Spending on infrastructure looks set to rise, mostly in the US but also in Europe. This is a structural trend to rebuild the economy in a sustainable way, with a focus on green and digital investment.

- Headlines highlighting the ongoing debate in the US on the terms to approve a fiscal package with a focus on infrastructure miss the point. While the overall figures are still undecided, the main thing is that infrastructure spending is forthcoming. In Europe, the recovery fund, while smaller, should catalyse investment in this area too.

- Some of the infrastructure this money is going to be spent on is physical – roads, bridges, railroads and other public-work projects. But some is in green and digital areas, especially in Europe. Policymakers’ awareness of climate change and the need to support human capital suggest to us that the effort to make infrastructure more sustainable is structural.

- This long-lasting policy shift supports our view that real assets should stay well supported and benefit further. This applies to both public and private markets, especially when there’s a strong overlap between fiscal (using government investment to rebuild the economy) and sustainability aspects (tackling climate change and other key issues).

Infrastructure spending is likely to get a structural boost – more prominently in the US but also in Europe and, indeed, globally. The Biden Administration and the Democratic-led Congress are working on a USD 3.5 trillion reconciliation bill to enact President Biden’s ‘build back better’ agenda. Congress could approve over USD 4 trillion in fiscal spending over the next 10 years, though political roadblocks remain. We expect quite a few stumbling blocks ahead. A key issue to be ironed out is the top-line spending number. Moderate Senate Democrats have expressed reservation about the cost of such an expansionary fiscal policy. Needing all Democratic votes in the Senate and virtually all in the House, we expect the negotiation process – partly linked to the debt ceiling/shutdown debate – to stretch over the next few weeks and, possibly, months.

We think the negotiations will lead to the headline spending number coming down to something like USD 2 trillion. Separately, the Senate has already passed a USD 1.2 trillion package authorising spending over the next five years with USD 550 billion of new money (figure 1), though the House is currently stalling as this too is linked to the overall political negotiations. Most of the new funding focuses on traditional infrastructure such as roads, bridges, railroads and other public-work projects. To put the new spending into context, we estimate that the infrastructure bill should on average boost growth in government gross investment by two percentage points over the next five years relative to the pre-pandemic trend, lifting overall economic growth.

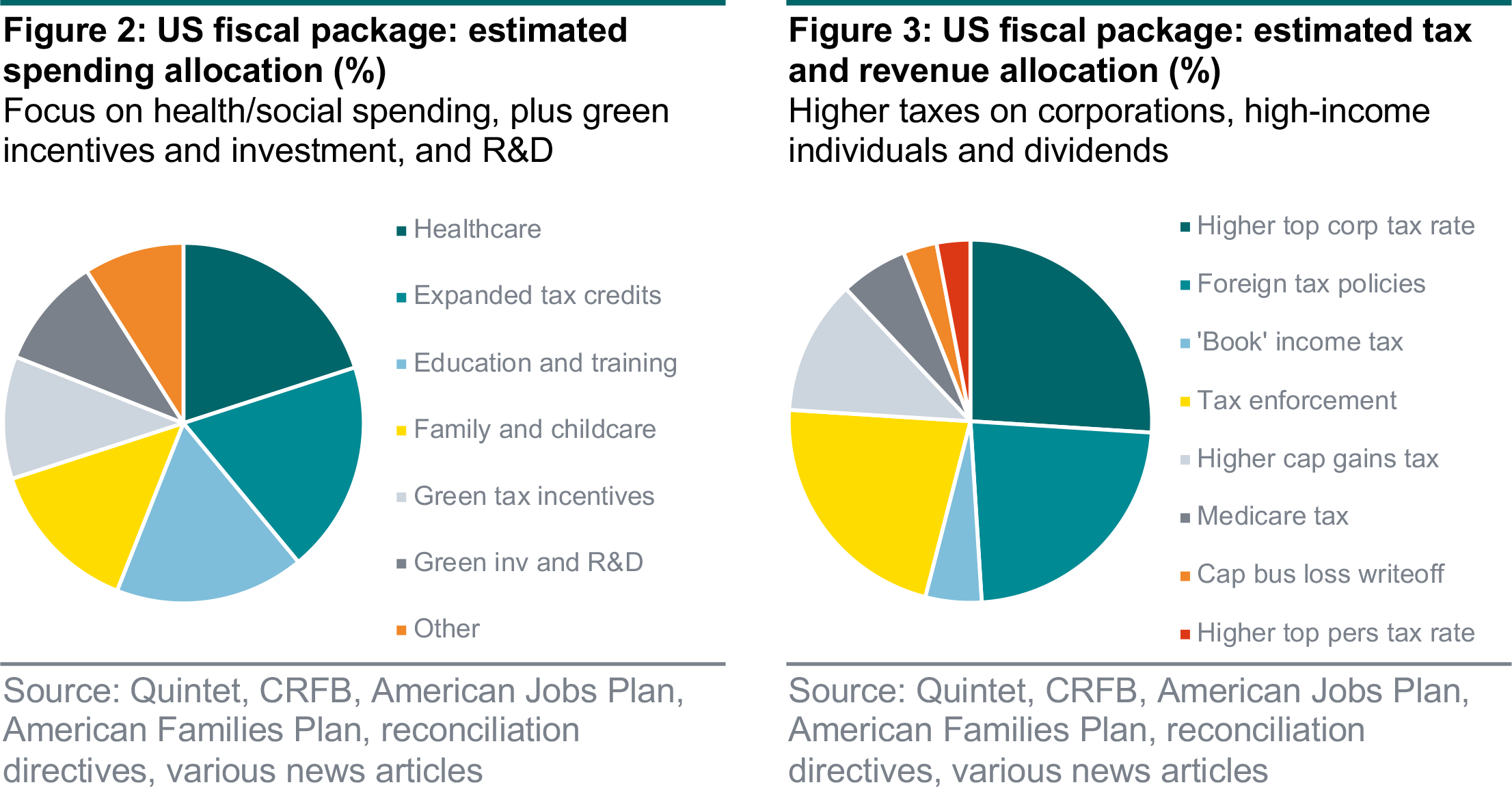

The USD 3.5 trillion reconciliation package could be scaled back – although we think it will remain substantial. Based on Biden’s American Jobs Plan, American Families Plan, reports from congressional committees plus reconciliation directives and news articles, we can approximate how the spending pie will be divided (figure 2). While the bulk will probably fund various healthcare and social spending programme, about a fifth of the total should be allocated to tax incentives and investments in green energy, infrastructure and funding for R&D. To pay for some of the spending, the plan is to raise the marginal rate on corporations and high-income individuals, making it more difficult for businesses to reduce their tax burdens and to tax capital gains at a higher rate (figure 3).

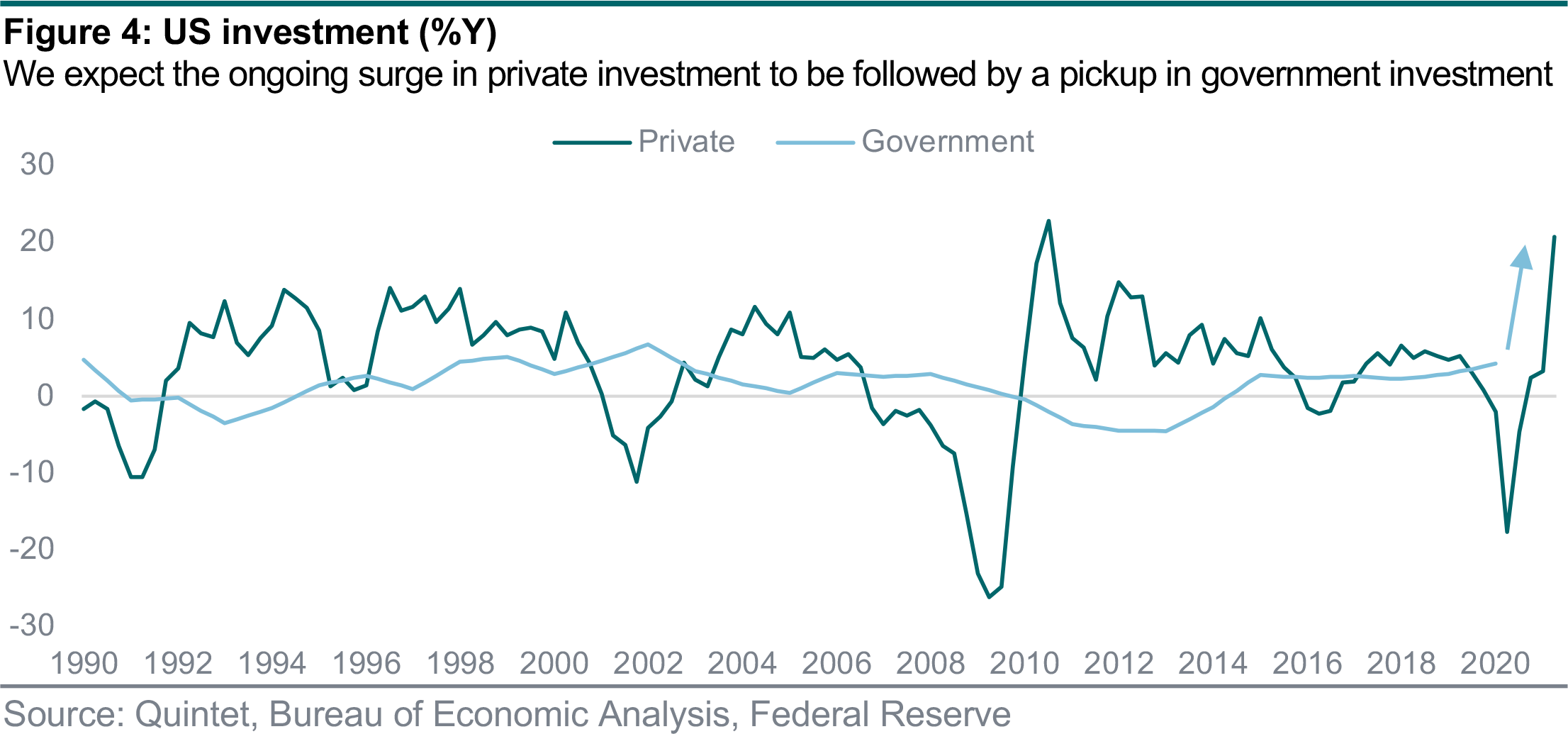

Private investment tends to follow the business cycle: it expands when things are good and shrinks when they’re bad (figure 4). Conversely, government investment – as a tool to deliver fiscal stimulus – tends to be countercyclical: its growth accelerates when things are bad and slows when they’re good and debts are repaid. The pandemic has partly altered this logic: even though reopening following the lockdowns has boosted private investment, Covid-19 has highlighted the need to rebuild some of the physical infrastructure and to make it more sustainable, building on President Biden’s election platform. We believe this to be a structural macroeconomic trend. We expect government investment in the US to pick up from here, complementing and, in fact, magnifying the surge in private investment.

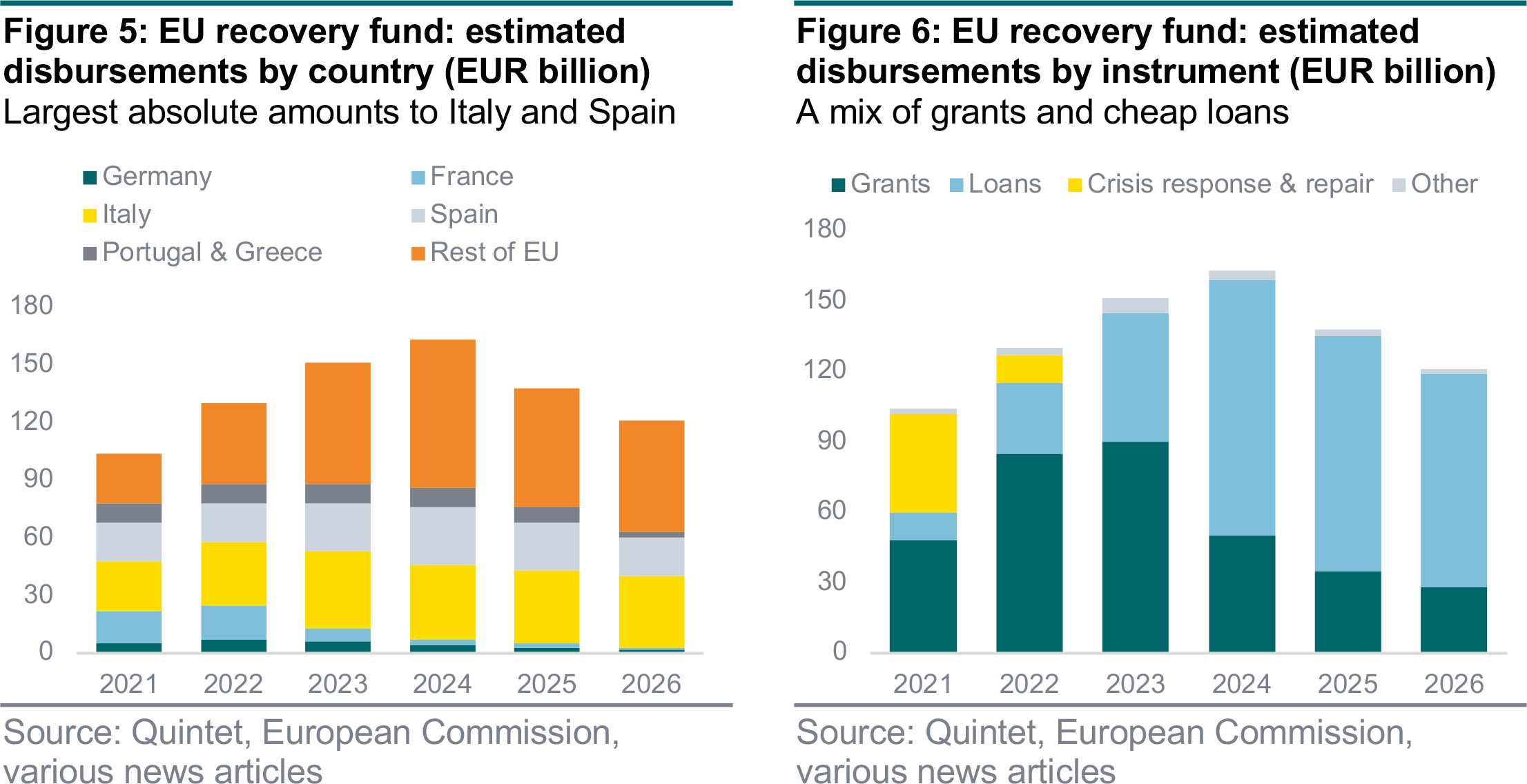

The EU recovery fund is finally operational (figures 5 and 6). The plan is for the European Commission to issue EUR 750 billion of long-term AAA-rated bonds (5% of EU GDP). Crucially, the national plans suggest that part of the funds will go to the regions (the southern periphery and the eastern fringes of Europe) and sectors (services such as travel, hospitality and leisure) that have been disproportionately affected by Covid-19. The funds will also finance green and digital priorities across the EU. Part of the money won’t have to be paid back, as it will be disbursed as grants. The rest is loans at subsidised rates. Here too the focus is on investment, with disbursements to pick up gradually and, in terms of annual amounts, to reach the highest figure in 2024 – to diminish somewhat thereafter.

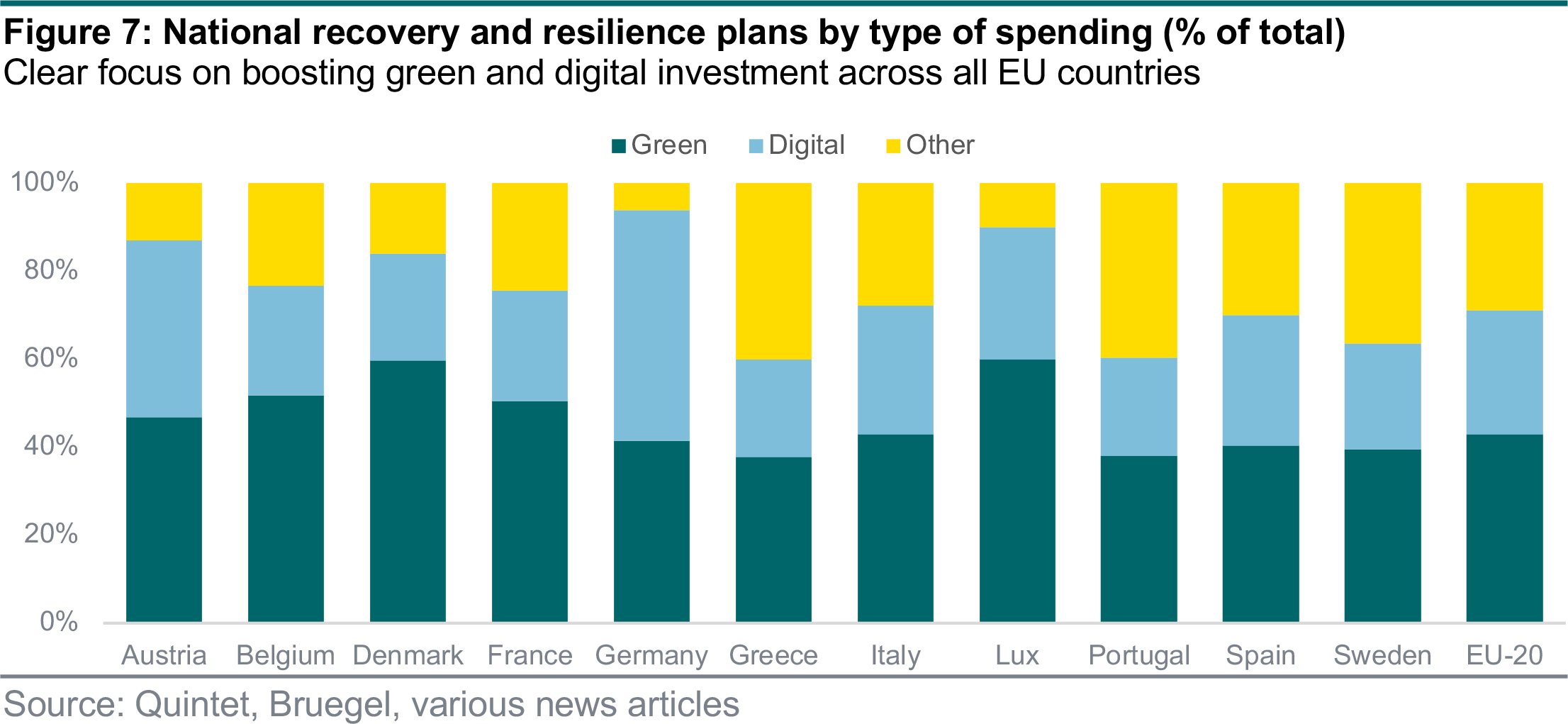

The way the money from the EU recovery fund is spent depends on the so-called national recovery and resilience plans, which are drafted by national governments and need to receive the approval of the European Commission (figure 7). The 20 plans we analysed suggest that some 40% of the expenditure is earmarked for green investment and 30% or so for digital investment. In this case too we think the likely outcome is a boost to overall investment, with public resources probably helping catalyse additional initiatives in the private sector. If anything, EU policy appears to focus on sustainable investment even more than the US, although the absolute numbers are smaller. That said, national fiscal policy will likely play a role too, perhaps contributing to close some of the gap.

According to the Energy and Environmental Institute, residential and commercial buildings are responsible for almost 40% of US carbon dioxide emissions. In the US, buildings use about 40% of the country’s energy for lighting, heating, cooling and appliance operations. Furthermore, production, transport and materials used – such as wood, concrete and steel – account for another 8% of energy use. One-third of this energy is generated from coal-burning power plants.

However, infrastructure isn’t just about roads and bridges, but increasingly green and digital investment too. One of the key reasons why we think the push to make infrastructure more modern and sustainable is structural has to do with policymakers’ focus on climate change and human capital.

Ways to tackle weather and climate-related disasters – and to reduce their probability of happening

– feature prominently in policy debates. What’s more, water scarcity is a particularly pressing issue. The need to improve the infrastructure to boost human capital, from digital to education, is very much taking centre stage too. Let’s take a look at some examples.

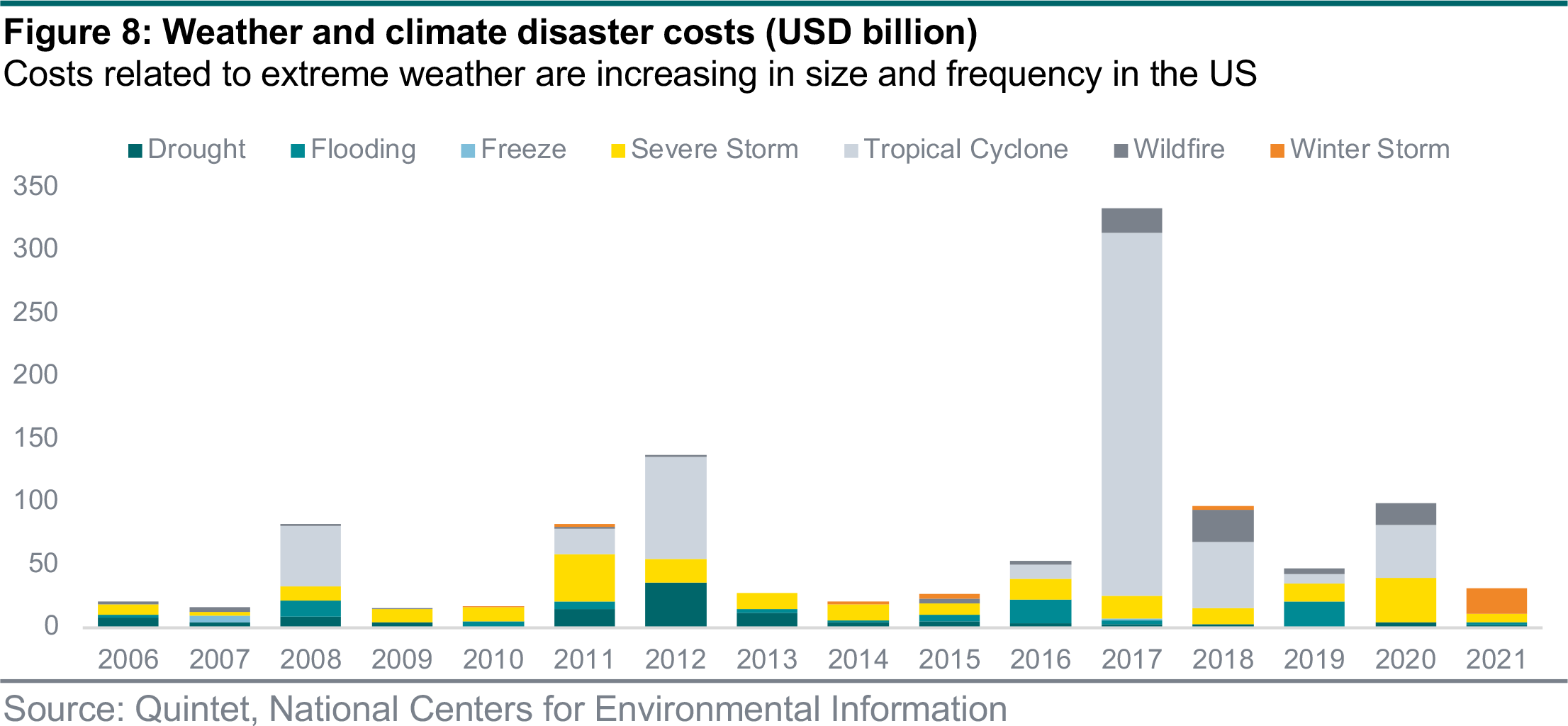

There have been 298 major weather and climate disasters, in the US alone and a quarter of them were in the last five years. According to the US National Centers for Environmental Information, the total cost is in the hundreds of billions (figure 8). The average age of the nation’s dams in the US is 57 years and the US Environmental Protection Agency projects that 4,600 bridges may be at risk from increased rainfall by 2050. The old and now fragile infrastructure had not been built to withstand these extreme weather events and any that may arise over the next several years and decades from large floods and earthquakes. The latest report from the Intergovernmental Panel on Climate Change shows that extreme temperature events that previously occurred once every 10 years are 4.1 times more likely to occur if global warming rises to 1.5ºC above pre-industrial levels.

Water is still scarce in many parts of the US, especially in the southwest where drought is a problem. A report by the EU Commission highlighted how water scarcity affects 11% of the population and 17% of the EU territory. 20–40% of Europe’s available water is being wasted (leaks in the supply system, no water-saving technologies installed, too much unnecessary irrigation, dripping taps and so on). There are innovations that have been developed to fight this, such as waste-water recycling and other waste-saving technologies across commercial, industrial and residential areas, but more needs to be done.

The Federal Communications Commission says that, in 2019, an estimated 14.5 million people in the US didn’t have access to fixed broadband service and 8.4 million to mobile broadband. This is disproportionately affecting low-income earners, especially in rural areas and in those exhibiting higher poverty rates. In the US, broadband service is not a utility (such as water, electricity or gas) – in some Asian countries it’s available to all, at reasonable prices. The broadband providers can charge much higher tariffs to make a profit in these hard-to-reach areas. Broadband availability on tribal lands, in particular, has significantly lagged that of the rest of the country.

Education infrastructure is in dire need of replacement. For example, during the global financial crisis of 2008, capital outlays for schools in the US decreased almost 40% and only returned back to that level in 2018. Schools in poorer areas have buildings that could be a health risk. With the student population increasing, this means that building extensions and equipment upgrades are urgently required, according to the National Center for Education and Statistics. The overall picture is no different in Europe.

Economic policy is increasingly focusing on these areas, with a view to fulfil several broad United Nations’ objectives too. Both the infrastructure bill in the US and the EU green deal will help contribute to multiple UN Sustainable development goals: SDG 7 (Affordable and Clean Energy), SDG 9 (Industry, Innovation and Infrastructure), SDG 11 (Sustainable Cities and Communities) and SDG 13 (Climate Action). In addition, SDG 3 (Good Health and Well-being), SDG 6 (Clean Water and Sanitation), SDG 8 (Decent Work and Economic Growth) and SDG 12 (Responsible Production and Consumption) will be positively impacted.

The Horizon 2020 European Green Deal Call looks at both mitigation and adaptation methods to combat the climate crisis and has selected 72 research and innovation projects for funding. These projects help protect Europe’s unique ecosystems and biodiversity, investing in environmentally friendly technologies. The projects funded under this initiative are expected to deliver results with tangible benefits in areas such as clean, affordable and secure energy, the circular economy, energy and resource efficient buildings, and sustainable and smart mobility, just to name a few. This is why we think the intersection between infrastructure and sustainability is a structural trend.

Authors:

Daniele Antonucci Chief Economist & Macro Strategist

AJ Singh Sustainable Investing Strategist

Philip Odum Macro Strategist

Bill Street Group Chief Investment Officer

This document has been prepared by Quintet Private Bank (Europe) S.A. The statements and views expressed in this document – based upon information from sources believed to be reliable – are those of Quintet Private Bank (Europe) S.A. as of 4 October 2021, and are subject to change. This document is of a general nature and does not constitute legal, accounting, tax or investment advice. All investors should keep in mind that past performance is no indication of future performance, and that the value of investments may go up or down. Changes in exchange rates may also cause the value of underlying investments to go up or down.

Copyright © Quintet Private Bank (Europe) S.A. 2021. All rights reserved.