Our equity investment process is built on a robust principles-based sustainable philosophy, combining our expertise with high-quality data. Sustainable investors are acknowledging that material ESG factors influence investment returns, as we explain here.

- Our revamped equity investment process embeds a sustainable approach at every step – from the investment universe we use, throughout the research process and in portfolio modelling, as well as when exercising our shareholder rights to vote and engage with companies.

- We’ve based our approach on a series of principles, and we use additional information about sustainability to enhance our analysis and expand our understanding of investment risk and opportunities. This sets us apart from investment managers that simply exclude investments which don’t meet their sustainability criteria.

- To support our new equity investment process, we’ve also launched a proprietary tool that provides sustainability profiles for thousands of public companies.

Sustainable investors acknowledge that material environmental, social and governance (ESG) factors influence investment returns. We believe a sustainable approach delivers the best investment outcomes when deployed using a principles-based approach – as a set of guiding processes and lens with which to view the world. This framework expands our understanding of investment risk and opportunities, as opposed to narrowing the vision by simply excluding investments that don’t meet sustainable criteria. Our toolkit harnesses sustainable investing’s power by deploying a number of complimentary strategies, leaders, improvers, themes and dedicated assets (figure 1).

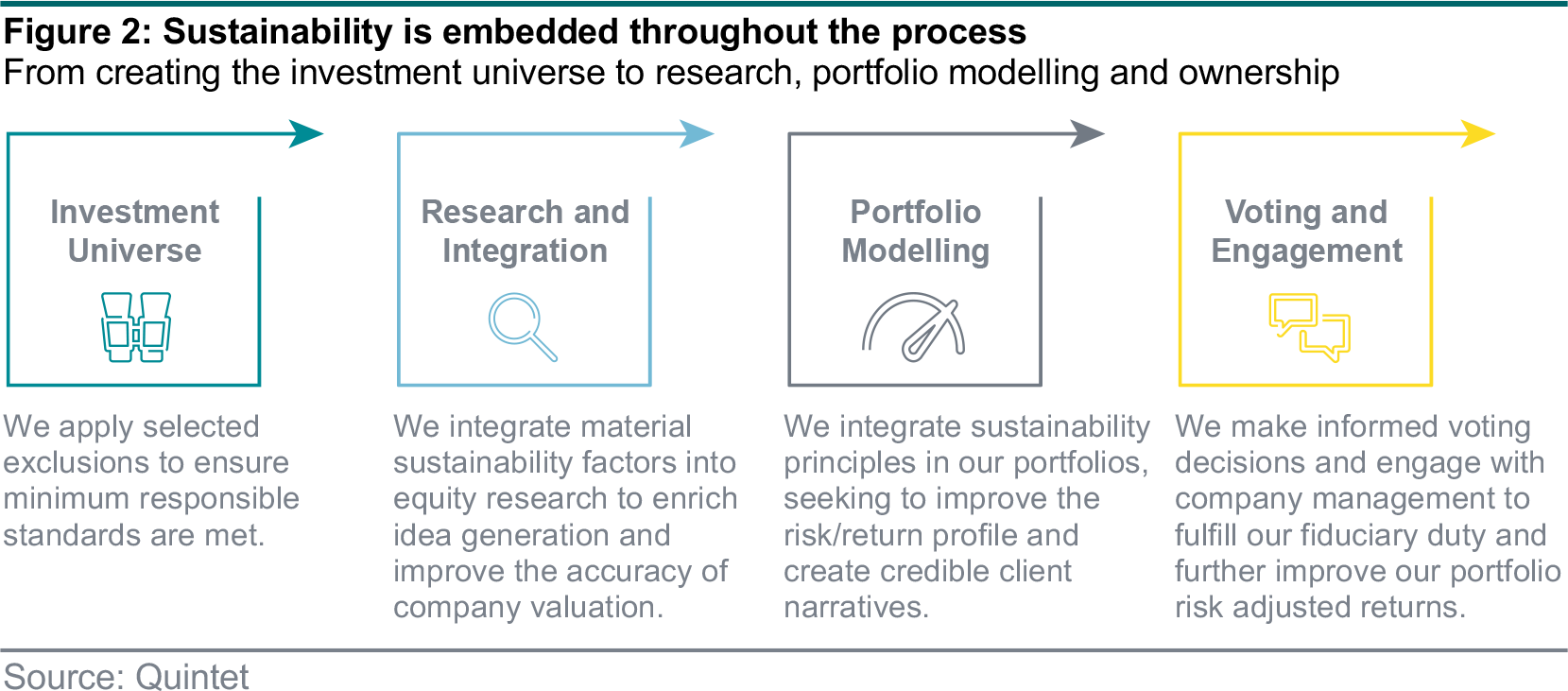

Typically, equities are responsible for most of the risk and returns in a multi-asset portfolio. Therefore, it’s important to fully embed sustainability in the research and portfolio modelling process when analysing stocks – and use the leaders, improvers and themes toolkit. We follow a four-stage procedure (figure 2).

As part of our group investment universe definition, which we derive from internal and external equity research analysts, we include a few exclusions. They are hard rules that prohibit us from buying a given security. Because we follow a principles-based approach, we seek to minimise the number of exclusions. Instead, where questionable corporate behaviour exists, we first analyse it before making a decision – a case of thinking before acting. Regardless, there are times when corporate behaviour is of dubious legality and / or its existence creates insurmountable risks to an investment. We exclude those companies involved in controversial weapons, subject to EU arms embargoes, and those that are non-compliant with the UN Global Compact and unlikely to respond to constructive engagement.

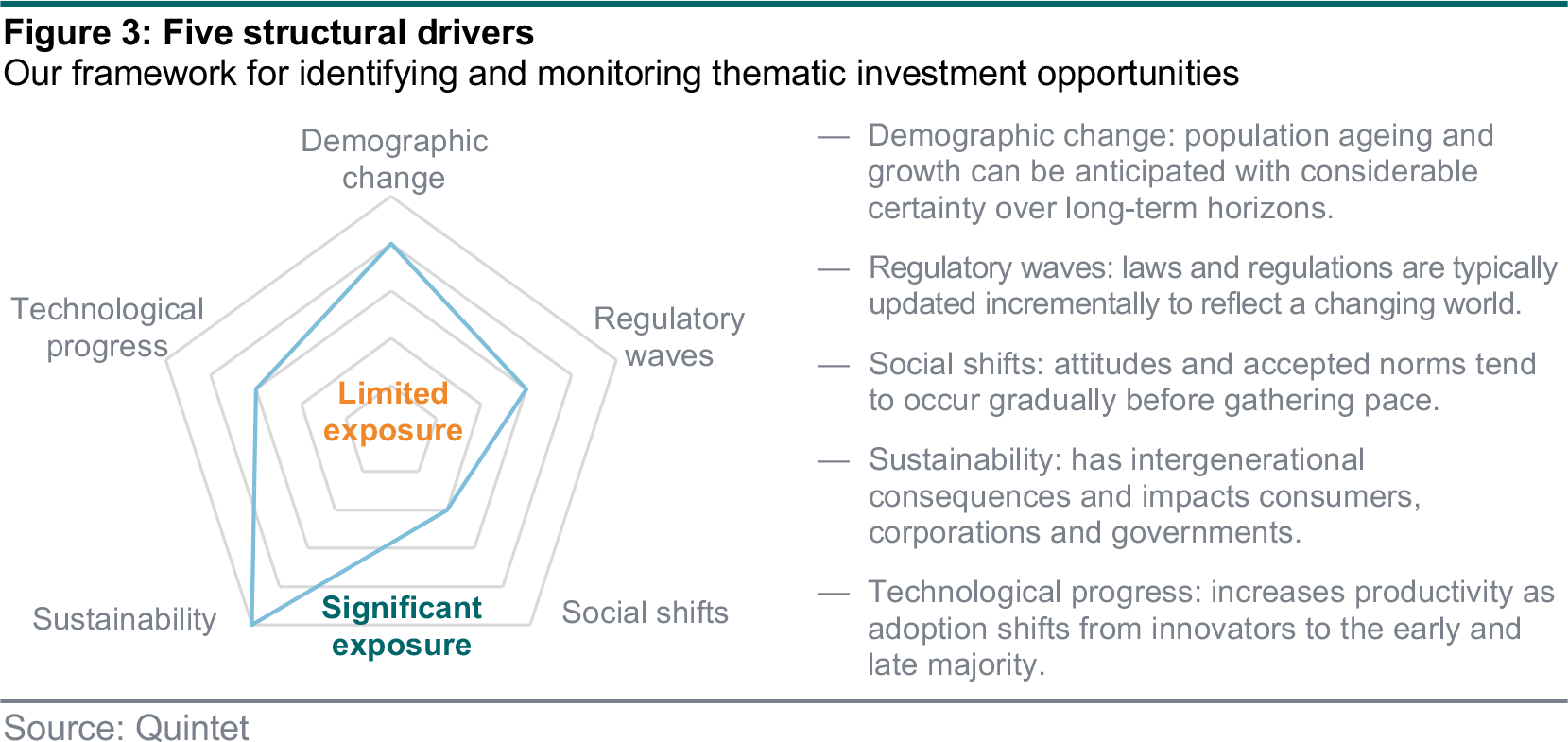

Academic research suggests as much as 85% of a stock’s performance is caused by specific factors, as opposed to broad market movements.1 That’s why fundamental research is essential for identifying winners and losers when selecting stocks. As long-term investors, we focus our analysis on a company’s structural market position and competitive environment, the potential for compounding growth, and the quality of the cash flows and business model. Sustainable investing can be deployed to both enhance idea generation and improve company analysis. When generating ideas we deploy five structural drivers (figure 3) to identify those themes and stocks with the greatest potential for long-term growth. You can read more about our thematic approach here.

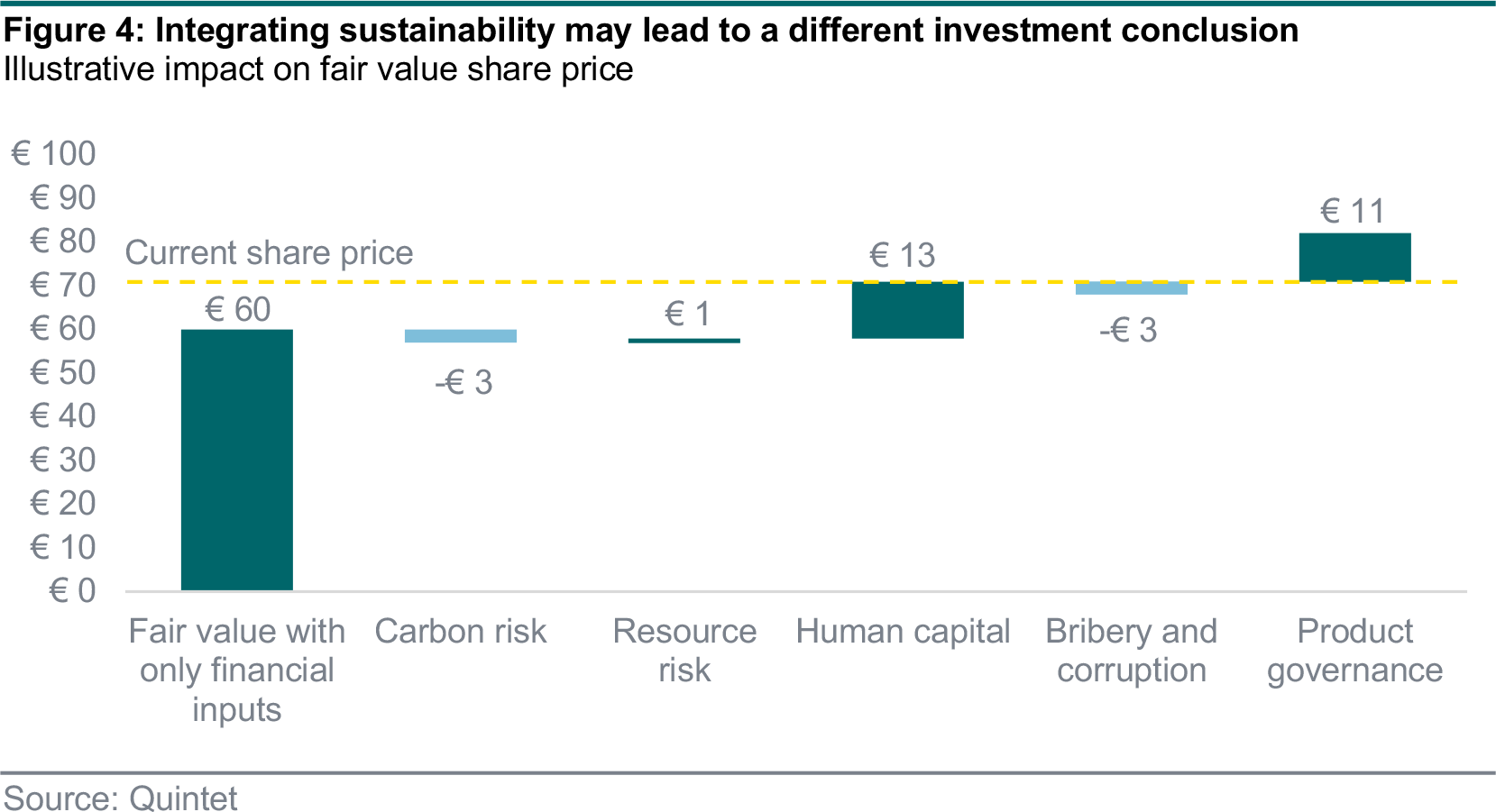

When undertaking company analysis, we consider information such as whether a company is a leader on the sustainable issues that have the greatest relevance to its valuation. These issues vary between companies. For example, the sustainability of input materials used by a capital goods firm as well as its disposal practices will be material to its valuation. However, issues such as supply chain management and human capital will be more relevant for a retailer’s share price. Integrating sustainability factors into company analysis can reveal hidden risks and opportunities and may lead to a materially different investment conclusion than using just conventional financial information (figure 4).

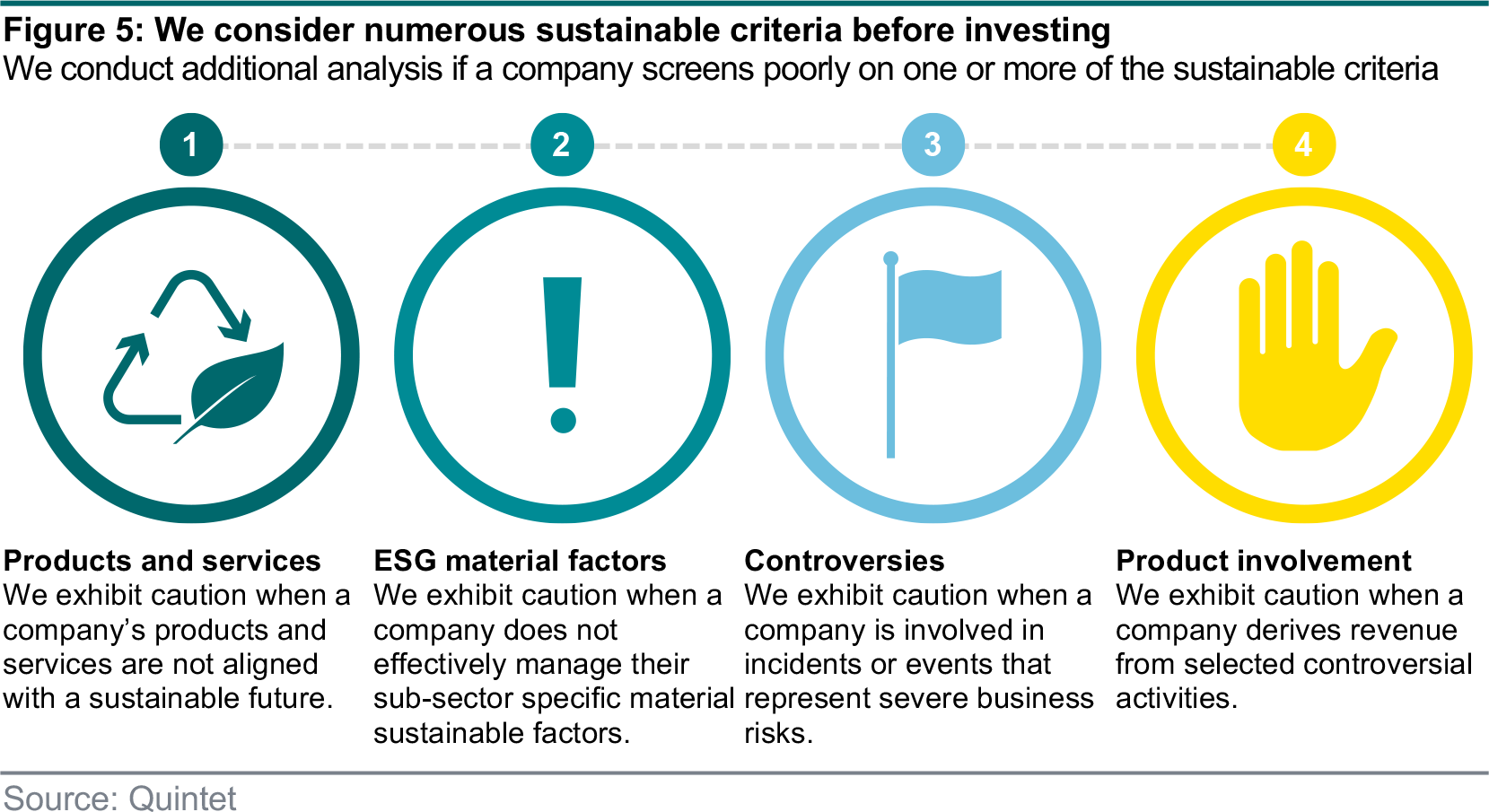

When building equity portfolios, the interaction between holdings is as important as each individual security selection. We consider overweights and underweights relative to sector and country benchmarks, as well as tilts to factor exposures – such as growth or quality. In addition to these financial metrics, before inclusion in a model portfolio, we consider a number of sustainable criteria (figure 5).

We screen potential portfolio candidates using data from primary analysis as well as corporate disclosures across over 10,000 companies with up to 100 data points per company. Because we follow an approach that’s based on principles rather than rules, when a company performs poorly on one or more of the sustainable criteria, we choose to perform additional analysis on the specific issue, rather than immediately excluding the company. This allows us to either confirm or contradict our screen’s concerns. When the additional analysis yields a favourable outcome, we include the stock in portfolios. If we’re still concerned then we don’t invest.

This progressive approach to portfolio modelling may lead us to identify stocks that are undergoing material sustainability improvement or even entire business model transformation – changes that can be great for people and the planet and also for investment returns. We record this due diligence and company analysis, which is essential for minimising sustainable-related idiosyncratic downside risks; explaining the rationale for our holdings; and protecting our reputation as a credible sustainable investor.

Once we’ve invested in a security, we initiate – where possible – our voting and engagement program. We aim to exercise our influence as an investor to improve the behaviour of the companies in our portfolio. In 2020, supported by our partner EOS at Federated Hermes (EOS), we engaged with more than 750 companies on ESG and strategy issues. We also voted on more than 10,000 proposals across 700 meetings (figure 6). In order to offer the highest levels of transparency we publish every voting decision. Our full-year 2020 active ownership report is available in multiple languages, with the English version here.

We believe a progressive environmental and social voting stance is consistent with our fiduciary responsibilities and improves our equity investment process. In 2020, we supported 96% of applicable shareholder proposals related to environmental issues and 94% related to social topics. For context, a ShareAction study of 60 large asset managers on approximately 100 climate resolutions found members of Climate Action 100+ supported, on average, 69% of climate resolutions, while non-member asset management firms supported 39%.2

We’ve built an equity investment process on a robust principles-based sustainable philosophy that combines our expertise with high-quality data. We seek to identify companies where sustainable leadership can translate into a competitive advantage and ultimately higher share prices. A thematic lens can help us discover new investment opportunities. When sustainability data raises concerns, fundamental analysis helps us to either identify a compelling case for sustainability improvement or avoid a potential investment risk.

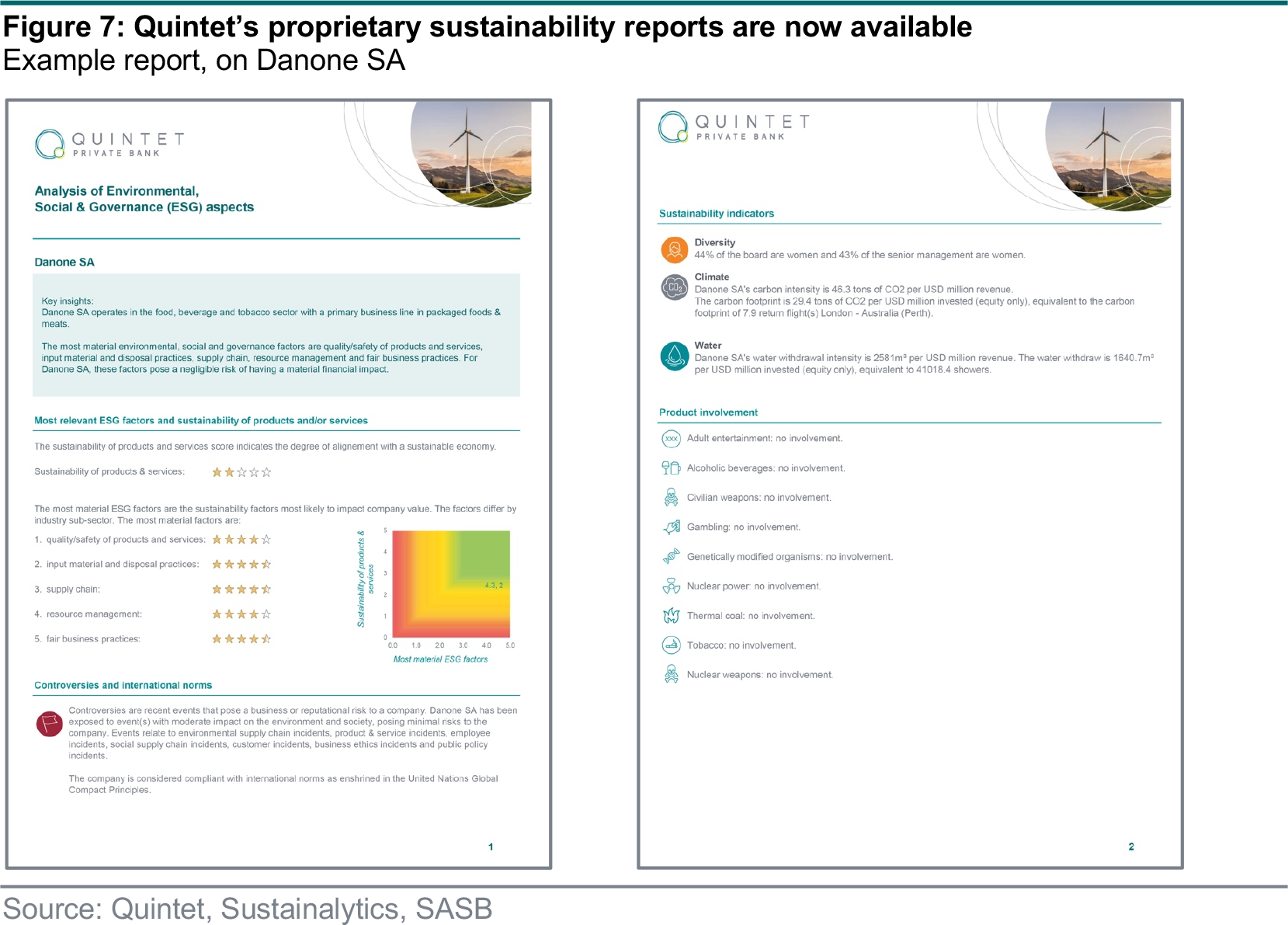

In order to integrate sustainable considerations into the research and portfolio modelling process, it is essential to have high-quality and assessable data. We’ve constructed sustainability profiles for thousands of companies by drawing on leading frameworks, such as the Sustainable Accounting Standards Board, internal expertise and trusted data suppliers.

The profiles highlight any differences between the sustainability of a company’s products and services, and how well it manages its most relevant sustainability risks and opportunities. For example, Danone operates in the packaged food industry, which faces some fundamental sustainability challenges, such as nutritional content, water risks, disposable plastics and animal welfare. However, the company manages its sustainability risks and opportunities very well, and has an impressive record on issues such as product quality, input material and disposal practises, and supply chain management.

The profiles also include:

- a summary of recent controversies – unfavourable incidents that have entered the public domain;

- a range of common statistics on gender diversity, carbon emissions, and water withdrawal - presented with everyday equivalents (such as flights for carbon emissions); and

- whether the company is involved in commonly questioned activities, such as thermal coal or nuclear weapons.

The profiles serve as a base from which we analyse equities. We also use them to obtain company sustainability snapshots and to answer key questions such as “Is the company involved in thermal coal?” or “What percentage of the management team is female?”

1 Goyal, A,. Santa-Clara, P,. (2001). Idiosyncratic Risk Matters!

2 ShareAction, (2020) Voting Matters 2020, p.g. 26

Authors:

AJ Singh Head of Sustainable Investing

Bas Gradussen Sustainable Investment Strategist

Giang Vu Sustainable Investment Strategist

Martynas Rudavicius Sustainable Investment Strategist

This document has been prepared by Quintet Private Bank (Europe) S.A. The statements and views expressed in this document – based upon information from sources believed to be reliable – are those of Quintet Private Bank (Europe) S.A. as of 31 May 2021, and are subject to change. This document is of a general nature and does not constitute legal, accounting, tax or investment advice. All investors should keep in mind that past performance is no indication of future performance, and that the value of investments may go up or down. Changes in exchange rates may also cause the value of underlying investments to go up or down.

Copyright © Quintet Private Bank (Europe) S.A. 2021. All rights reserved.