The end of negative interest rates in Japan

After eight years in negative territory, the Bank of Japan (BoJ) lifted its key policy rate to 0-0.1% last week. It was an important move but widely expected, so markets carried on as usual. The yen continued to weaken (it’s now at its lowest levels this century vs the dollar), helping Japanese equities climb further to new record highs. This is a prime example of markets “pricing in” actions by a central bank. It’s usually only when central banks surprise markets that they react significantly. One could argue that with interest rates still very low, there is room for more increases but the likelihood of large and fast rate rises as we saw in the West is low given Japan’s elevated public debt while other central banks are turning more accommodative. An unexpected move like that next month would likely spark volatility.

Another week, another record for equities

Japan wasn’t the only equity market hitting record highs last week; the US and developed markets more broadly were as well. Last Wednesday, the US Federal Reserve (Fed) held interest rates at 5.25-5.5%, but it was Fed Chair Jerome Powell’s comments that boosted markets. Powell painted an encouraging economic picture of still robust but moderating economic growth and falling inflation, warranting lower interest rates. This is a favourable environment for stocks. As Powell also dropped enough hints that interest rates would come down this year, government bond prices rose too (as yields fell).

US economic growth might be stronger than expected, putting the Fed in a tough spot

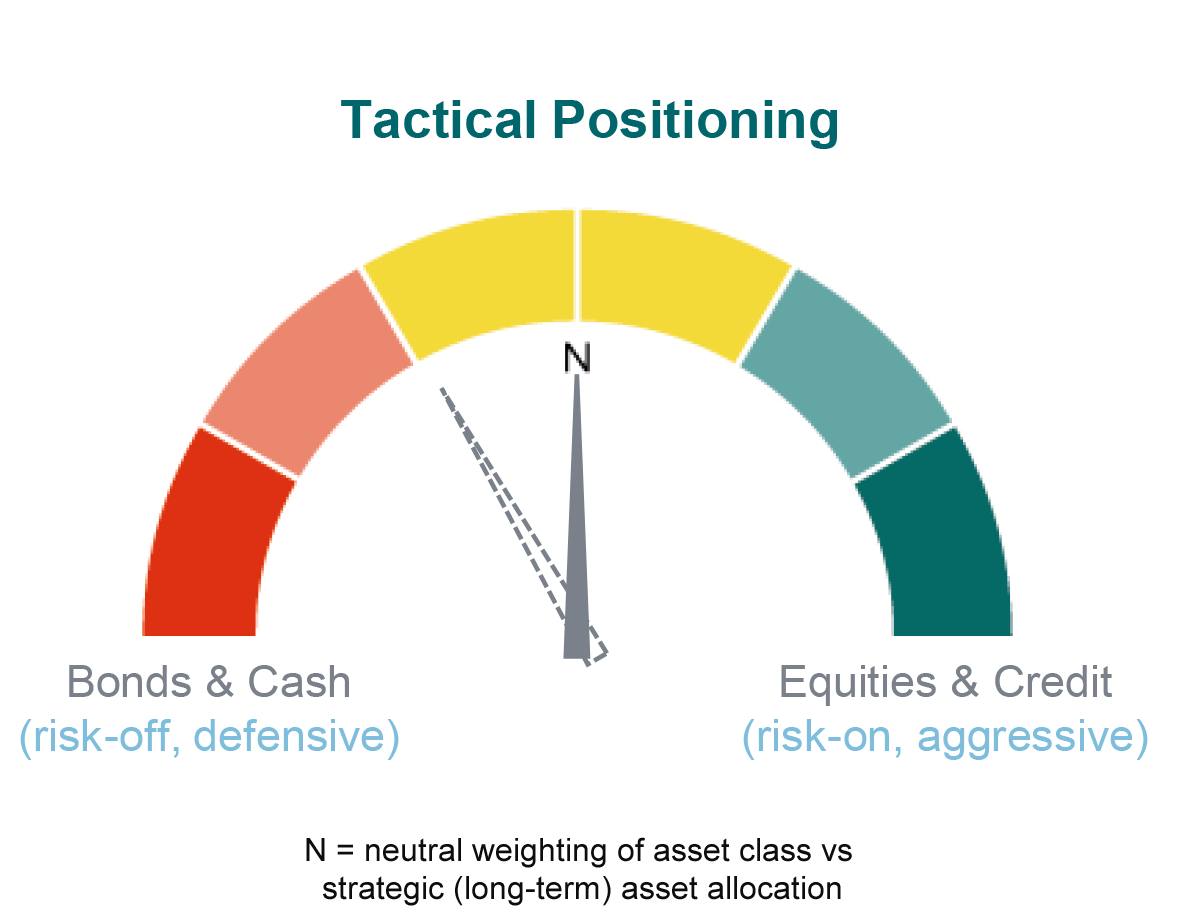

While we believe June is likely to be when the Fed will start cutting rates, it is still three months away. An unexpected jump in inflation along the way could spur volatility; we’ll be watching the personal consumption expenditure price index, the Fed’s preferred measure, this Friday. Although we expect US inflation to fall in 2024, the resilience of the economy means that positive surprises are possible. At this stage, US economic growth is tracking 2% this quarter, somewhat higher than our base case. Should further positive economic surprises materialise over the next few weeks, this could lower the odds of seeing four 25 basis point rate cuts this year and make three cuts more likely. A central bank rate path that’s still uncertain, stretched valuations and lingering (geo)political risks are reasons why we’re not increasing our equity exposure just yet. Tactically, we’re aligned to our long-term asset allocation.

The Swiss National Bank kicks off the rate-cutting cycle in Europe

The Swiss franc was the weakest currency last week after the Swiss National Bank (SNB) surprisingly lowered its key policy rate to 1.5% from 1.75%. Inflation is no longer an issue in Switzerland, so more cuts are likely, supporting our view of further weakness in the Swiss franc. We think more central banks in Europe will follow through between June and September. Last week, the Bank of England and Norges Bank paved the way for interest rate cuts, which also weighed on the Pound sterling and the Norwegian krone. The European Central Bank has good foundations to cut rates too given the ongoing stagnation in growth and falling inflation – this week we’re watching inflation data for France, Italy and Spain. That said, currency weakness could be more limited as they will likely start to cut rates when the Fed does, weighing on the US dollar. The Swedish central bank, this Wednesday, could be another central bank signalling that rate reductions are coming soon.

Staying balanced

For about a year and a half, we’ve held fewer equities and more bonds in portfolios compared to our long-term strategy. In February, given better US economic prospects and interest rate cuts from mid-year, we brought both back to neutral. As such, we increased our equity holdings and reduced bonds.

For a detailed overview of our allocation in flagship portfolios, please visit our latest Counterpoint.

Data as of 22/03/2024.