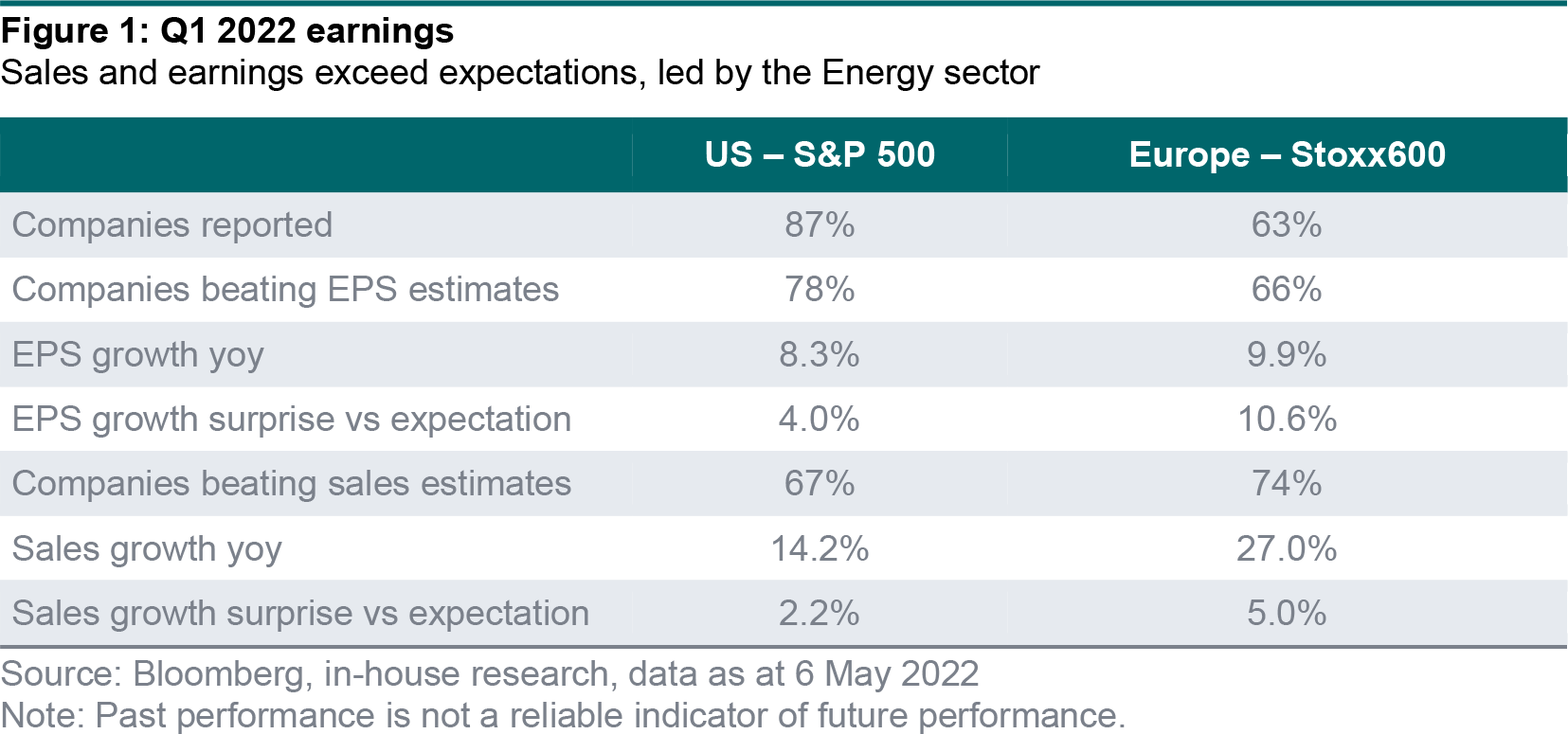

- The Q1 2022 earnings season has continued the recent positive trend with 78% of US companies and 66% of European companies exceeding expectations. These results are above the long-term trend in both regions.

- However, the magnitude of the positive earnings surprise (4% in US and 11% in Europe) is lower than recent quarters.

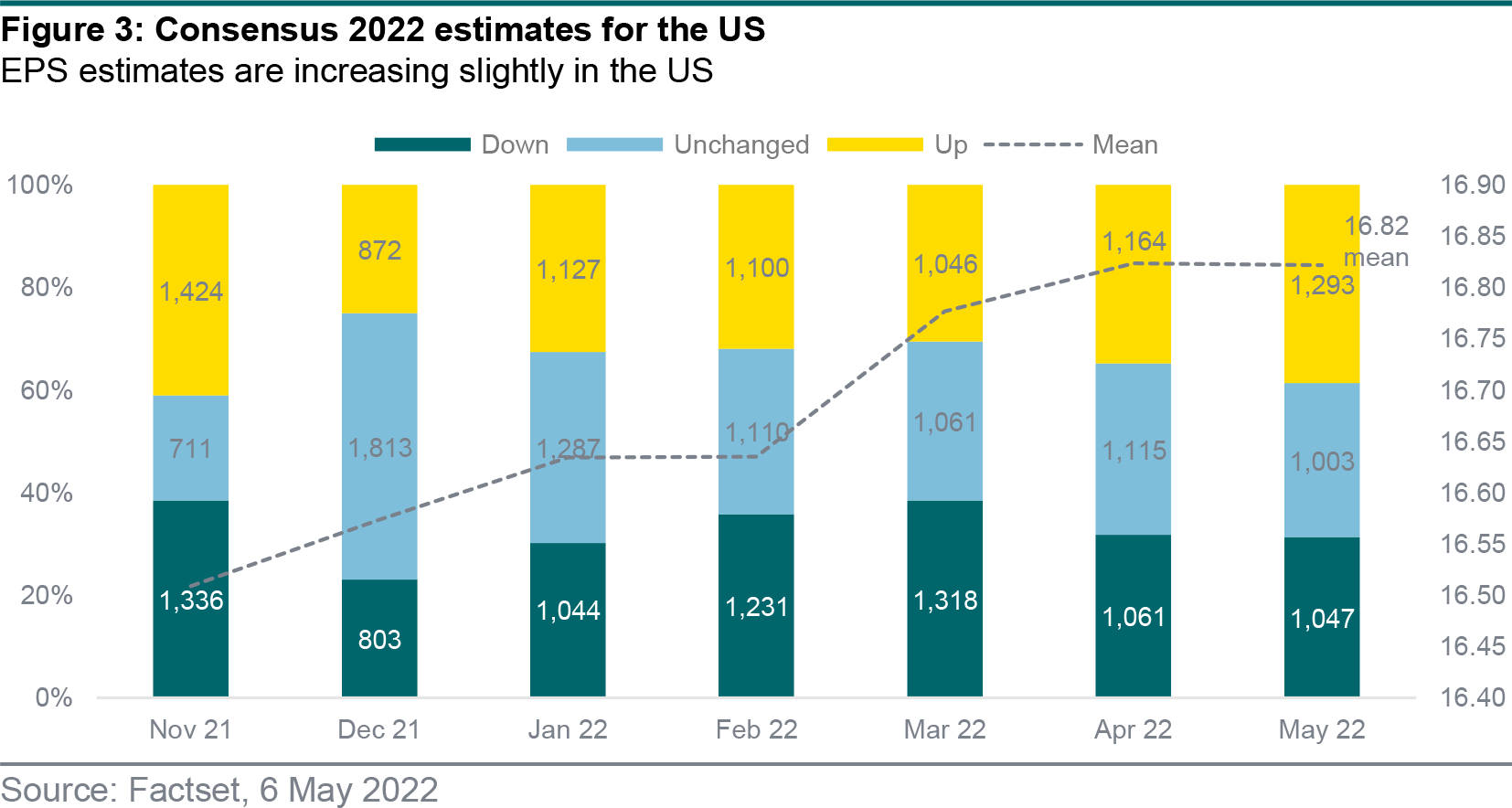

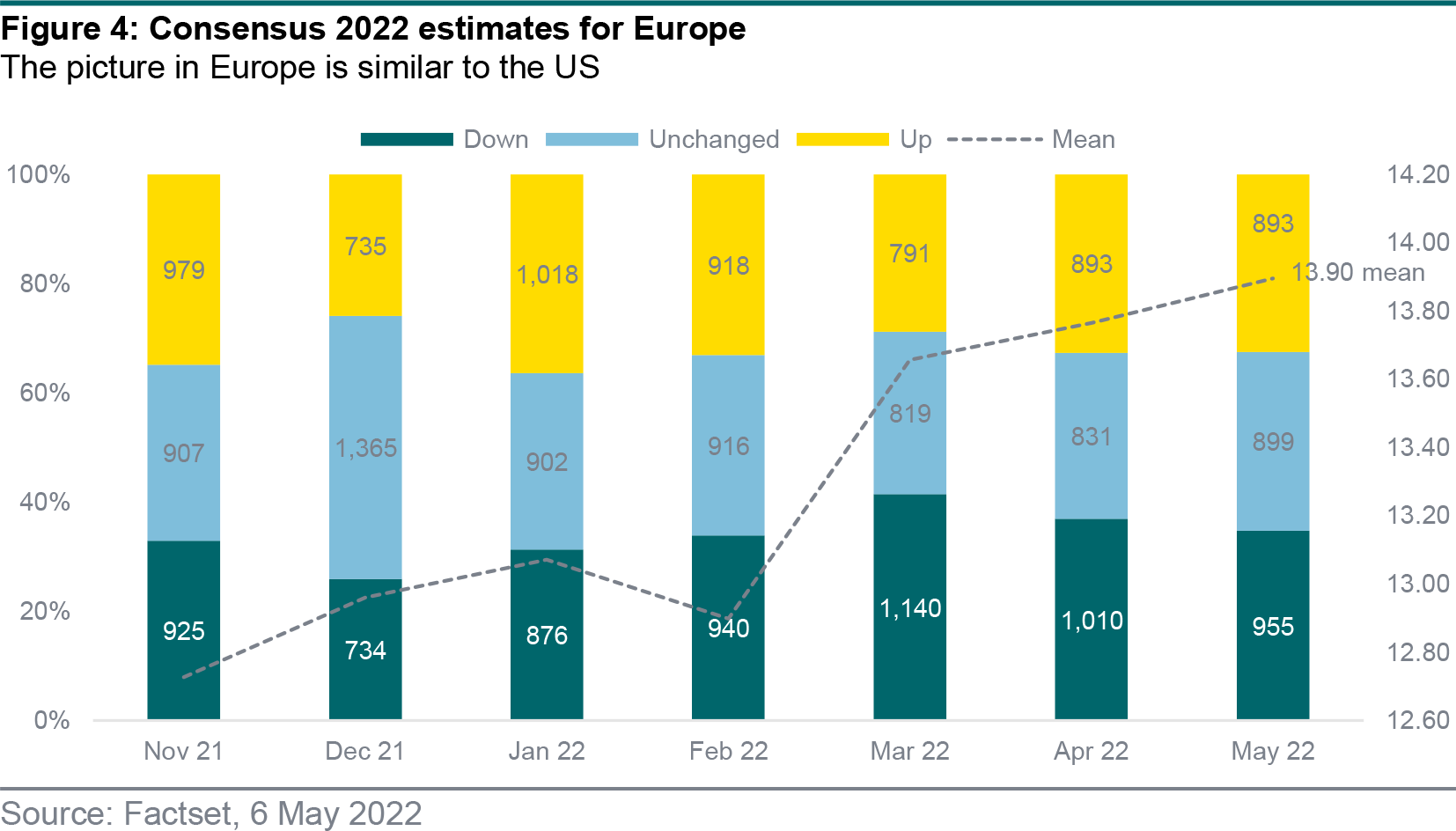

- Earnings forecasts are increasing slightly, but company guidance has been revised down modestly since the start of the reporting season.

A majority of companies have reported their Q1 results and we now have a good view of how the full earnings season is likely to conclude. Of the 87% of US companies that had reported as at 6 May 2022, 78% have exceeded EPS estimates, with an average surprise of 4%. The percentage of companies exceeding estimates is slightly above the long-term trend.

The energy sector is understandably contributing significantly to the overall performance, with sales growth of 59% in the US and 69% in Europe. However, excluding energy, sales growth is still a robust 11% in the US and 16% in Europe.

Earnings growth was 7% in the US and 45% in Europe, although this reduces to 1% and 17% respectively excluding the energy sector.

Information technology and communication services

The globally important IT sector always commands a high degree of attention and this was again the case in Q1 2022. The two largest companies in the world, Apple and Microsoft, delivered better- than-expected results, which exceeded on both the top and bottom line. Apple did, however, acknowledge that supply chain disruptions as a result of China’s COVID restrictions would impact costs in the second quarter.

Alphabet, parent of Google, had mixed results, with strong performance from Search and Cloud, but weaker-than-expected growth at YouTube. Visa issued very strong results, with revenue increasing over 25% year-on-year, led by a strong recovery in cross-border volume as global travel continues to recover.

The semiconductor industry continues to see high levels of underlying demand, although some supply chain issues are creating short-term headwinds. ASML reiterated its positive long-term outlook for the sector.

Consumer (discretionary and staples)

The two largest companies in consumer discretionary, Amazon.com and Tesla, dominate results from this sector.

Tesla’s results highlighted strong demand for its electric vehicles and exceptional execution. Revenue growth was +81% year-on-year and gross margins expanded to 30%, compared to 27% expected. The company also expressed confidence in its full-year vehicle delivery growth.

Amazon.com delivered strong growth (37%) in its market-leading AWS cloud business, but disappointed the market with lower e-commerce profitability due to rising internal and external costs. Revenue growth guidance for Q2 was also below consensus, although this can largely be accounted for by the shift of Prime Day from Q2 to Q3 this year.

Procter & Gamble reported 10% sales growth, its strongest in many years – 5% from price, 3%

from volume and 2% from mix. P&G’s price increases are being accepted by the consumer, a sign of pricing power so far. Estee Lauder, a leader in high-end cosmetics and fragrances, also reported strong sales growth of 9%, but warned that lockdowns in China would have a more negative impact in the second half of the year.

Financials

Banks are a focus for investors anticipating rising interest rates, but the sector’s underlying trends are mixed. The tailwind from credit write-backs is now largely complete, so banks are returning to business as usual. Here the outlook is for rising costs due to both staff remuneration (particularly in investment banking) and technology spending. While the interest rate environment may be becoming more favourable for banks, the competitive threat from new fintech entrants remains high and is likely to require increased investment to combat.

Healthcare

Healthcare is a diverse sector, typically less impacted by economic variables. Thermo Fisher Scientific reported above-consensus 19% sales growth, even compared with an exceptionally strong COVID-testing driven prior year period. Thermo is also seeing early revenue synergies from its biopharma outsourcing acquisition, PPD.

Eli Lilly posted robust results and raised guidance for the full year, largely driven by higher-than- expected COVID antibody sales. Novo Nordisk reported better-than-expected results from its leading diabetes and obesity franchises and raised its full-year guidance. Roche reported slightly mixed sales for Q1, with strong Diagnostics benefiting from COVID testing, but slightly less positive results from its new pharmaceutical products.

Industrials and materials

It’s been a similar picture to last quarter in industrials, with strong order books and revenues being somewhat offset by rising costs. This dynamic is fairly consistent across companies that have reported to date. Those with differentiated product lines are performing better as they have greater pricing power.

Schneider Electric and Linde are two very different companies, but both were able to raise prices (7% and 6% respectively), helping them to exceed sales forecasts.

Consensus 2022 EPS estimates for the US market have risen very modestly over the last three months, and expectations are now for 12.4% growth in EPS for 2022. Europe is seeing stronger increases in 2022 EPS, led by the energy sector. Consensus now expects 18.1% growth in EPS for 2022.

However, it is worth noting that company guidance for 2022 EPS has decreased by 0.9% on average since the start of the reporting season.

Authors:

- Kenneth Warnock Head of Direct Equities

- Bill Street Group Chief Investment Officer

This document has been prepared by Quintet Private Bank (Europe) S.A. The statements and views expressed in this document – based upon information from sources believed to be reliable – are those of Quintet Private Bank (Europe) S.A. as of 16 May 2022, and are subject to change. This document is of a general nature and does not constitute legal, accounting, tax or investment advice. All investors should keep in mind that past performance is no indication of future performance, and that the value of investments may go up or down. Changes in exchange rates may also cause the value of underlying investments to go up or down.

Copyright © Quintet Private Bank (Europe) S.A. 2022. All rights reserved.