. But it doesn’t. While there are perhaps more upside than downside risks, we think that ample liquidity and ‘cash on the sidelines’ will likely pull in bond demand at (modestly) higher yields. We remain bullish on breakeven inflation and, albeit temporarily, we expect inflation to rise above central bank targets over the next few months without triggering any policy rate hikes from the Fed, European Central Bank and Bank of England – at least not for the next two to three years.

Probably the most well-known example of rising yields having negative implications, at least in recent memory, is when US real yields rose 130 bps between May and July 2013, as the market worried about the removal of Fed accommodation – the so-called ‘taper tantrum’. However, the magnitude seems very different this time around. US 10-year real rates have currently risen by around 35 bps from the lows, about a quarter of the May 2013 move. Crucially, we expect the Fed’s communication on the removal of accommodation to leave less uncertainty.

Another example is May 2015. The Fed ended up hiking in December that year, but in May markets worried that rate rises were more imminent. China’s equity market was going through a full-blown boom, rising 140% to May 2015. The ensuing 43% decline led to tighter financial conditions in China, a contraction in manufacturing and a large drop in the currency. Oil prices fell over 35% that summer and 55% overall. Today, we think that the first Fed hike is still 2.5 years away. Although China’s equity market is up significantly year on year, it’s far less than in 2015. We expect the currency to appreciate in China. And we see rising oil prices too.

Still, we are not complacent about the risk of rising interest rates for emerging markets and we’re monitoring very closely the EM countries with vulnerable fundamentals – as flagged by our EWI. Rising interest rates are especially a problem for countries with external imbalances (current account deficits and high external debt) and inconsistent macro policies (easy fiscal policy and low real interest rates). Asian economies, with their high savings and relatively low debt levels, are better positioned to withstand higher interest rates.

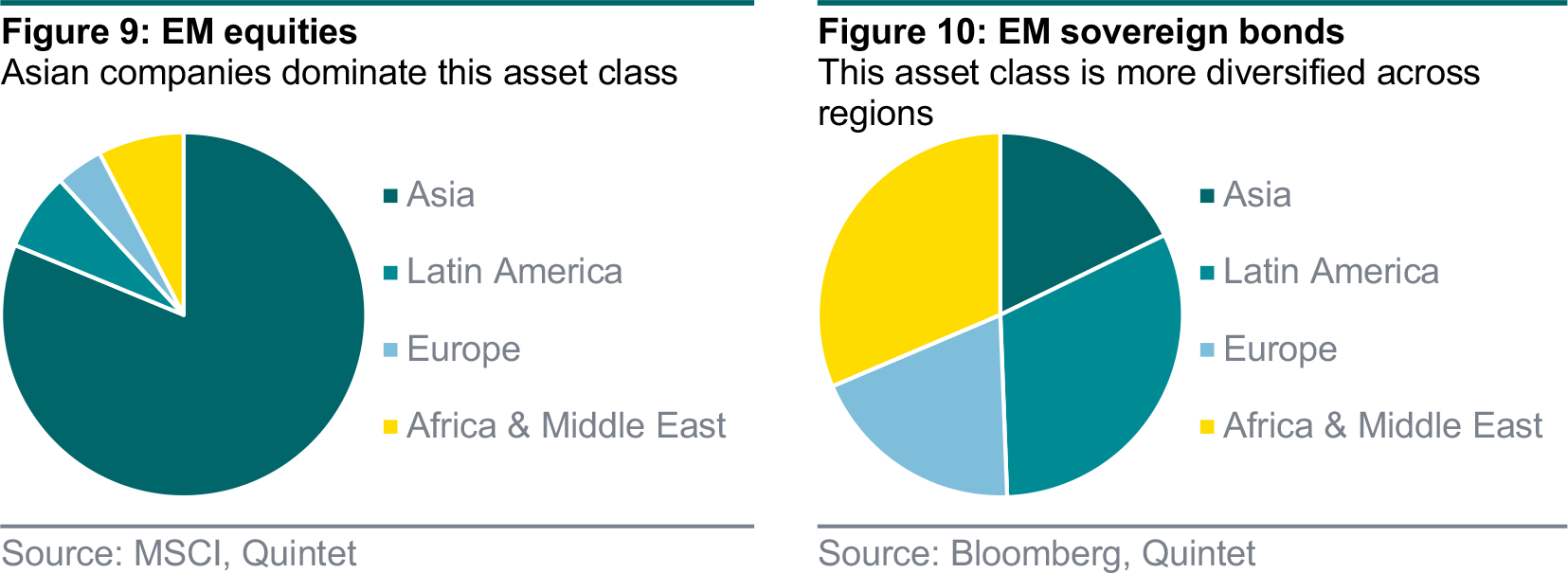

Our current tactical asset allocation is overweight several emerging market asset classes, namely EM equities, EM sovereign and Asian high yield bonds. As seen above, emerging markets actually are a very heterogeneous group of different regions and countries. It’s thus crucial to consider the underlying regional composition when assessing the risks and return potential of EM asset classes.

EM sovereign bonds are more diversified across the different regions. Unlike equities, Latin America, Africa and the Middle East deserve more attention when analysing this asset class. Currency risk is not a direct concern, as this is USD-denominated debt. The more vulnerable state of many Latin American economies is reflected in valuations, as the region’s credit spread currently is 130 bps above the Asian one.

As these simple examples show, the EM macro scoring can inform our asset allocation process regarding underlying regional dynamics and risks. At the same time, it’s important to stress that this is just one perspective among the many we take into consideration.

There are now almost 113 million confirmed cases of Covid-19 globally. Yet the rate of daily new infections appears to have stagnated at around 45 per million, which is a significant fall from 94 per million at the start of 2021. This fall is taking place in the US, UK and euro area, and is mainly due to the lockdowns that are in place. Throughout the euro area, restaurants and many recreational activities are restricted, and in some countries a night-time curfew has also been enforced.

In the US, masks are still not compulsory in all states and most stores are also open. Nevertheless, overall the country seems to have the pandemic more under control, supported by the rapid progress of its vaccination programme. More than 13% of Americans have received at least their first dose, while the corresponding number in the UK is 26%.

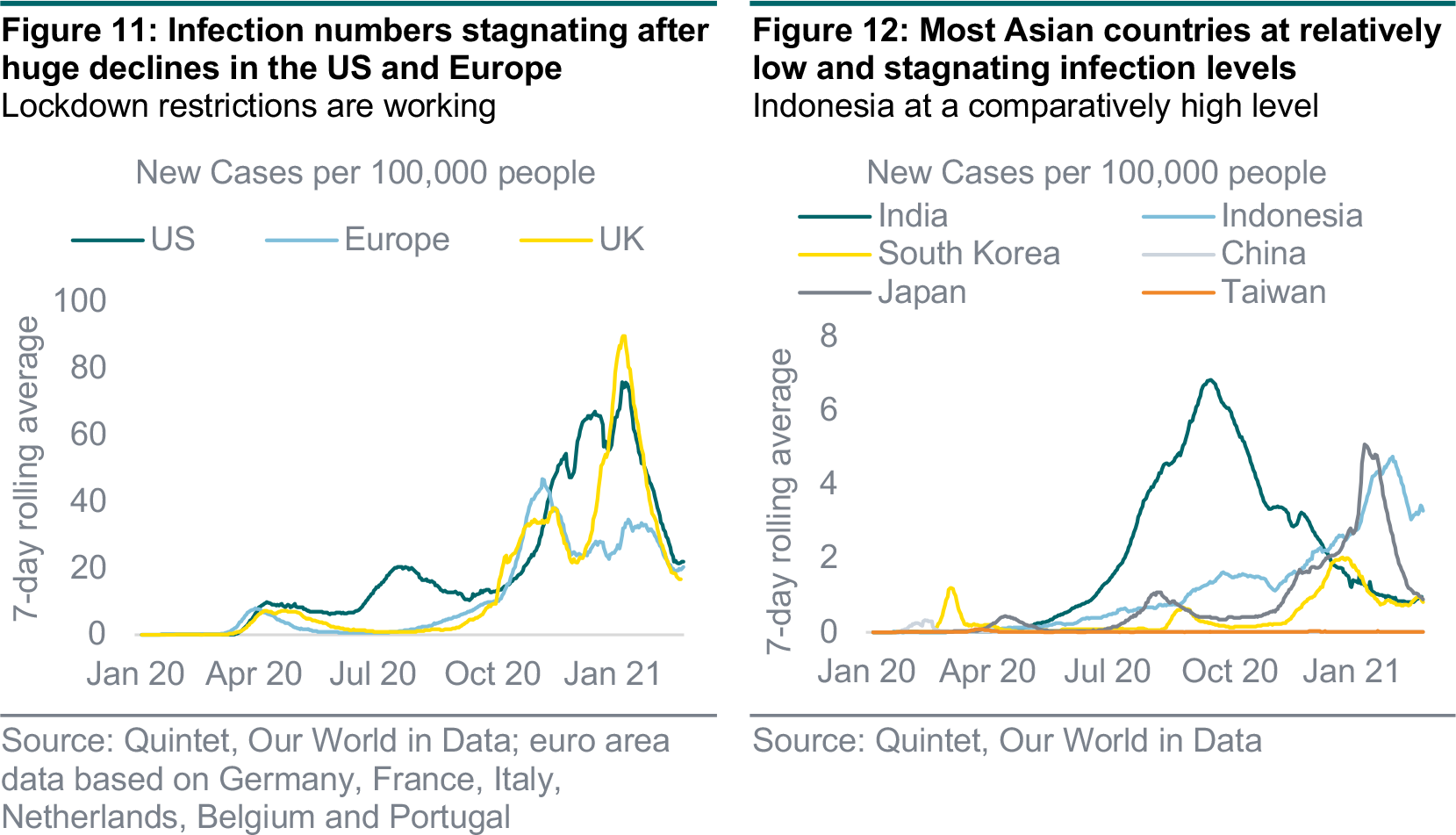

New daily infection rates in both the US and Europe have slowed to around 20 per 100,000 inhabitants (figure 11). Both regions have reached this level after sharp falls since the start of the year and are roughly at the same stage as six months ago.

Asia’s infection pattern looks different. The number of confirmed new infections is much lower in relation to the number of inhabitants (figure 12). Moreover, levels and trends are very different within the region. India had its peak in the middle of last summer/early autumn and confirmed new infections have been dropping since then with a flattening curve. Meanwhile, the country’s cases per 100,000 inhabitants are at a similar level to those of South Korea and Japan. However, these two countries have not had nearly as extreme an increase. Japan was hit harder than other Asian countries at the beginning of the year, but quickly took strict measures to reduce its numbers.

Indonesia’s infections were still surging until a month ago, although the country has managed to curb the pandemic recently. Nevertheless, the numbers in relation to the population are still far above other Asian countries. Today, China and Taiwan seem to be almost unaffected by the pandemic. However, reported infection figures should always be viewed with caution, as developing countries in particular tend not to have strong testing capacity. While most Asian countries have ordered enough vaccine doses to reach herd immunity, their vaccination processes are lagging.

Singapore is progressing fastest with around four people per 100 inoculated. Japan only started vaccinating on 17 February and South Korea on 26 February, making it the last OECD country.

Several factors explain why the virus is spreading at a slower rate even though mutations have appeared across Europe and parts of the US, including Florida. One is the progress of vaccinations. Since last month, the number of vaccinated people worldwide has increased considerably. With ongoing deliveries from Pfizer/BioNTech, AstraZeneca and Moderna in Europe and the US, vaccination rates should continue to rise.

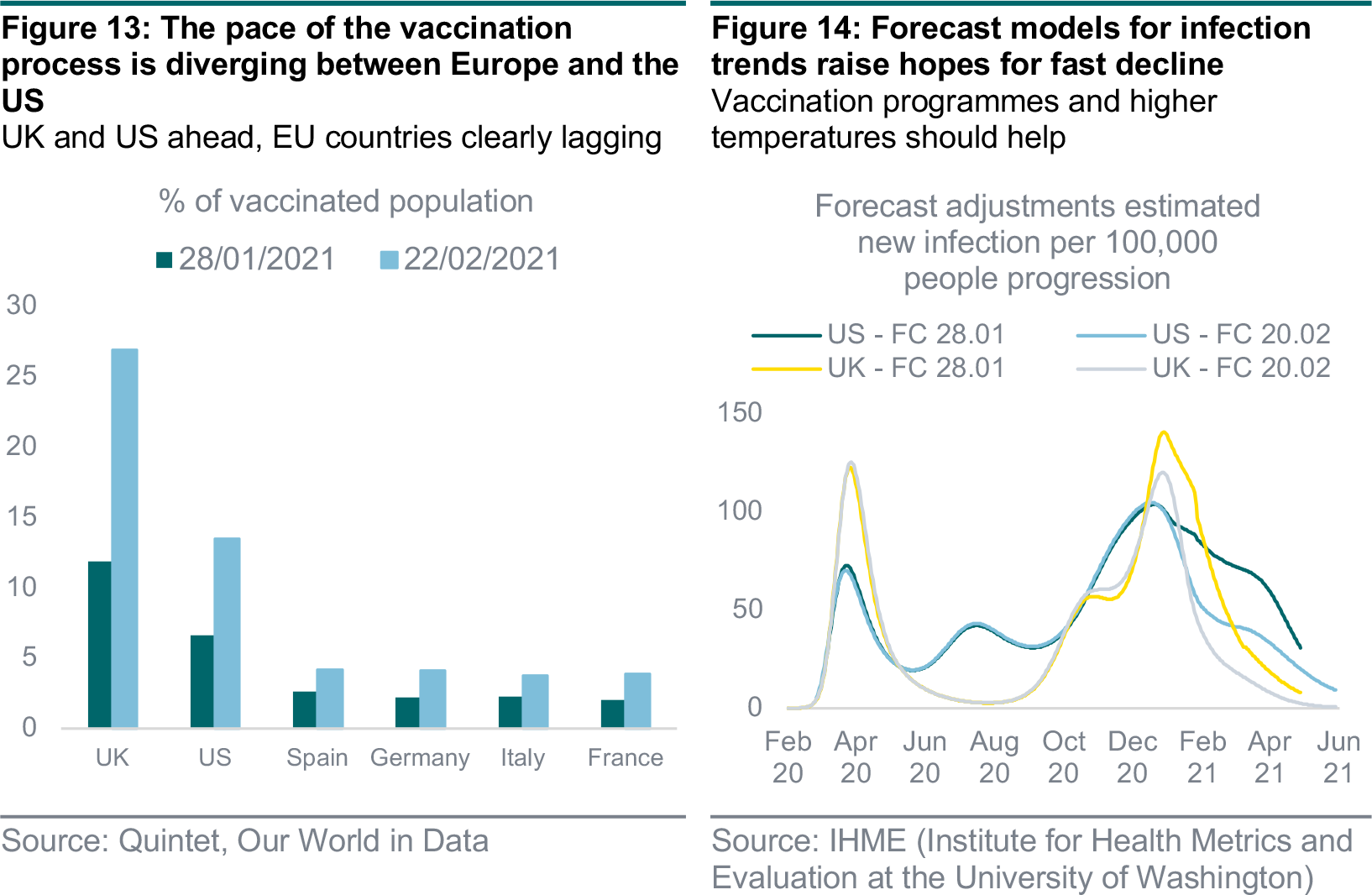

Euro area countries are ramping up their vaccination programmes, although the pace of the rollout is slower (figure 13). One of the reasons is scepticism about their efficacy, such as AstraZeneca’s vaccine in Germany. The rate of new infections will determine when countries are able to relax their lockdown measures, and therefore the timing and pace of the economic recovery process.

Forecast models for upcoming new infection trends reflect the influence of vaccinations and higher seasonal temperatures. For example, Washington University’s Institute for Health Metrics and Evaluation (IHME) has adjusted its forecasts (figure 14). As the vaccination rate increases, the number of new infections decreases and herd immunity should be achieved more quickly.

Although there is still uncertainty about the efficacy of some vaccines, studies confirm they are slowing the spread of Covid-19. This positive development in forecasts could take some time to materialise in Europe. The delays in vaccine deliveries and in some case a slight reluctance among the population are still playing a major role in this development.

Forecasts suggested the UK would suffer a large increase in infections during the first quarter of 2021 owing to mutations. However, the widespread vaccination programme seems to have prevented this increase. The UK is now forecast to have very low infection rates by the middle of 2021 – even lower than the US. This positive development should lead to the easing of lockdown measures as outlined by Prime Minister Boris Johnson, who indicated that all restrictions could be removed from 21 June. In addition, higher summer temperatures should – like last year – push infection numbers down further. Heading into autumn, it will be important that vaccination programmes are advanced enough to avoid another difficult winter.

Authors:

Daniele Antonucci Chief Economist & Macro Strategist

Bernhard Eschweiler Consultant

Carolina Moura-Alves Group Head of Asset Allocation

Philipp Schöttler Cross-Asset Strategist, Group Chief Investment Office

Bill Street Group Chief Investment Officer

This document has been prepared by Quintet Private Bank (Europe) S.A. The statements and views expressed in this document – based upon information from sources believed to be reliable – are those of Quintet Private Bank (Europe) S.A. as of 1 March 2021, and are subject to change. This document is of a general nature and does not constitute legal, accounting, tax or investment advice. All investors should keep in mind that past performance is no indication of future performance, and that the value of investments may go up or down. Changes in exchange rates may also cause the value of underlying investments to go up or down.

Copyright © Quintet Private Bank (Europe) S.A. 2021. All rights reserved.