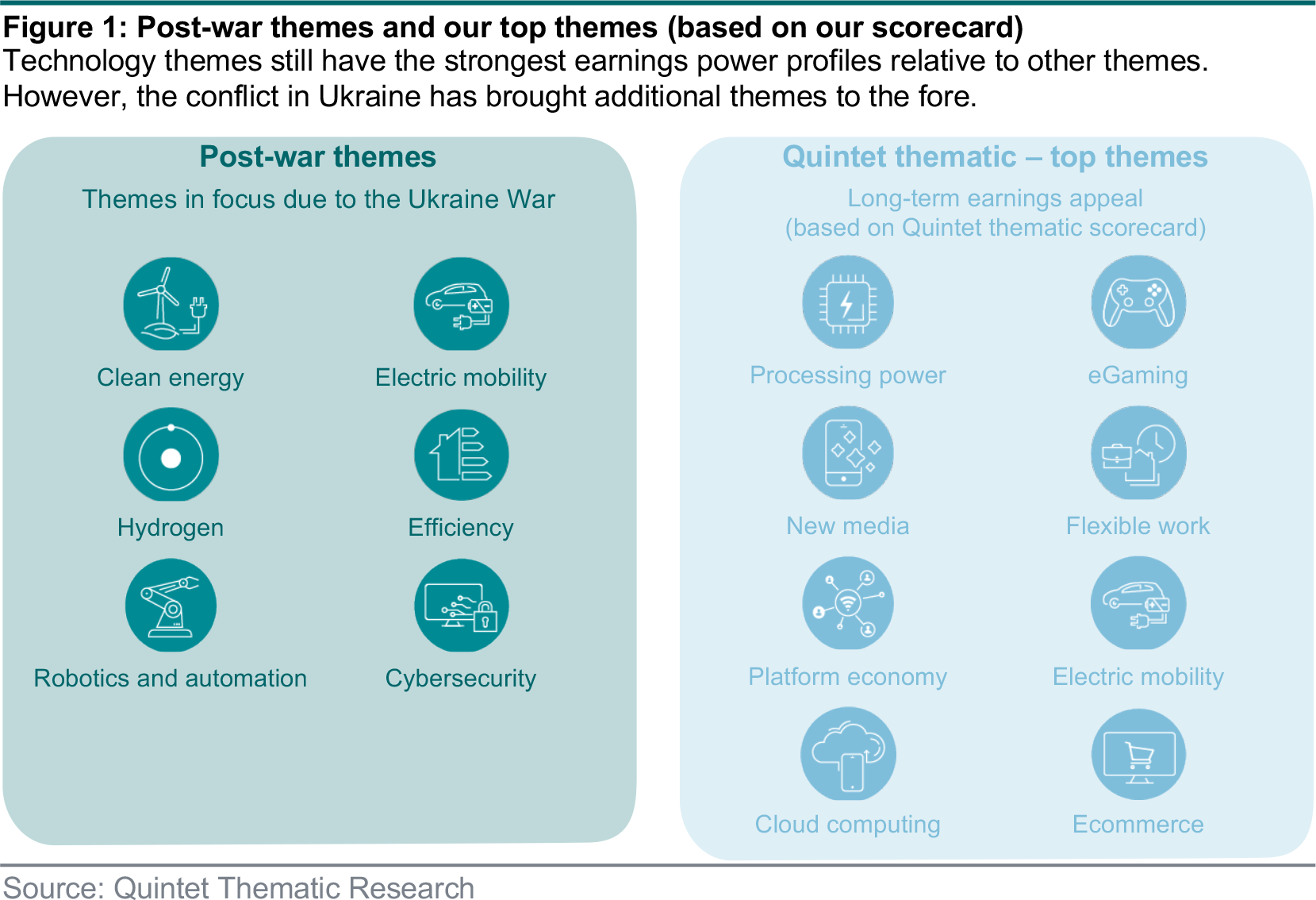

Ukraine War: themes to de-risk economies

We believe the war in Ukraine – which is first and foremost a humanitarian tragedy – will spur some countries and businesses to reduce long-term risks that have emerged from that conflict. Structural investment themes likely to witness growth associated with such de-risking include those linked to sustainable energy (such as clean energy and electric vehicles), localised supply chains (robotics and automation) and online safety (cybersecurity

- The war in Ukraine has exposed structural weaknesses in the tightly interconnected global economic system – not just in energy supply but also in areas like supply chains and material sourcing. Risks have also increased around cybersecurity and hacking of key systems.

- Crises can cause human tragedy and disruption but also spur innovation. COVID-19 led to huge advances in genomics, digital health, e-commerce and flexible working technologies. Similarly, the conflict in Ukraine could boost technologies key to addressing major issues like climate change, supply chain risks and ageing populations.

- Despite near-term price surges in energy and strategic metals, this crisis will likely lead to a major reassessment of systemic risks and shifts to alternatives in the long term. Themes linked to sustainable energy, local supply chains and digital safety will be key as priorities realign.

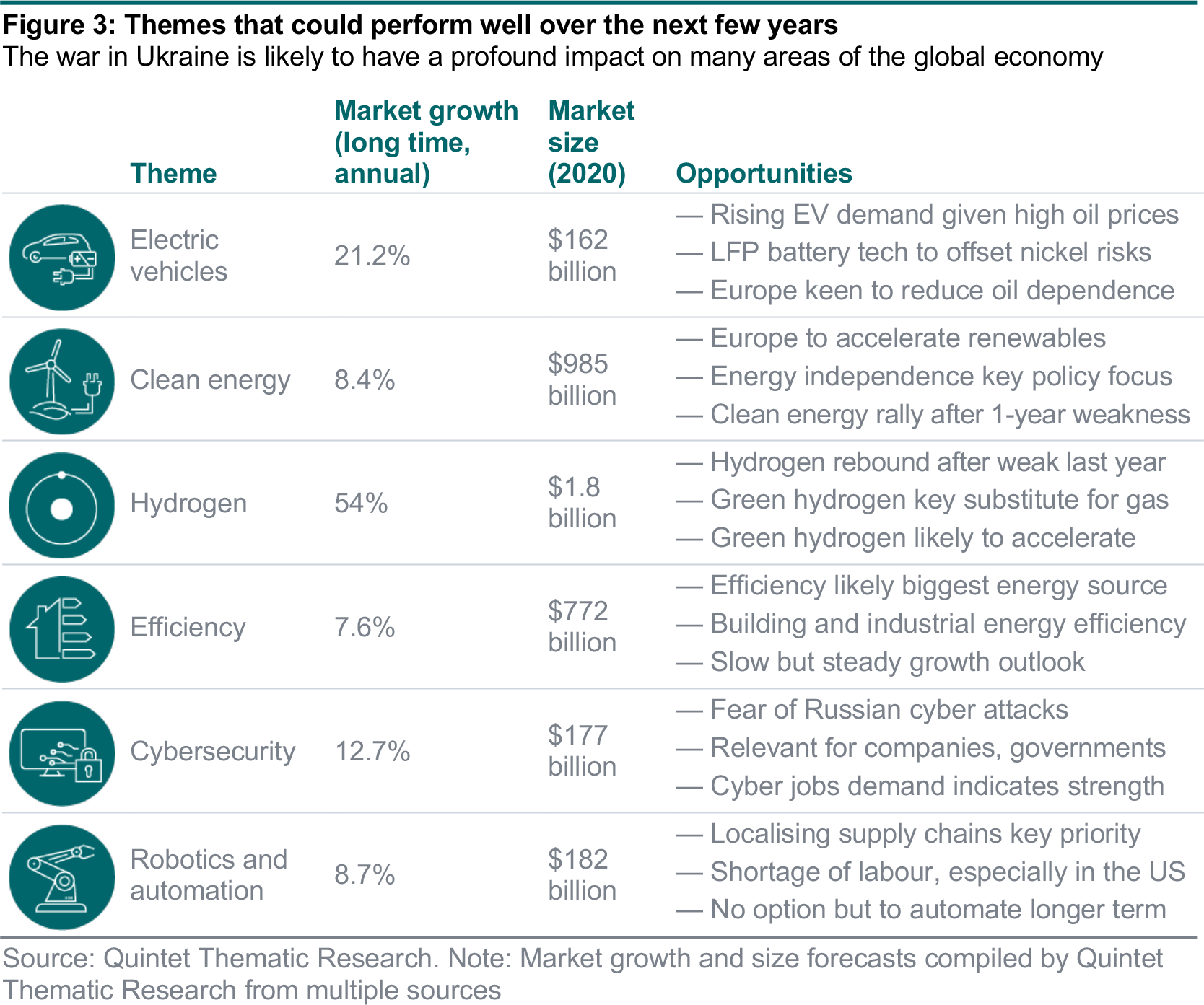

Sustainable energy themes are likely to be a main focus in the post-war era. The conflict in Ukraine has further exposed dependence on fossil fuels prone to supply shocks and huge spikes in energy costs (and inflation). The global nature of energy markets means that supply disruption in one region affects everyone via pricing. As a result, countries worldwide will look to accelerate the process of reducing energy risks. We believe sustainable energy themes that could directly emerge from the Ukraine crisis and having strong long-term support are clean energy and electric vehicles. Other sustainability themes like hydrogen, efficiency, recycling and future food should grow too.

De-risking supply chains is becoming crucial given multiple shocks in recent years, from the US-China trade war, COVID-19 and climate risks, to the conflict in Ukraine. Countries and companies are likely to rebalance supply chains towards greater local production, thereby boosting robotics and automation. Investment in cybersecurity will likely be boosted as digital systems need to be secured.

It is important for investors to recognise that these shifts will not happen overnight, irrespective of any near-term volatility. We believe investing in themes that are well placed in the long term, as well as a diverse set of innovation themes is the right approach.

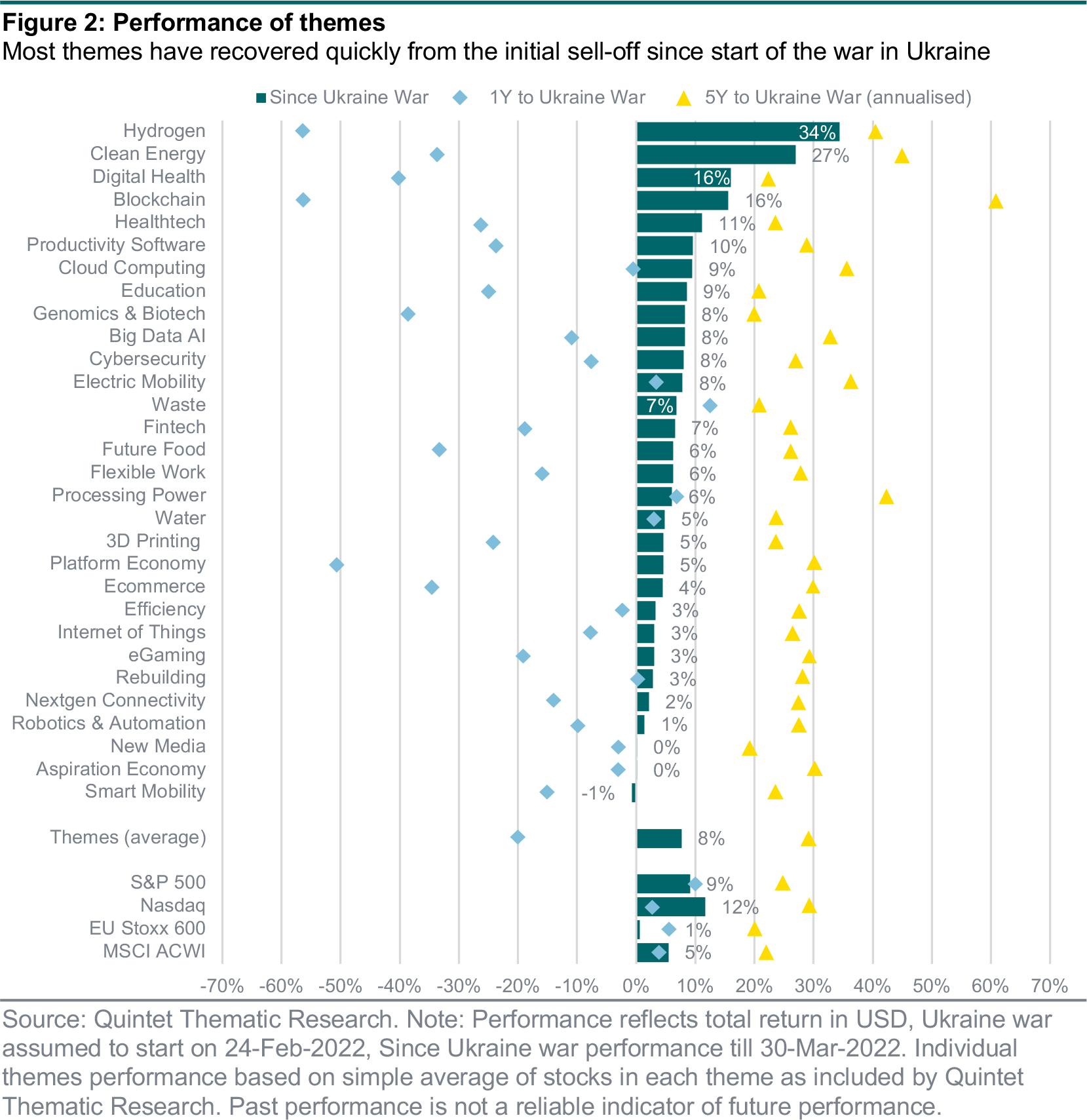

Five-year returns until the Ukraine crisis. Among the 30 themes we track, most performed well up to mid-2021 (when the growth to value rotation started) with strong annualised five-year returns (20-40% pa) until Russia’s invasion.

One-year returns until the Ukraine crisis. Most themes underperformed since mid-2021 till the start of the war in Ukraine, amid the post-COVID-19 reversal and the growth to value rotation driven by rising bond yields. During this rotation, only some themes held up – waste, water, rebuilding, efficiency, cloud computing, processing power and electric mobility – these themes either had some defensive qualities or underlying strength in demand.

Since the invasion of Ukraine. Following Russia’s invasion, hydrogen and clean energy themes have performed strongly, although they underperformed the year before. Overall, many themes have started to perform well as broader markets recover from the initial shock, while clarity from the Fed on rate hikes has also helped growth stocks in general. We believe themes that could be in focus during the next few years but have lagged in the market recovery include electric mobility, efficiency and robotics and automation, providing investment opportunities for the long term.

Sustainable energy. Sustainable energy themes that could grow faster in the next few years and benefit from strong market support are clean energy and electric mobility. Other sustainability themes like hydrogen and efficiency ought to emerge too but their paths are more winding. Vertical farming (future food) and recycling (sustainable resources and waste) can be long-term solutions.

Local supply chains. Most industries will likely try to rebalance their supply chains towards greater local production, thereby boosting robotics and automation.

Data security. Spending on cybersecurity will likely be boosted as digital systems need to be secured further.

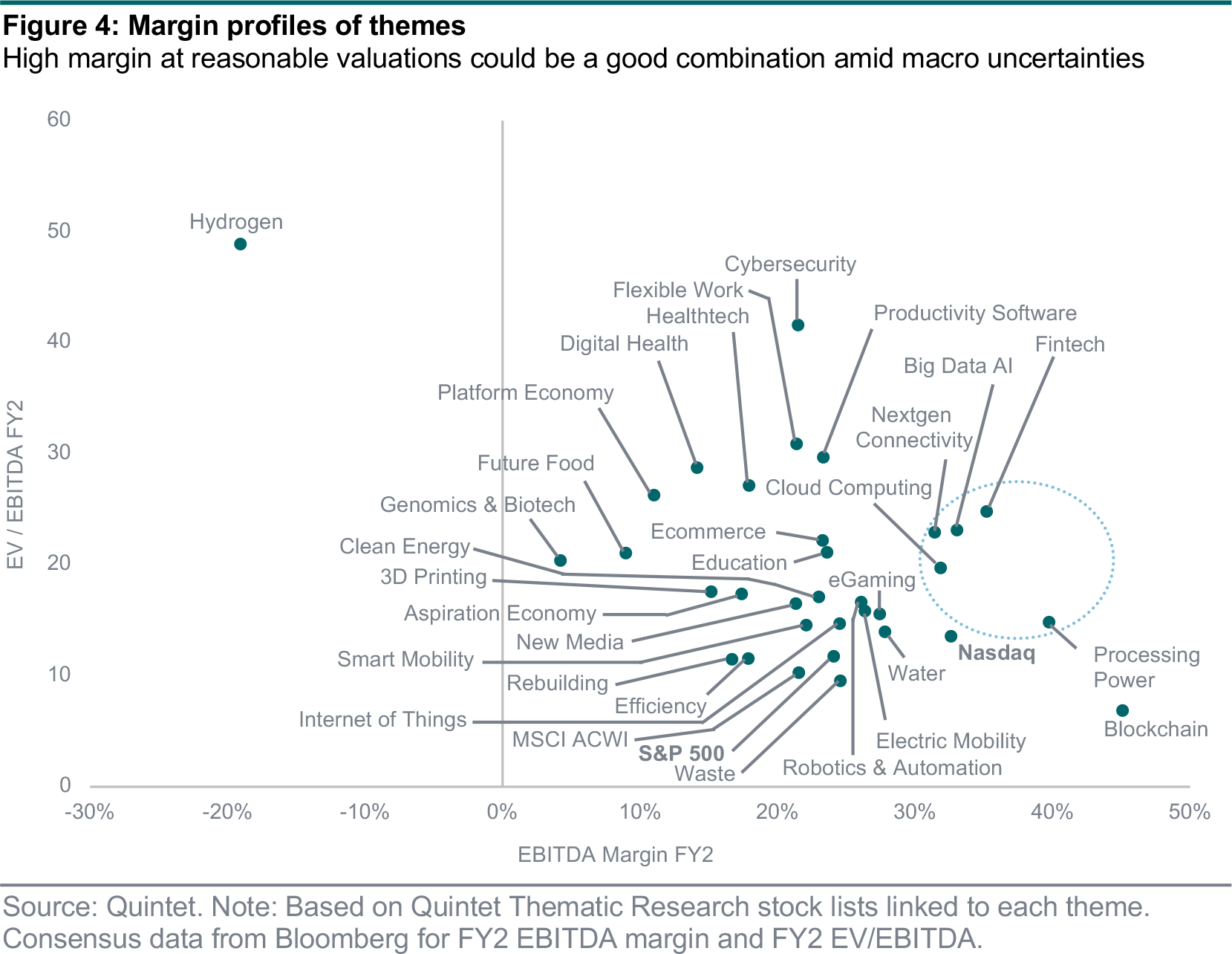

Margins. As input costs rise, whether via material and energy costs or wage inflation, it is worth considering the margin profile of themes. We have assessed EBITDA margins as a simple proxy for cash generation. The higher the margin of companies within a theme, the less exposed the theme will be to rising costs. Of course, margins are not the only driver as sales growth and pricing power are important drivers too. And consensus forecasts could change as the year progresses anyway. But all else equal, higher margins are preferable to lower margins, in our opinion.

Valuation. Long term investing during times of trend growth may not require too much focus on valuation. But during times of heightened uncertainty around costs, growth, supply shocks and interest rates, valuation can become an important consideration as we have seen in 2021. Most companies across the world, whether thematic or not, will likely face cost pressures in 2022 and not all have the pricing power or sales growth to cushion these pressures. Thus, it makes sense to be overweight themes which have the combination of high margins, robust growth and reasonable valuations. This can help cushion the impact of multiple and earnings compression.

Well-placed themes linked to the war in Ukraine. Following Russia’s invasion, we believe electric mobility, robotics and automation, and clean energy offer appealing margin-valuation profiles as well as attractive structural stories over the long term. Hydrogen is not profitable yet while efficiency has lower margins. Cybersecurity should benefit from additional spending but trades at higher multiples, even against other technology themes.

Structurally strong themes. Among more persistent themes that are not directly linked to the conflict, we believe processing power, nextgen connectivity, cloud computing and big data AI have the best margin-valuation combination. Fintech screens well but also has seen more competitive pressures recently and some slowdown post COVID-19, we believe.

Structural themes play out over multiple years, sometimes even longer than a decade. To identify strong themes for the long term, it is important to consider the following characteristics:

- Companies with high margins (e.g. software, ecosystem and network effects). They have less exposure to raw material or energy cost pressures. These companies will likely have more exposure to employee costs but concepts like flexible working can help them adjust more easily.

- Companies in high-growth markets. Due to underlying demand, companies in high-growth areas are better able to grow sales and even increase prices. For example, Tesla, Netflix, Apple and Amazon have been able to increase prices many times without any material impact on demand so far. Processing power linked companies are likely to benefit from supply shortages in the near term with data volume and device growth the major long-term supports.

Generally, but more so in 2022, we think it is prudent to focus on S-curve themes over moonshot themes.

- S-curve themes are those where the technologies are known or close to being commercially successful (e.g. cloud computing and electric vehicles) but we are still in the early stages of penetration and market growth.

- Moonshot themes, on the other hand, could be very impactful and profitable if successful but commercial success is not yet proven or certain (e.g. quantum computing and space tech).

Typically, S-curve themes have better earnings visibility than moonshot themes. This is a useful characteristic to have in the near term as the market tries to digest many different uncertainties such as inflation, interest rates, growth rates, labour shortages and geopolitical risks. In addition, investors can always await further maturation of moonshot themes because the period of success could last a decade or even more.

Our proprietary Quintet Thematic Scorecard allows us to quantitatively assess companies across all themes and rank them on a relative basis. In simple terms, themes with a score closer to 10 have stronger sales growth and gross margin profiles than those with scores closer to zero. We consider both reported history and forward-looking consensus estimates. We also consider valuation, expectations and performance but overall, long-term earnings profile is the main criteria. We believe that in the long term, earnings power is most likely to determine which companies and therefore which themes are likely to perform well over extended periods despite short-term volatility. Please refer our Quintet Thematic Framework Launch (Nov-2021) for further insights into our approach and methodology.

Generally, we do not expect major changes in our scorecard in any given quarter, even if changes can happen over two- to three-year timeframes. Despite full-year results in the last quarter and also some shifts like post-COVID slowdown in some digital technologies, we did not see major changes among the top quartile of themes compared to our first scorecard published in November 2021.

- Improvers among top quartile. Cloud computing (from #9 to #7) improved two places. processing power, egaming, electric mobility and platform economy improved one rank.

- Decliners among top quartile. New media (from #1 to now #3) and ecommerce (from #5 to #8) saw downward revisions, likely reflecting post COVID-19 softness, in our opinion.

Among the lower-ranked themes, there can be more shifts due to weaker earnings power, whether due to more volatile sales growth and weaker gross profit profiles. Even within the lower-ranked themes there can be companies with strong profiles. Sometimes short-term performance can be strong even for poorly scoring themes due to other factors (e.g. hydrogen has rebounded since the Ukraine war despite weak margin profiles).

Authors:

- Pinaki Das Head of Thematic Research

- Daniele Antonucci Chief Economist & Macro Strategist

- Kenneth Warnock Head of Direct Equities

- Bill Street Group Chief Investment Officer

This document has been prepared by Quintet Private Bank (Europe) S.A. The statements and views expressed in this document – based upon information from sources believed to be reliable – are those of Quintet Private Bank (Europe) S.A. as of 4 April 2022, and are subject to change. This document is of a general nature and does not constitute legal, accounting, tax or investment advice. All investors should keep in mind that past performance is no indication of future performance, and that the value of investments may go up or down. Changes in exchange rates may also cause the value of underlying investments to go up or down.

Copyright © Quintet Private Bank (Europe) S.A. 2022. All rights reserved.