To exclude or engage

There are several ways to align portfolios with sustainable considerations. Sometimes deciding not to invest is the optimal choice. However, investing can often provide an opportunity to encourage positive change.

- Exclusion and engagement can be combined when investing sustainably. We can remove exposure to the most damaging activities from portfolios, while still seeking engagement opportunities with companies to improve financial outcomes and benefit people and the planet.

- Exercising the influence we have as an investor through engagement is consistent with both our fiduciary duty and our objective to be a sustainable company.

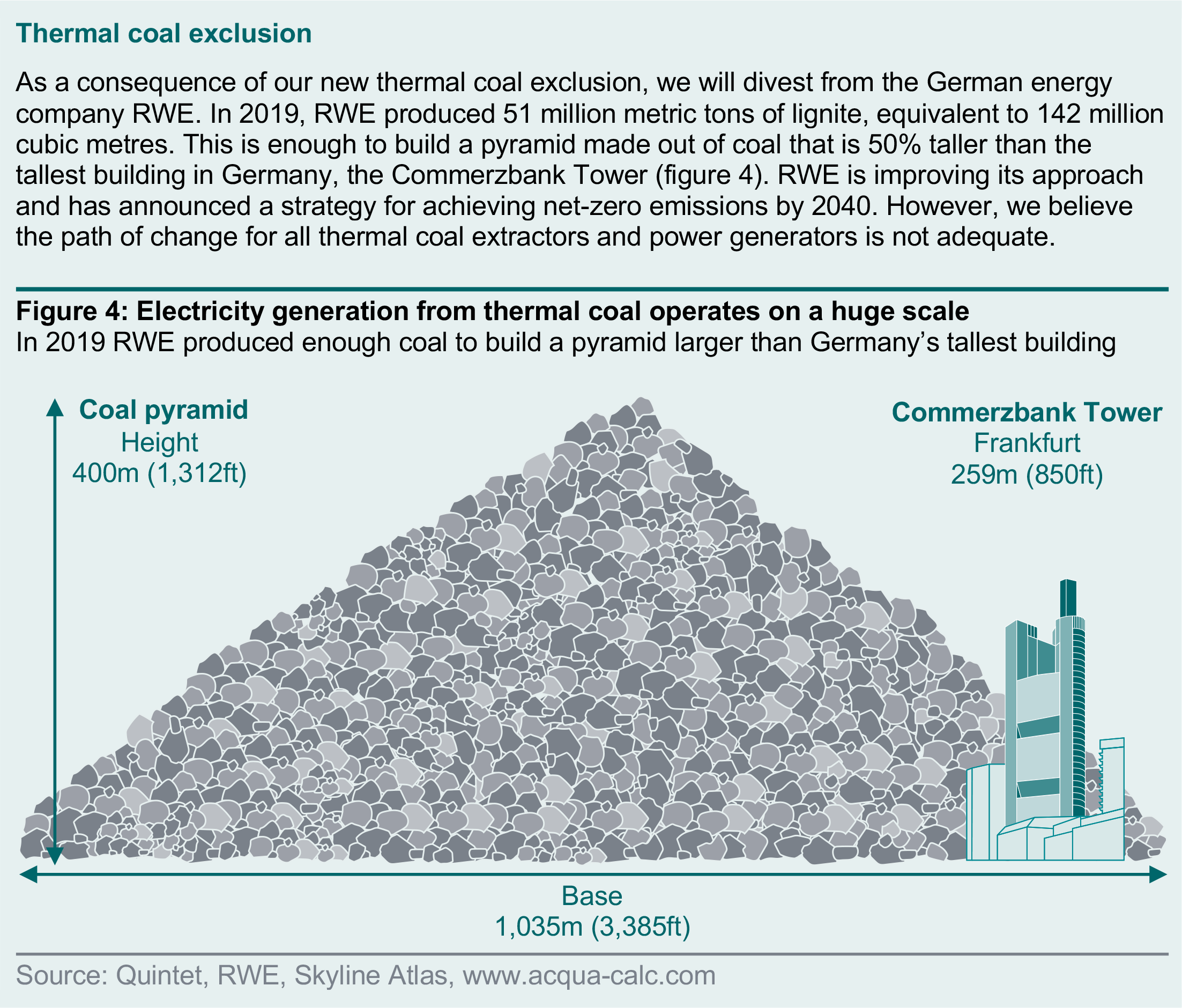

- From 2022 we will not invest in companies deriving more than 10% of revenue from thermal coal extraction or power generation. We view the “technology” as obsolete, financially unviable over the medium term, and highly detrimental to the environment.

Sustainable investors have a wealth of tools they can deploy to further achieve their financial and sustainable objectives. Two popular methods are exclusion and engagement (figure 1).

- Exclusions remove companies, sectors or economic activities from an investment universe or portfolio based on an investor’s preferences, moral or social values and / or risk tolerance.

- Engagement uses the influence obtained by purchasing securities to enhance the conduct of companies by encouraging more sustainable business models.

At first glance, when confronted with unsavoury practices, these methods appear opposed. Exclusion involves selling or not investing in securities, while engagement involves investing to exert influence.

We combine these methods by excluding companies involved in the most damaging activities, while still seeking engagement opportunities with others to improve financial outcomes and benefit people and the planet. In our report Strategy primer: sustainable improvers we evidence the favourable financial benefits that come from improving sustainability practices.

Exclusion was the “original” sustainable investing method, dating back to the 17th century when religious groups – such as the Quakers and Methodists – avoided companies that were not in line with their values. The first ethical mutual fund was launched in 1971 at the height of the Vietnam War and excluded companies involved in the production of nuclear and military weapons. Today, exclusion remains the most widely used method when integrating ethical preferences.

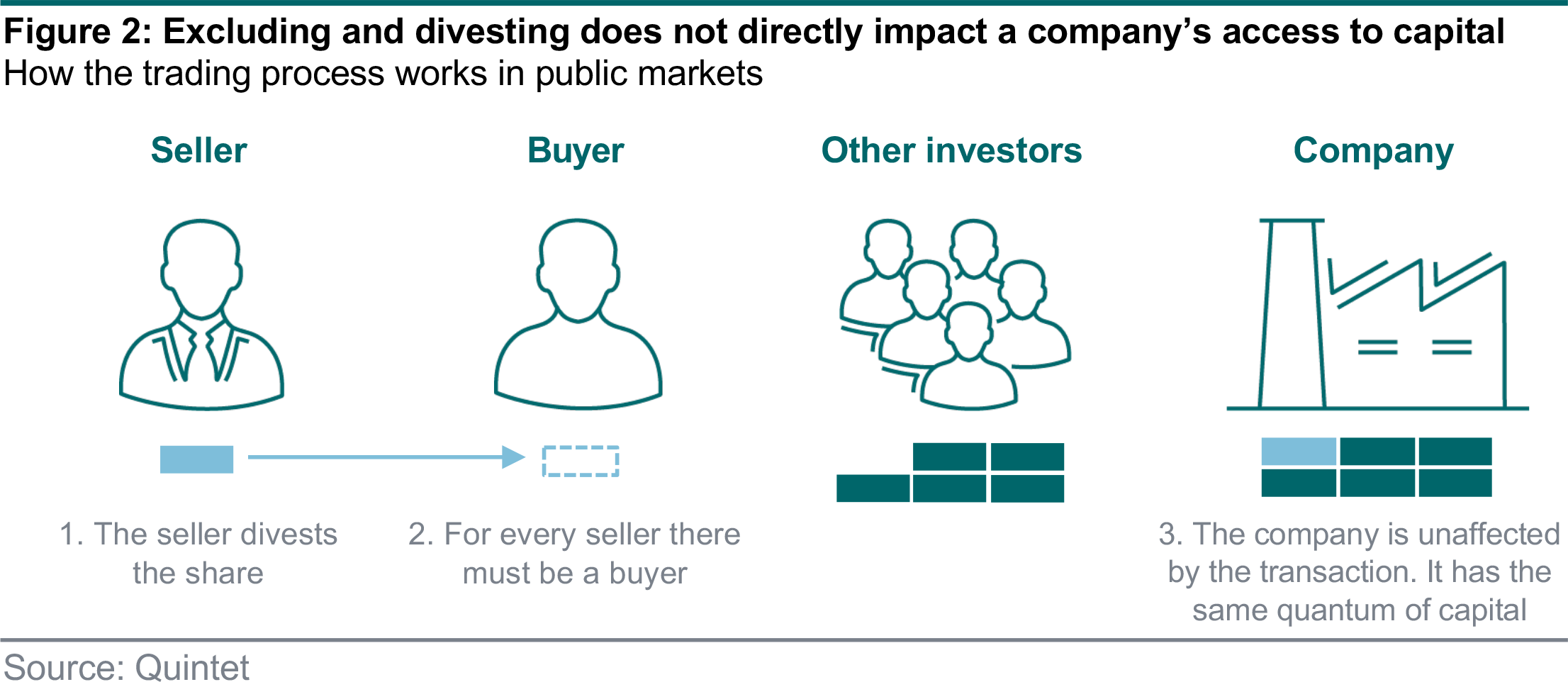

Proponents of exclusionary methods argue that by not investing – or by selling – an investor pushes the value of a security down, therefore restricting access to capital and making it incrementally harder for entities that harm people or the planet to operate. However, evidence to support this theory is limited. When excluding – or selling stocks – in liquid markets, by definition, a seller is matched with a buyer. Therefore, the impact on the price of a security is limited (figure 2).

Research of major exclusions find that divestments merely “reallocate shares and operations from ‘‘socially responsible’’ to more indifferent investors”. Further evidence of exclusion’s limited impact on people and the planet comes from a non-sustainable source – divestment following a company’s ejection from a major index such as the S&P 500. With over USD 13 trillion of assets benchmarked to the S&P 500, an ejection triggers a divestment multiple times larger than any sustainable- investing derived exclusion.

Evidence shows that even with this selling pressure, an abnormal decrease in the value of a security lasts just 20 days before being reversed – hardly time to impact an entity’s access to capital. Academic research concludes to raise the cost of capital for an entity and induce change, in excess of 25% investors must choose to divest – which is well above what is observed in the market.

The value of exclusion is rarely about directly helping people and the planet. It is instead primarily to align investments to values and protect a portfolio from activities so damaging that they may create intolerable levels of financial risk.

Academic evidence suggests a small number of exclusions will have no material bearing on the ability to construct a diversified portfolio. As few as 20 randomly chosen stocks will exhibit the same level of volatility as a market-wide portfolio and a little over 100 stocks will produce equivalent results on the more complex measures of risk, such as expected shortfall. From a statistical point of view, excluding a small percentage of entities from a large universe will not harm a portfolio’s risk-adjusted returns.

We regard exclusion as a last resort, when active ownership has proven unsuccessful or is not possible, and further investment would be incompatible with our principles or would create intolerable levels of financial risk. Because we follow a principles-based approach to sustainable investing, we use only a limited number of exclusions.

We exclude companies involved in controversial weapons, subject to European Union arms embargoes, and those that are non-compliant with the United Nations Global Compact and unlikely to respond to constructive engagement.

From 2022 we will start excluding companies deriving more than 10% of revenue from thermal coal extraction or power generation. We view the “technology” as obsolete, financially unviable over the medium term and highly detrimental to the environment.

The International Energy Agency (IEA) found that CO2 emitted from coal combustion is responsible for over 0.3°C of the 1°C increase in global average annual surface temperatures above pre- industrial levels. This makes coal the single largest source of global temperature increase.

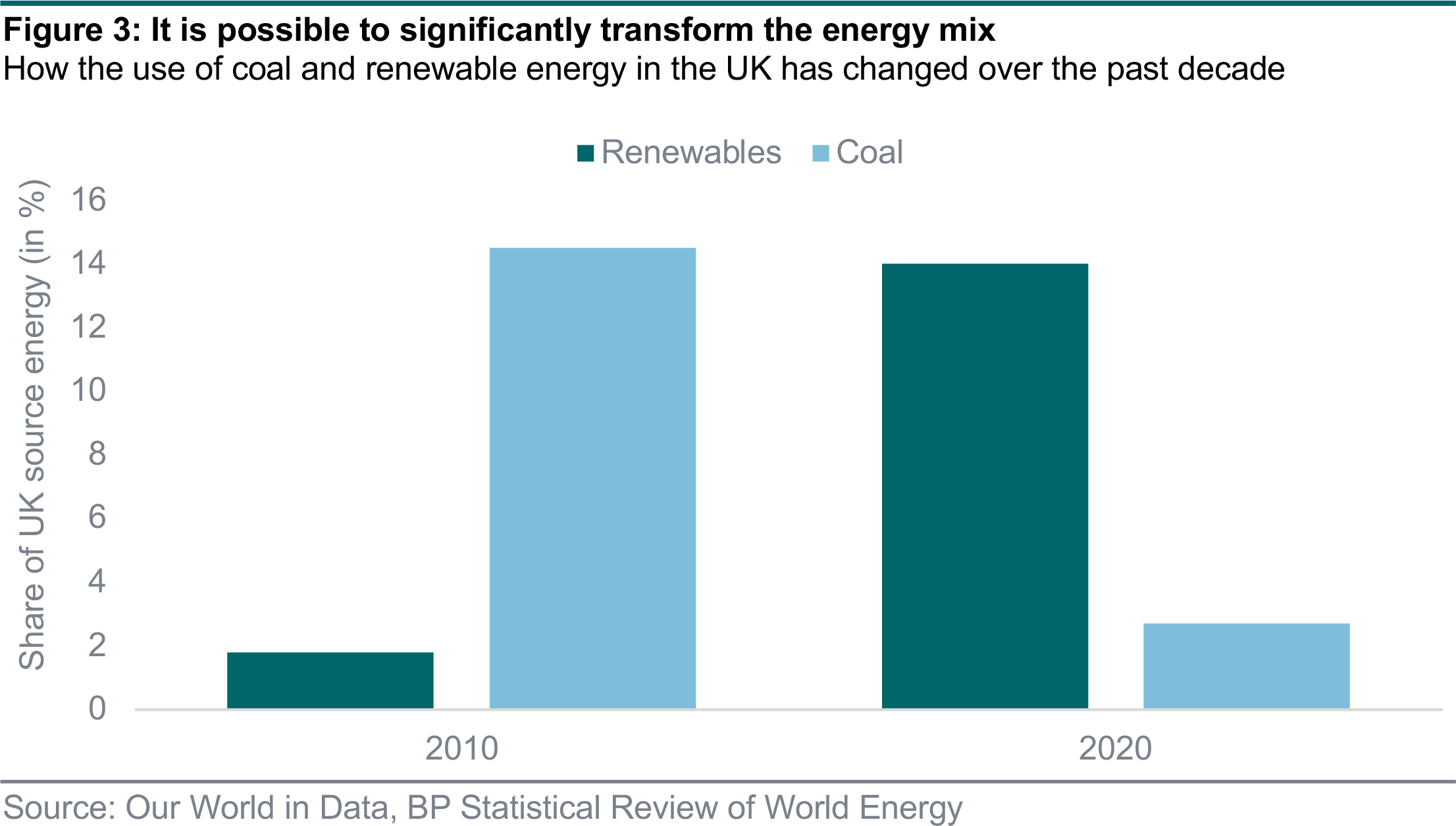

According to the Intergovernmental Panel on Climate Change (IPCC), coal-fired electricity generation must be reduced to near-zero to limit warming to 1.5°C as defined in the Paris Climate Agreement. Under the report’s middle-of-the-road scenario, combustion of thermal coal needs to be reduced by 75% from 2010 levels by 2030, and by 98-100% by 2050. Such a shift is possible if companies and governments commit to the transition. For example, in the UK in 2010 thermal coal comprised around 15% of the country’s energy mix. Following investment in renewables thermal coal now comprises just 2% (figure 3).

Over the past decade, engagement has grown in popularity. It’s an approach that involves monitoring companies and identifying environmental, social and governance (ESG) issues or strategic business deficiencies. Investors have the opportunity to interact with their management teams as well as voting at shareholder meetings to encourage them to change their practices and performance.

Investors can measure engagement’s impact through milestones and key performance indicators. Successful company engagement often entails specific metrics, benchmarking, well-defined targets and suitable verification, and can change business practices for the benefit of people, the planet and profits. Engagement campaigns, both individual and collective, have scored successes in recent years. They include collaborative investor engagement through Climate Action 100+, an investor initiative launched in 2017 to ensure the world’s largest corporate greenhouse gas emitters take necessary action on climate change. Since the launch of the initiative, nearly half of companies have set a net zero target or ambition in some form by 2050.

Research shows that engagement works best when focused on material issues and pursued over extended periods. There are financial benefits for investors when engagement occurs at the right level and with the appropriate resources.

Academics found that engagement leads to a reduction in downside risk. A seminal 2012 paper led by Cambridge University researchers with a dataset spanning more than 600 US companies between 1999 and 2009 found that successful engagement on environmental and social topics triggered a cumulative size-adjusted abnormal return of 7.1% over the subsequent 12 months. The sentiment was echoed by a study of almost 300 companies between 2005 to 2014, which found that value-at-risk was 20% lower for engaged firms compared to a control group.

We believe actively exercising the influence we have as an investor through engagement is consistent with both our fiduciary duty and our objective to be a sustainable company.

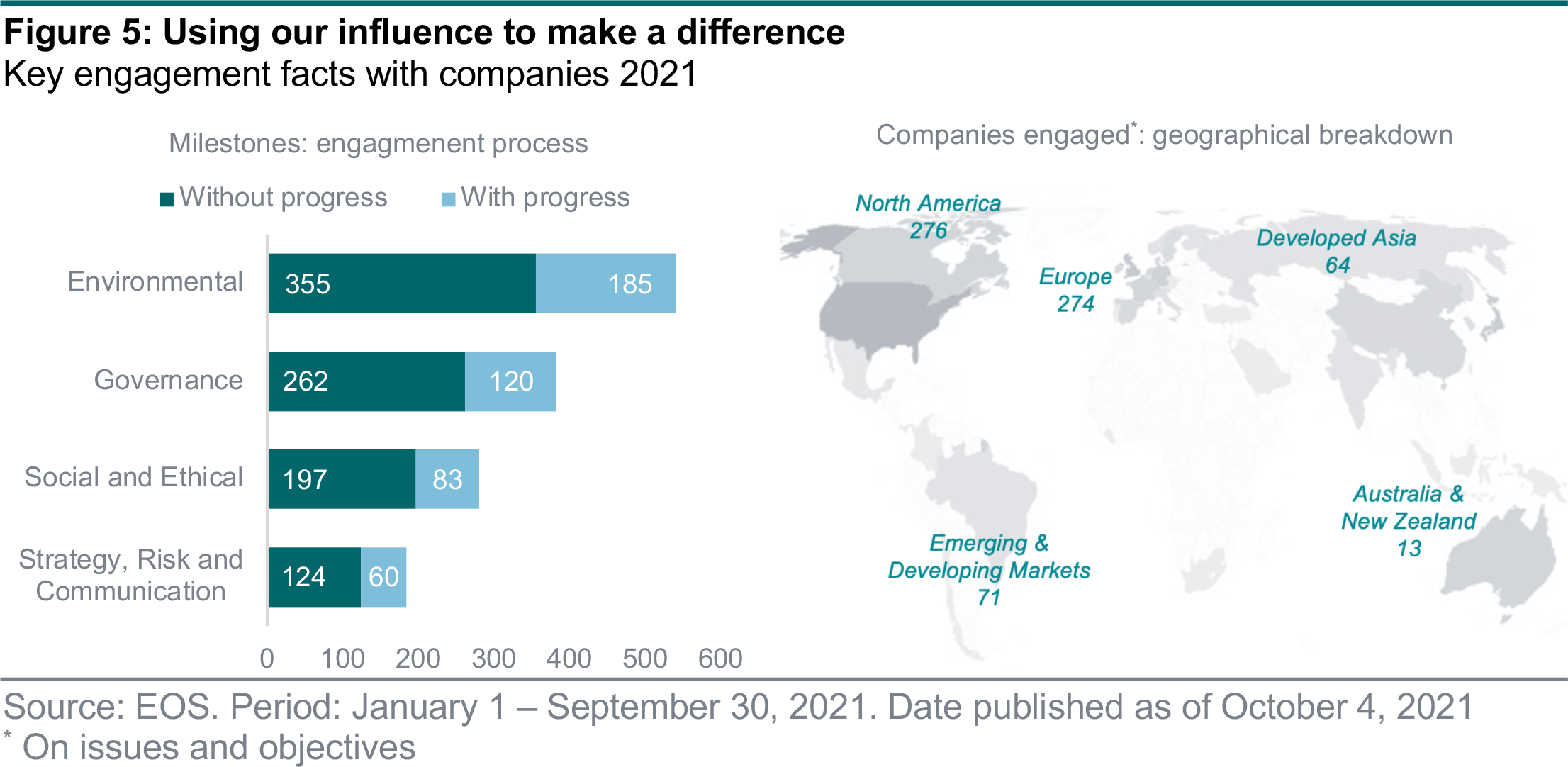

We collaborate with a leading stewardship service provider, EOS at Federated Hermes (EOS), to engage with companies in which we hold shares or bonds on behalf of our clients. We use a four-stage milestone system to track the progress of engagement, relative to the objectives set for each company (figure 5). Since the beginning of the year, we’ve engaged with 682 companies on more than 2,000 issues and objectives. For 32% of our engagements, at least one milestone was moved forward.

In addition, we use our rights as shareholders to vote at meetings of companies we invest in.12 Over the same period, we voted on 10,043 proposals at more than 700 shareholder meetings across the world. Our votes complement our engagement approach.

Lastly, we allocate a portion of each client’s assets to external managers (figure 6). We engage with these managers to communicate our beliefs and to understand theirs. We ensure the funds we select exercise voting and engagement with companies in which they invest.

We have been active owners since 2015 and continue to expand our efforts. We seek to be open and transparent about our active ownership efforts: all our 2020 votes are published here and our latest active ownership report can be found here.

Authors:

AJ Singh Head of Sustainable Investing

Bas Gradussen Sustainable Investment Strategist

Giang Vu Sustainable Investment Strategist

Martynas Rudavicius Sustainable Investment Strategist

This document has been prepared by Quintet Private Bank (Europe) S.A. The statements and views expressed in this document – based upon information from sources believed to be reliable – are those of Quintet Private Bank (Europe) S.A. as of 18 October 2021, and are subject to change. This document is of a general nature and does not constitute legal, accounting, tax or investment advice. All investors should keep in mind that past performance is no indication of future performance, and that the value of investments may go up or down. Changes in exchange rates may also cause the value of underlying investments to go up or down.

Copyright © Quintet Private Bank (Europe) S.A. 2021. All rights reserved.