Is the sky the limit for equities?

Equity indices from the US to Japan and through Europe continue to make record highs week after week. Last week was no different, although some indices closed flat such as the US S&P 500. There’s a structural element to this rally, which we carry in our portfolios. It’s the AI revolution that has sent related shares (AI, semiconductors, and “big tech” alike) through the roof. For example, did you know that the combined value of the so-called “Magnificent 7” (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla) is as large as the economies of Germany, Japan, and India combined? But it’s not just AI hype; economic drivers such as improving growth prospects and expectations of interest rate cuts are also boosting equities. That said, we believe a global economic slowdown is still likely, so there could be temporary setbacks for equities along the way. Therefore, we think the risk/reward for equities is reasonably balanced over the next 12 months, which is why our equity holdings are neutral relative to our long-term allocation.

Bonds on the backfoot

Government bond yields rose last week (meaning prices fell) following the rise in US inflation, but we don’t think this will be a long-lived trend as it was in 2023. Despite the slight uptick, inflation has been trending downwards and central banks will likely cut interest rates in 2024. As such, the peak in bond yields is probably behind us. While the US Federal Reserve will be in no hurry to cut rates at its meeting this Wednesday, it will still likely lean towards rate cuts around the middle of the year.

A big change for Japan

In 2016, Japan set negative interest rates and hasn’t budged ever since. But now there’s been growing speculation that the Bank of Japan (BoJ) will change its stance following strong wage negotiations and Japan’s stock market reaching a record high. The first step for the BoJ would be raising the policy balance rate from -0.1% to 0%, which could happen at its March 19 or April 26 meetings. We think the BoJ is unlikely to go much higher than 0% at this stage, which is reflected in Japanese bond prices and the yen exchange rate. Any major surprise could, therefore, move markets.

Surprise rate cuts in Europe?

We could see the first Western central bank rate cut this week as markets are not excluding a surprise rate cut from the Swiss National Bank (SNB) on Thursday. This comes after SNB President Thomas Jordan declared that they have reached monetary policy stability. This supports our view that the Swiss franc will likely depreciate against the euro over the course of 2024. We also expect the Bank of England on hold this week, but to hint that rate cuts are not that far.

Is spring coming to Europe?

While the Eurozone economy has been alternating between stagnation and slight contraction since mid-2023, it looks as if activity is no longer deteriorating. This week’s purchasing managers’ indices, while still weak, are expected to show a continuation of this gradually improving situation. If this improvement continues over the coming months, we will reduce our recession probability forecast and, potentially, consider adjusting our cautious Eurozone positioning, for example in equities. But this still looks premature for now, as recession risks still linger and seem underappreciated to us. So, for now, we hold low-volatility equities in Europe to protect against a sluggish growth environment, along with a reduced exposure to Eurozone equities.

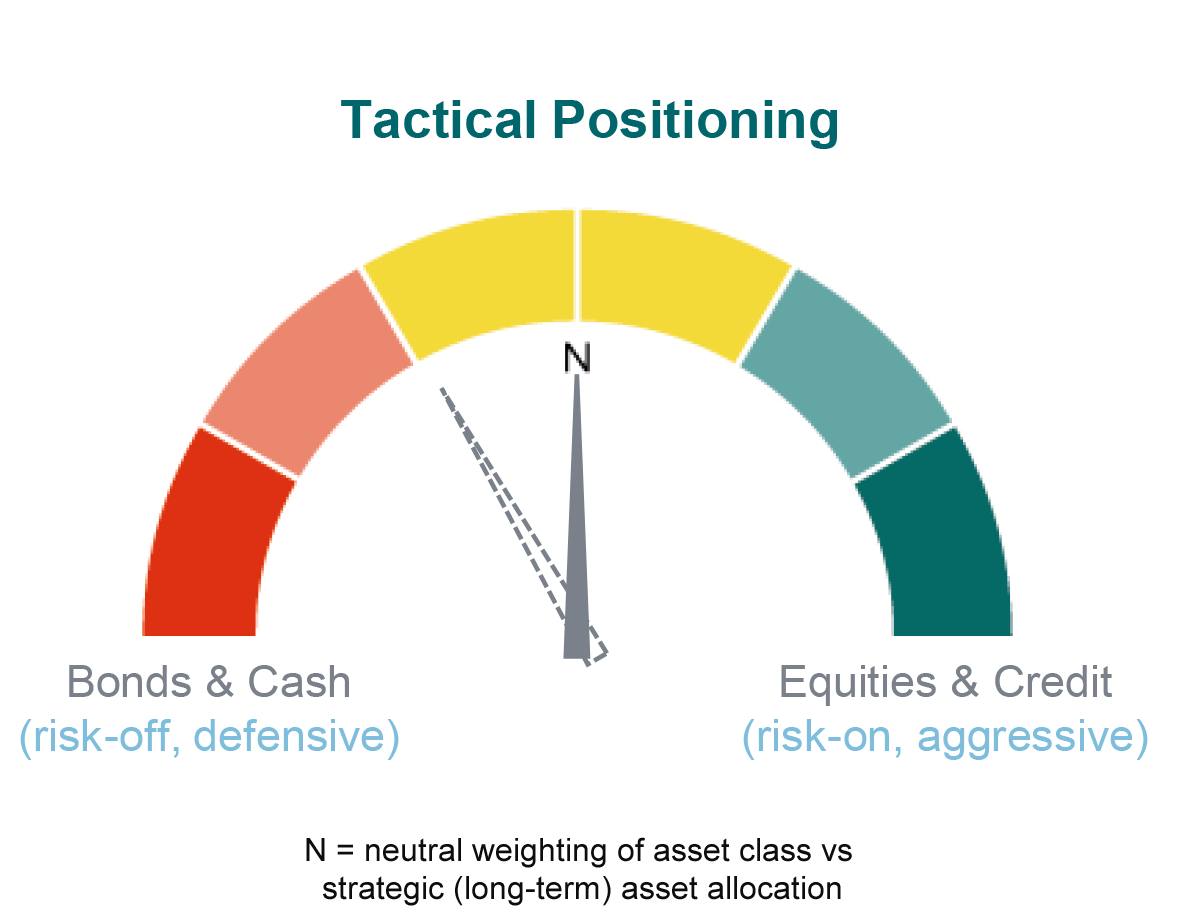

Staying balanced

For about a year and a half, we’ve held fewer equities and more bonds in portfolios compared to our long-term strategy. In February, given better US economic prospects and interest rate cuts from mid-year, we brought both back to neutral. As such, we increased our equity holdings and reduced bonds.

For a detailed overview of our allocation in flagship portfolios, please visit our latest Counterpoint.

Data as of 15/03/2024.