- The market reaction under our base case scenario (a second term for Macron) should be muted. A surprise win of a non-mainstream candidate would cause a major upset – lowering the euro and the CAC 40, and raising French bond yields. Low ‘Frexit’ risks but more strained relations with the EU would introduce a political risk premium on France.

- These elections matter a lot more than just for France. Under our base case scenario, given geopolitical tensions and a more multipolar world, we think France will be a key driver to push Europe to become more self-reliant across many sectors.

- France is likely to galvanise support for supply-side investment across Europe. We think two areas should benefit: first, renewable energy and the ‘green transition’ more generally; and, second, defence and technology too.

The presidential election in France is the main political event in the euro area in 2022. The French have to decide whether it’s wise to change the commander in chief at a time when a war is raging on European soil. France’s position matters in Europe and worldwide. Recently, President Emmanuel Macron has sought to play a leading role in diplomatic efforts to prevent Russia’s war against Ukraine and remains one of the main links between Volodymyr Zelensky and Vladimir Putin in trying to broker a peace deal.

Long-lasting crises have been a constant factor in Macron’s five-year term. Every president experiences problems, but the yellow vest protests (by the length of the movement and the violence of certain demonstrations), the pandemic (by its duration and its economic and social impact) and Russia’s war against Ukraine (by its location at the border of Europe and its economic impact) led Macron to adjust his initial reform agenda along the way.

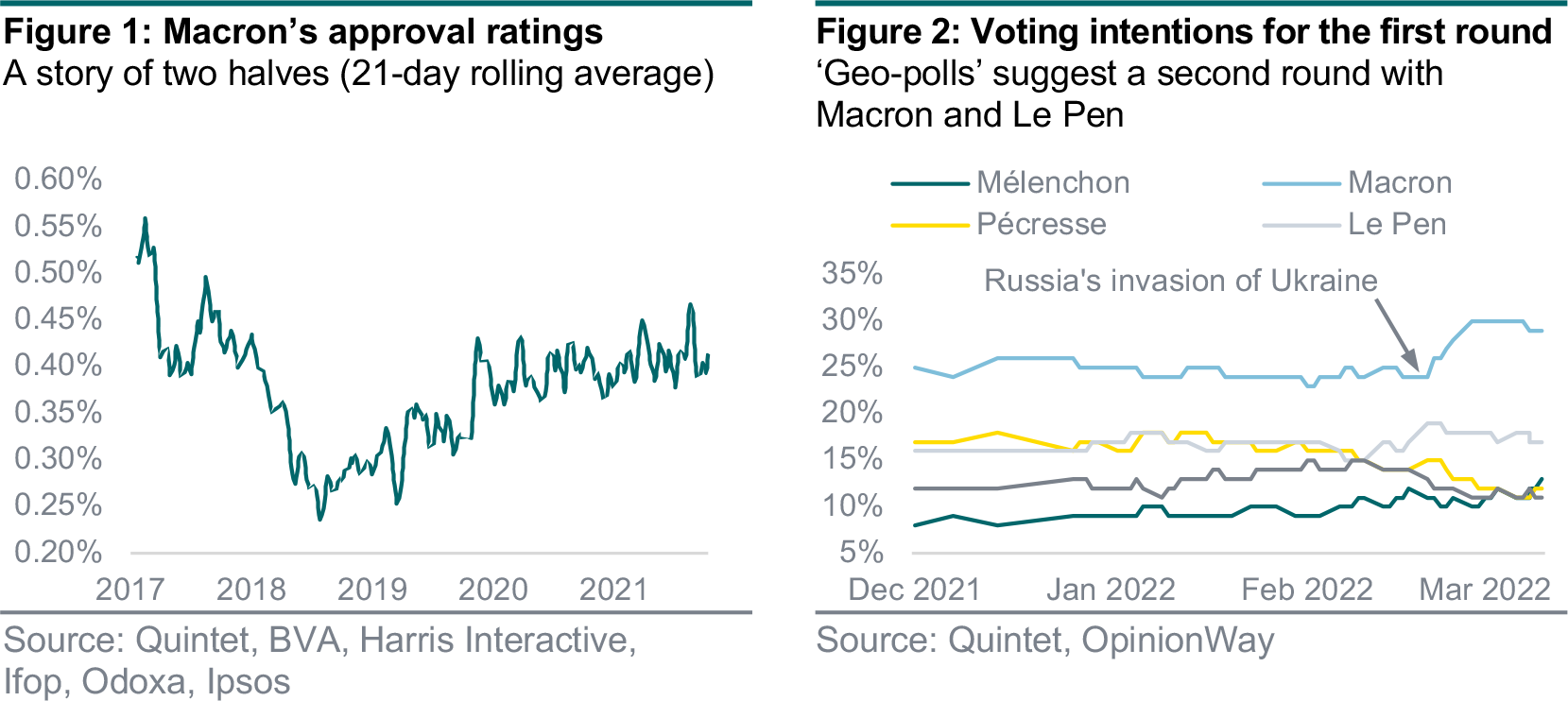

Perhaps this is why Macron’s approval ratings during his five-year tenure has been a story of two halves. His ratings declined during his first year in office, bottoming out during the yellow vest protests in late 2018. The management of the Covid crisis and France’s subsequent strong economic recovery boosted his ratings, rising even further following Russia’s invasion of Ukraine.

Generally a secondary topic in French minds, geopolitics has dominated the campaign more recently and will likely impact the result, for two main reasons. First, candidates without significant international experience, the polls suggest, appear to have little credibility in this area and limited ‘presidential status’ in the eyes of the French. From that perspective, the pro-European Macron fits this description, while Valérie Pécresse has little international exposure. Second, the war in Ukraine has weakened Eric Zemmour’s position, once Macron’s most important contender, due to his support for Putin. For instance, Marine Le Pen was more insulated as she quickly distanced herself from Putin.

The limited support for Zemmour and Pécresse somewhat benefited leftist Jean-Luc Mélenchon even though he is sympathetic to the Kremlin. The race for the contender in the second round was very close to call before the conflict, but Le Pen seems to be Macron’s most likely contender now. Regardless of the runoff in the second round, Macron looks set to win according to opinion polls, although his lead against Le Pen has somewhat narrowed in late March, with a rising risk of elevated abstention.

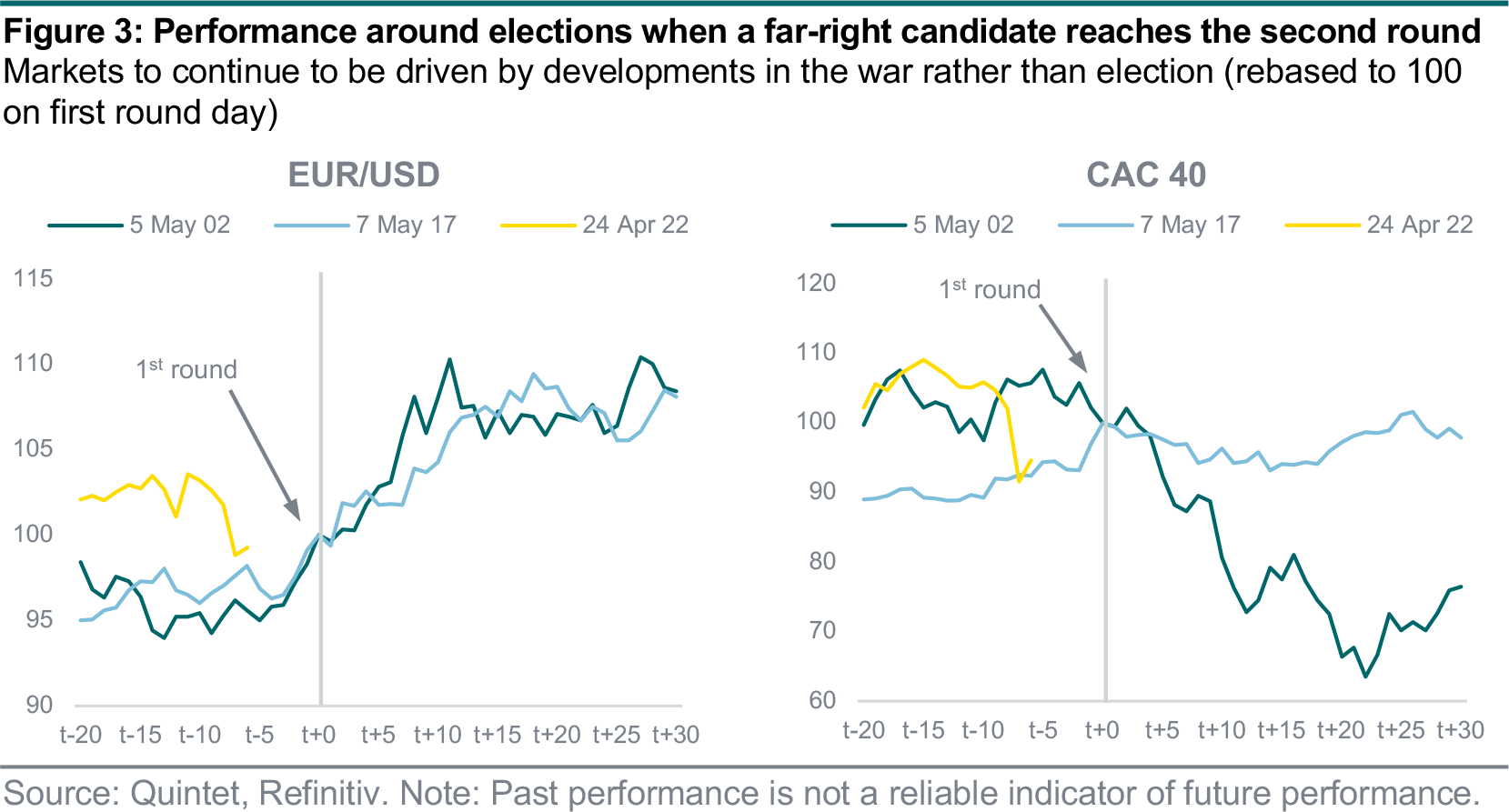

We expect a muted reaction under our base case scenario. Macron’s victory has been largely priced in, and the war has become the main driver for markets. In the past, when a mainstream candidate faced a far-right candidate (in 2002 between J. Chirac and J.M. Le Pen, and in 2017 between E. Macron and M. Le Pen), the euro rallied after the first round as markets anticipated the defeat of the non-mainstream candidate (see Figure 3). This time, we expect the euro to remain under pressure in the short term as Europe is exposed to Russia’s war more than the US is, and the European Central Bank (ECB) is much more dovish than the Fed. However, over the long run, the euro could gain from greater European cohesion.

For equities, they tend to follow global trends. In 2002, the tech bubble burst in the US pushed the CAC 40 lower. The index rose in 2017 on the back of the global synchronised recovery. In 2022, the CAC has already been rebounding in March as (excluding the scenario of a broad-based conflict) most of the uncertainty surrounding the war has already been priced in. Over the longer term, a surge in investment would boost equities, with energy (nuclear and clean), defence and healthcare sectors potentially benefiting the most.

Alternatively, a Le Pen victory would induce a political risk premium given risks of a complicated relation with the EU, sending bond yields higher (greater risk and rising debt), the euro and the stock market lower.

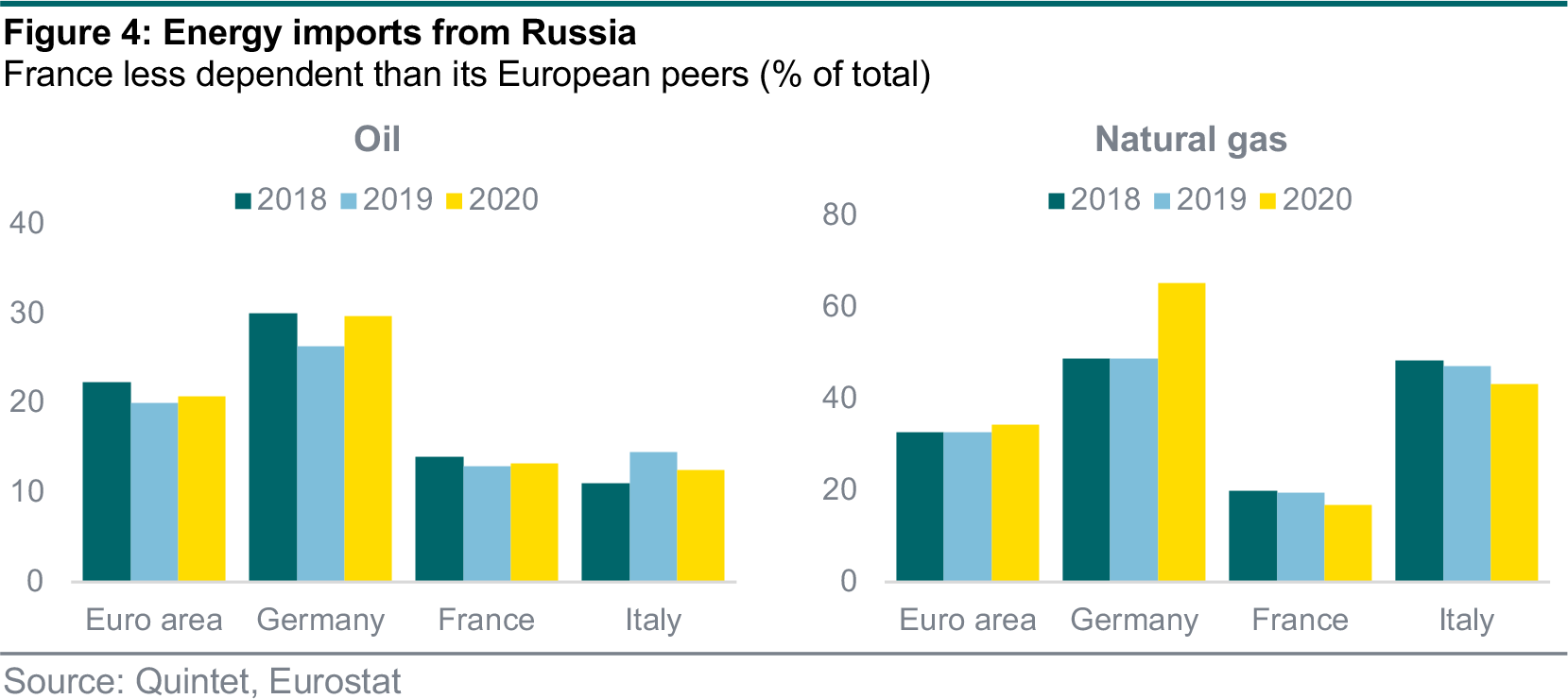

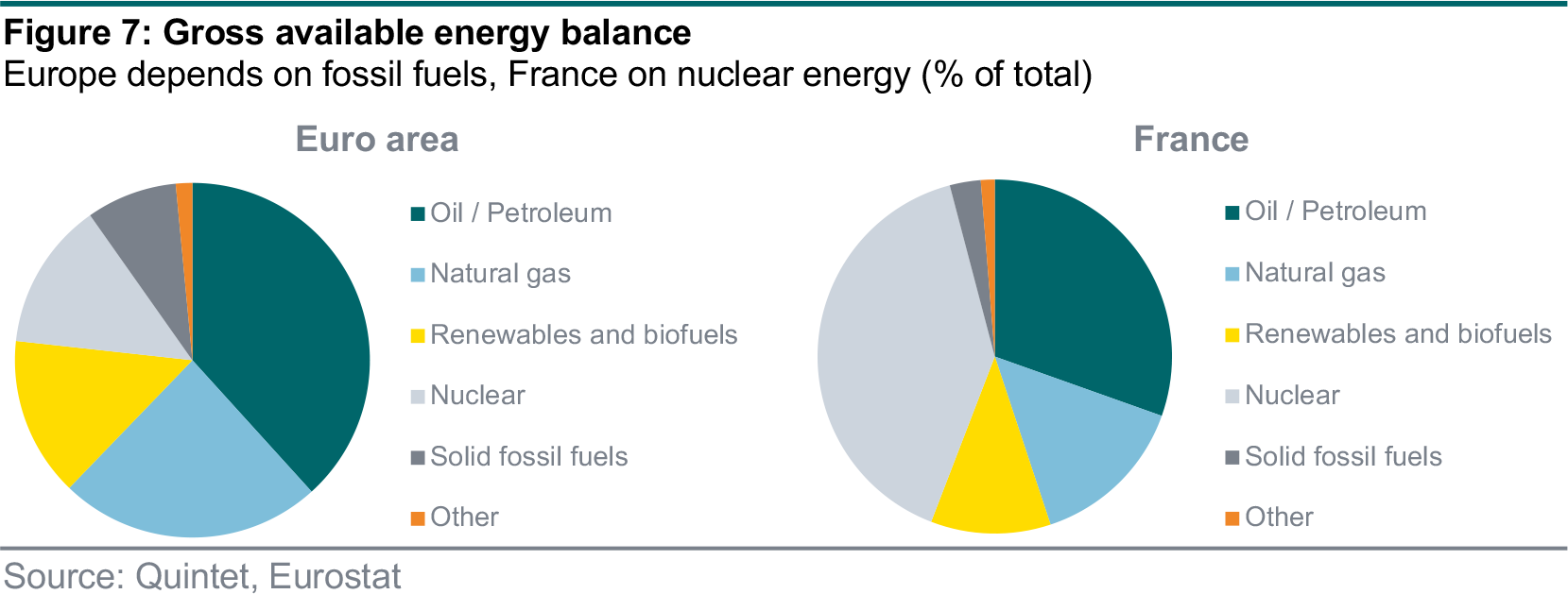

When it comes to the election, the French tend to focus on purchasing power. This factor is even more pronounced in 2022 with Russia’s war. Inflation has risen since the beginning of the Covid-19 pandemic, further exacerbated now by the conflict with soaring energy, metal and agricultural prices, which matters for both households and businesses. Europe and France are heavily dependent on Russian oil and gas. The EA respectively imports 21% and 34% of its oil and natural gas from Russia. France is on average slightly less exposed with only 13% and 17% of its oil and natural gas coming from Russia.

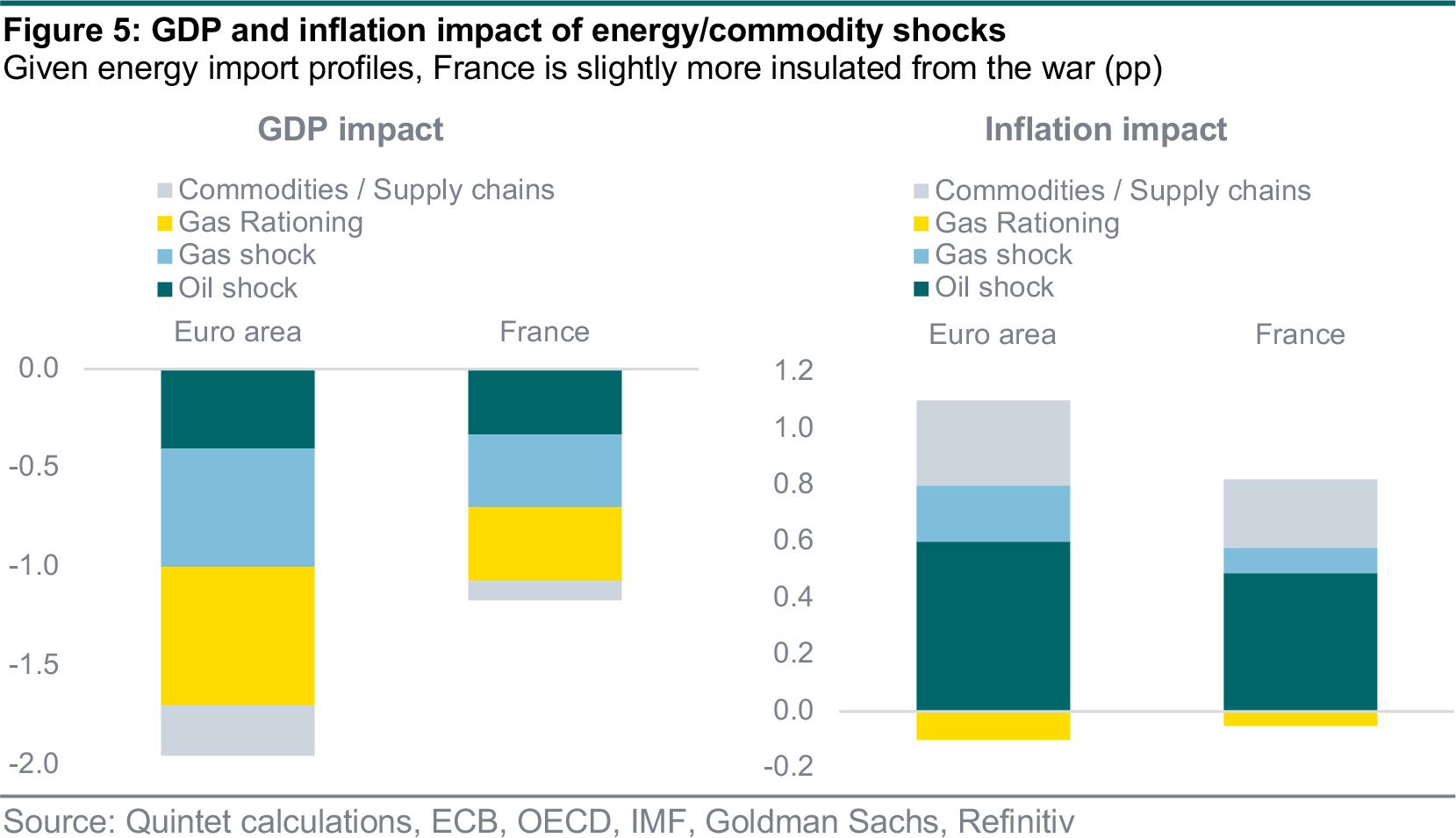

As such, the economic impact of soaring energy prices could be smaller in France relative to the rest of the euro area, which is supported by our assessment of the impact of oil at USD 130 per barrel for a year, a 50% increase in gas prices, a 50% gas rationing from Russia and other commodities / supply-chain strains. The shock could shave around 1 percentage point (pp) from France’s 2022 GDP but almost twice as much for the EA. Inflation could rise by as much as 1.0pp in the EA and by a bit less in France (0.8pp). Yet a recession still seems unlikely given strong underlying growth trends, fiscal expansion and an accommodative ECB.

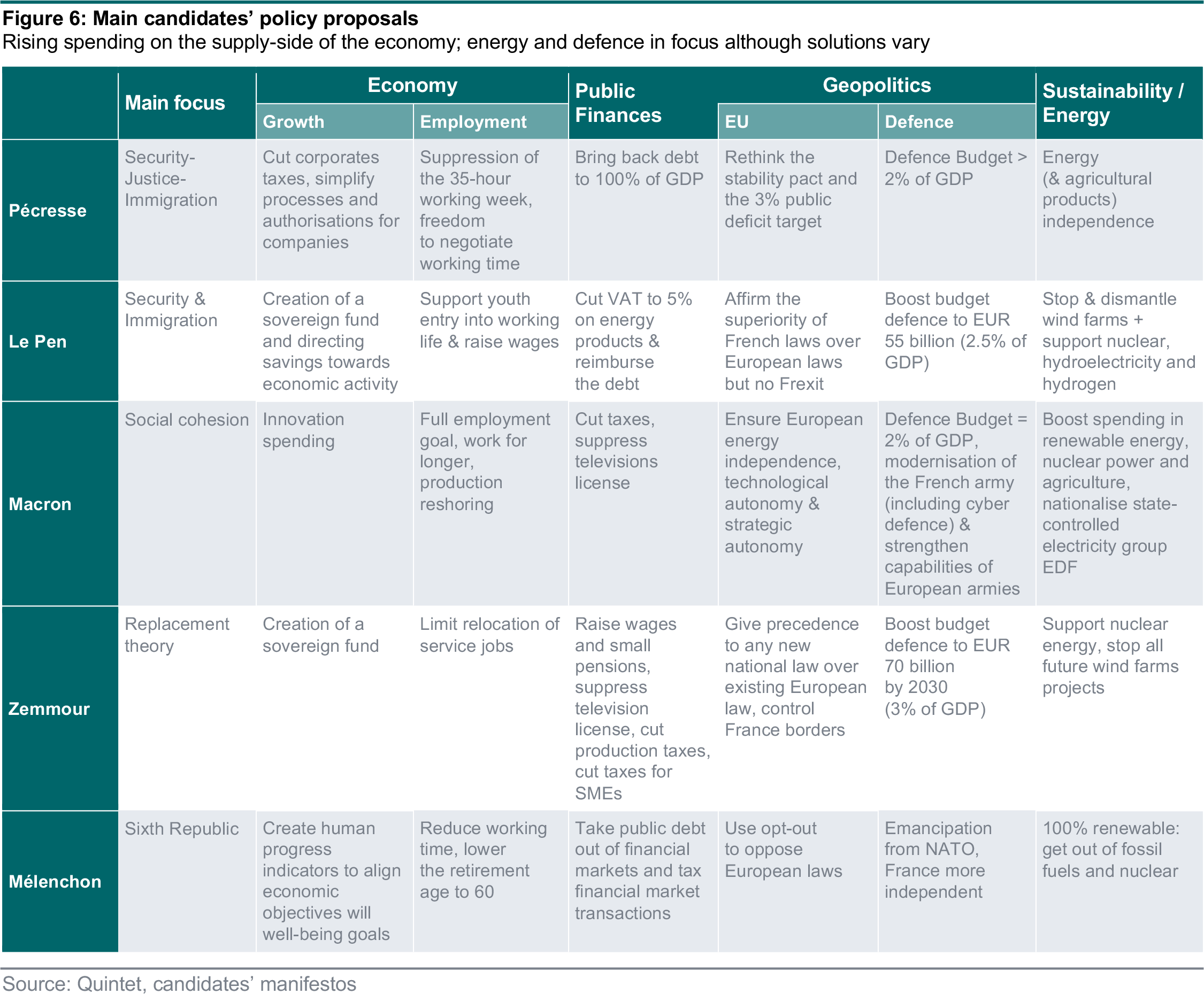

In this particular context, we expect several policy responses to cushion the negative impact of the war (see Figure 6). Some sort of fiscal expansion is likely regardless of the candidate (more spending and/or less tax). The current government of Prime Minister Jean Castex unveiled an economic and social resilience plan in March targeting the most exposed sectors and exporting companies. Measures include a EUR 0.15 discount per litre of fuel excluding tax between April 1 and July 31; financial aid for companies with elevated oil and gas bills of more than 3% of turnover; and support for specific sectors, such as fishing, agriculture, construction and transport.

If the conflict persists, more measures will likely be released. Yet Macron said he would limit the magnitude of the stimulus to be smaller than that of the pandemic, when France adopted a ‘whatever-it-takes’ approach to limit Covid-headwinds. Money from the EU recovery fund is also being disbursed now. In an alternative scenario of a populist victory, fiscal support could be larger.

Over a longer horizon, the war between Russia and Ukraine is likely to drive investment in the supply-side of the economy, as countries start to produce a larger share of what they consume. France could take the lead of this ‘revolution’ in Europe. Most of the focus will likely be on the energy sector given the urgent need to accelerate diversification and reduce carbon emissions.

The country already has a very low-carbon electricity mix owing to one of the largest nuclear sectors (around 70% of France’s power production) but aims to do more. Days before the start of the war, Macron had already unveiled a plan to build at least six nuclear reactors, and possibly another eight, under the latest national low-carbon strategy.

Renewable energy could benefit too. Reducing the country’s energy consumption and reliance on fossil fuels and increasing its carbon-free energy production is a strategy to achieve the 2050 net zero target. Firms involved in efficiency and modernising existing reactors, renewable energy, and enhanced and flexible power grids to maintain security of electricity supply and a low-carbon footprint will likely see a surge in investments. Meanwhile, production reshoring is already happening in the healthcare sector since the pandemic (relocation of paracetamol production due to a great dependence on China and India).

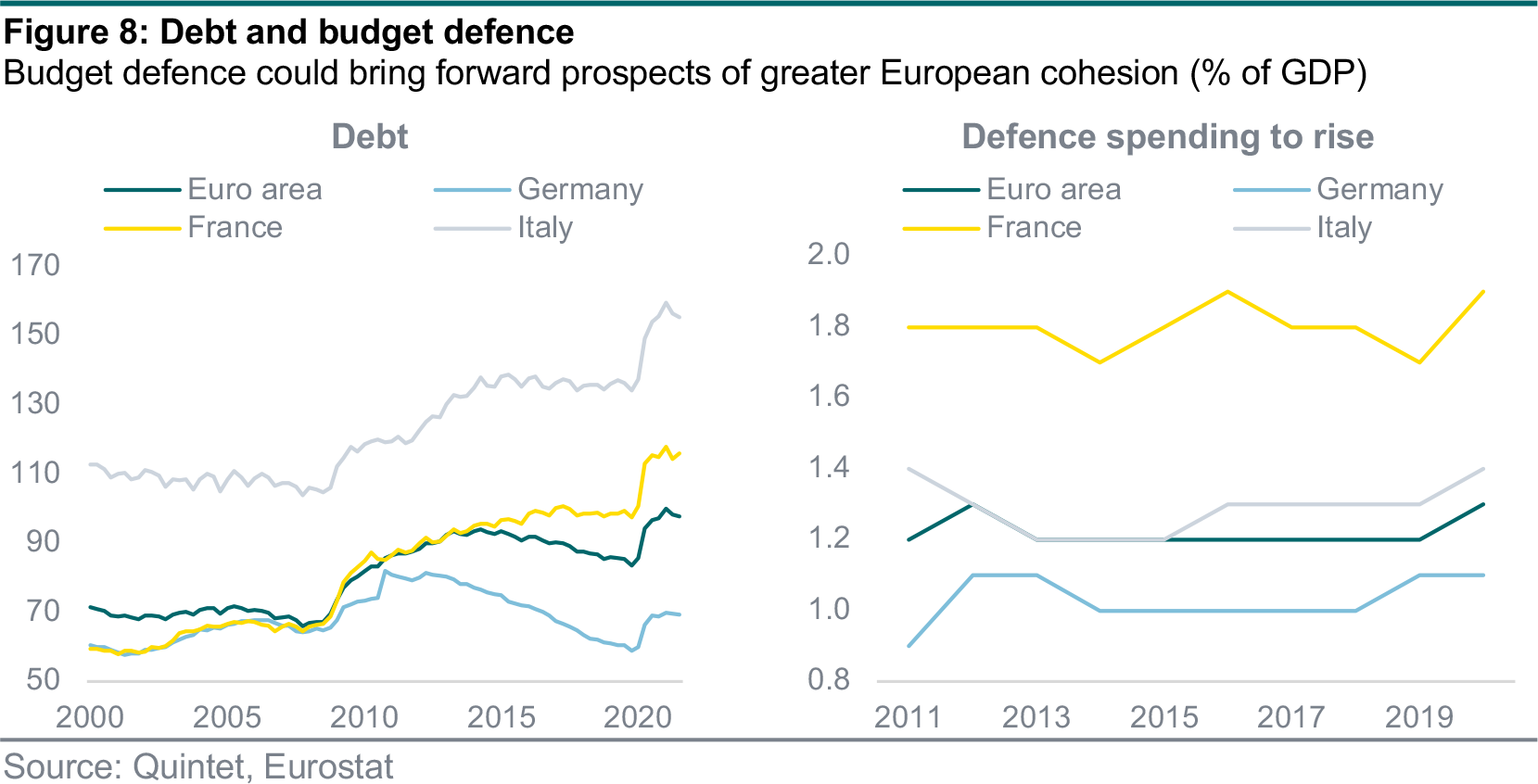

The defence sector could gain too, and be the medium to drive greater European cohesion. Indeed, many state members argue that expenditure will be best met if the burden is shared. The Covid crisis had already brought forward the prospects of greater fiscal cohesion with joint bond issuance under the EU recovery fund (EUR 800 billion). Russia’s invasion of Ukraine may encourage further integration. But the path towards fiscal union may still be a long and bumpy one.

Around 10% of the pandemic recovery funds has been disbursed so far, meaning money could now be used to tackle the negative effects of the war. Coordinated action remains uncertain as member states are divided on the most effective options to curb soaring energy prices. While northern countries tend to be reluctant to more debt, all member states have agreed to increase defence spending (e.g. Germany pledged to spend more than 2% of GDP vs 1.1% in 2020). In France, excluding Mélenchon, most candidates plan to increase defence spending to 2% of GDP or more (1.9% of GDP in 2020). Perhaps a European army could one day be created and jointly funded.

In any case, joint bond sales, whether for energy or defence purposes, could be a powerful signal of European cohesion, also making European securities a clear alternative to US Treasuries as global reserve assets, which would support the euro. Peripheral spreads, which tend to widen when risk sentiment deteriorates, have remained relatively anchored since the start of the war, highlighting the resilience of the block.

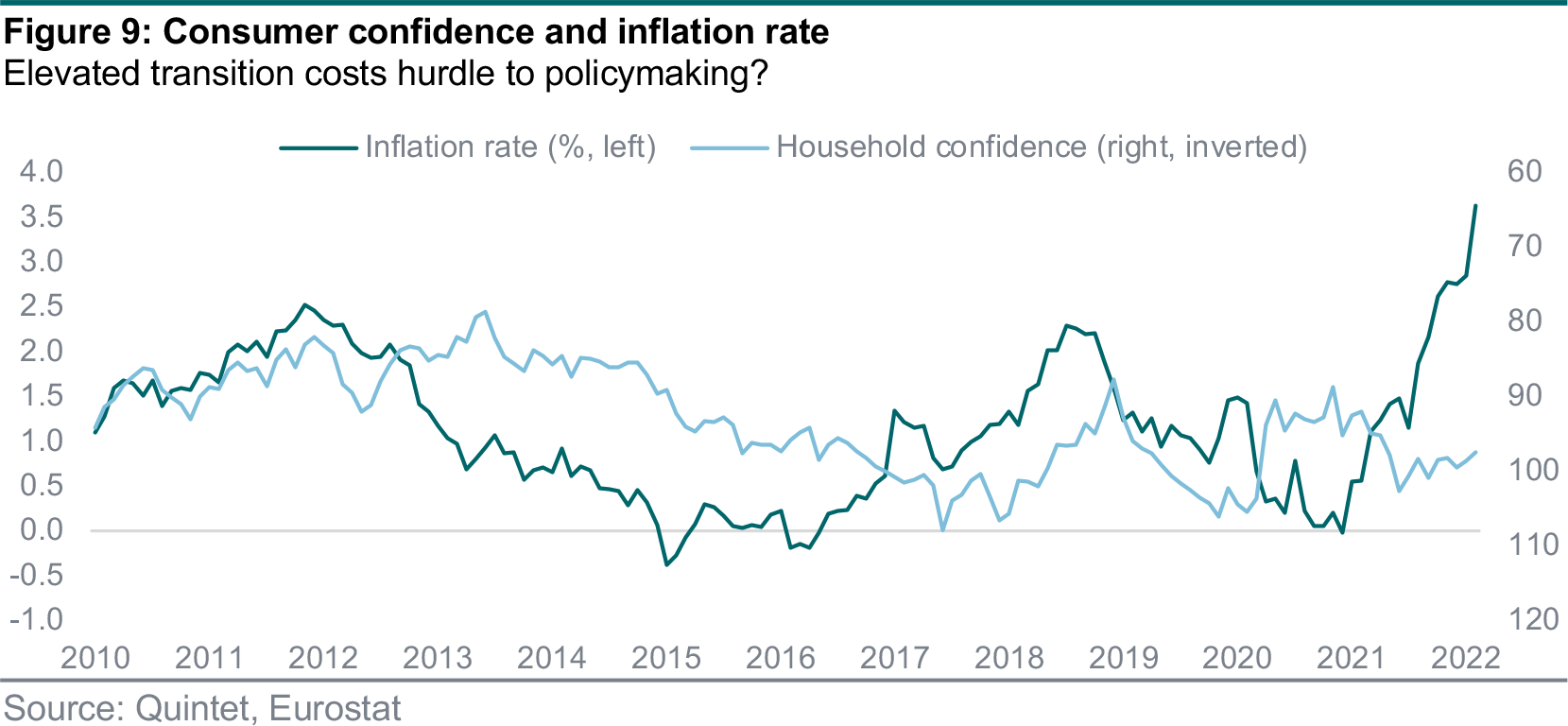

To conclude, we expect the contribution to growth from government and private investment to rise over the next few years above pre-pandemic levels. However, transition costs could be high with inflation above pre-Covid levels, which poses downside risks to policy decisions until objectives are met. Social discontent could rise again at some point, as was the case during the yellow vest protests, but the new government could minimise the impact with more support.

Authors:

- Nicolas Sopel Senior Macro Strategist

- Bill Street Group Chief Investment Officer

This document has been prepared by Quintet Private Bank (Europe) S.A. The statements and views expressed in this document – based upon information from sources believed to be reliable – are those of Quintet Private Bank (Europe) S.A. as of 28 March 2022, and are subject to change. This document is of a general nature and does not constitute legal, accounting, tax or investment advice. All investors should keep in mind that past performance is no indication of future performance, and that the value of investments may go up or down. Changes in exchange rates may also cause the value of underlying investments to go up or down.

Copyright © Quintet Private Bank (Europe) S.A. 2022. All rights reserved.